Emerging Markets Debt: Navigating oil shocks, rates and the US Dollar

A differentiated playbook for a more uncertain world

Emerging Markets (EM) have proved resilient to recent market shocks from surging oil prices and higher interest rates—a combination that would once have resulted in widespread stress. EM assets have become less sensitive to global ‘risk-off’ events, reflecting the fiscal discipline and improved fundamentals demonstrated by many EM countries over the past decade. Emerging Markets Debt (EMD) continues to offer a compelling investment opportunity, with attractive yields, solid credit quality, and a favourable risk–reward profile. The segment remains well positioned for growth in a shifting macroeconomic environment, offering investors both return potential and diversification benefits.

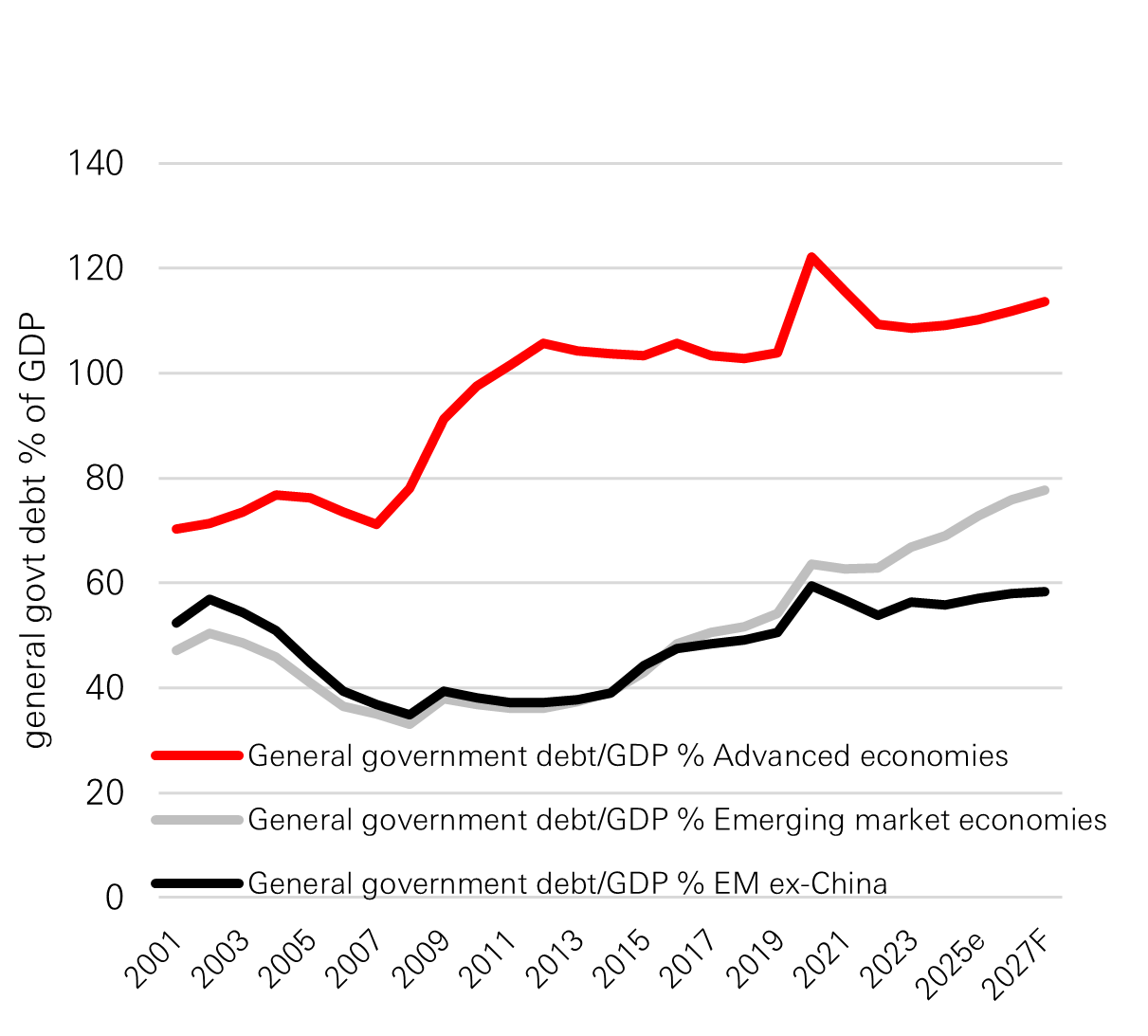

1. Fiscal discipline has led to improved fundamentals

Central to EM’s appeal is the marked improvement in fundamentals, driven by the fiscal discipline demonstrated by many emerging market (EM) countries. Global growth leadership is steadily shifting towards EM, with many countries exhibiting stronger trend growth, improving resilience, and more disciplined macroeconomic frameworks than in past cycles. Fiscal discipline is evident. Over the past 25 years, public debt dynamics have diverged sharply: EM countries have generally maintained stable balances, in contrast to the surge in advanced economies. In addition, a greater share of debt is now denominated in local currency, reducing overall currency risk and, in turn, volatility.

As a result, EM economies are better positioned to absorb external shocks than in earlier decades, supported by stronger external accounts, higher reserves, and more credible monetary policy.

Public debt has not grown at the same pace in EM

Click image to enlarge

Source: HSBC Asset Management, IMF, WEO, JP Morgan. As of December 2025, IMF WEO Oct 2025. Any views expressed were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way, HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target.

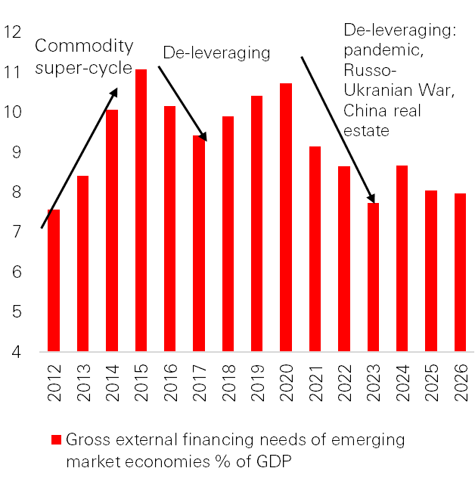

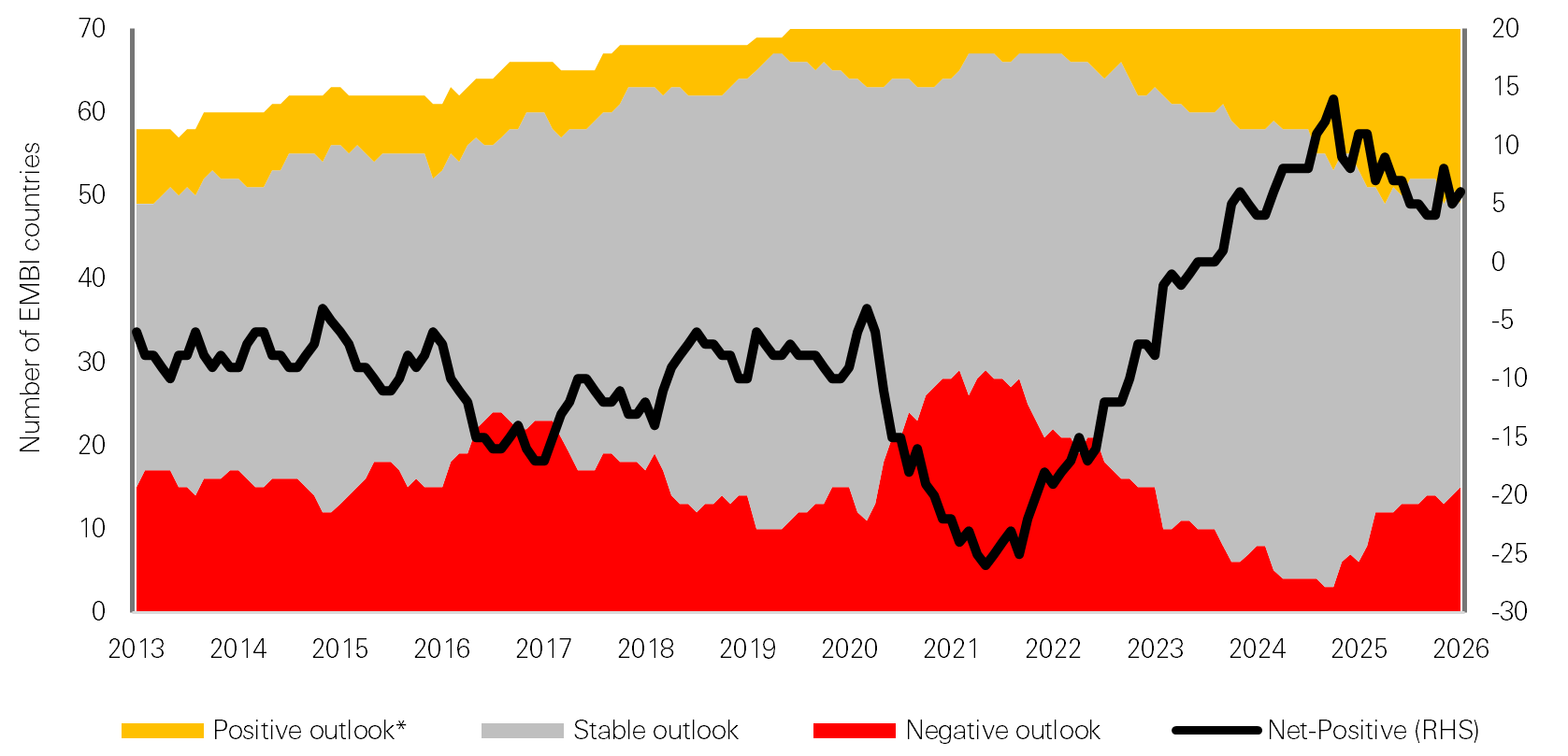

2. Fiscal discipline drives ratings momentum

Following the pandemic, EM sovereigns benefited from high nominal GDP growth to re-anchor fiscal accounts and deleveraging through debt restructurings and IMF programmes, helping to keep external financing needs modest and manageable. As a result, compared with the pre-Global Financial Crisis era, EM economies are absorbing stress more effectively today. Capital outflows have been muted, currency weakness has translated into less inflation, and the overall impact on growth has generally been smaller. In other words, EM is behaving less like a fragile, pro-cyclical bloc and more like a set of economies anchored by stronger and more credible policy frameworks.

This has led to improving credit ratings and record levels of positive outlooks, supporting asset class performance. Even Frontier markets, often seen as higher risk, now have manageable current account deficits and robust foreign currency reserves, further underpinning resilience.

Mid-cycle with manageable external financing needs

Click image to enlarge

Source: HSBC Asset Management, IMF, WEO, JP Morgan. As of December 2025.

EM index countries’ ratings outlook skew

Click image to enlarge

Source: HSBC Asset Management, Moody's, S&P, Fitch, January 2026.

For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way, HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target.

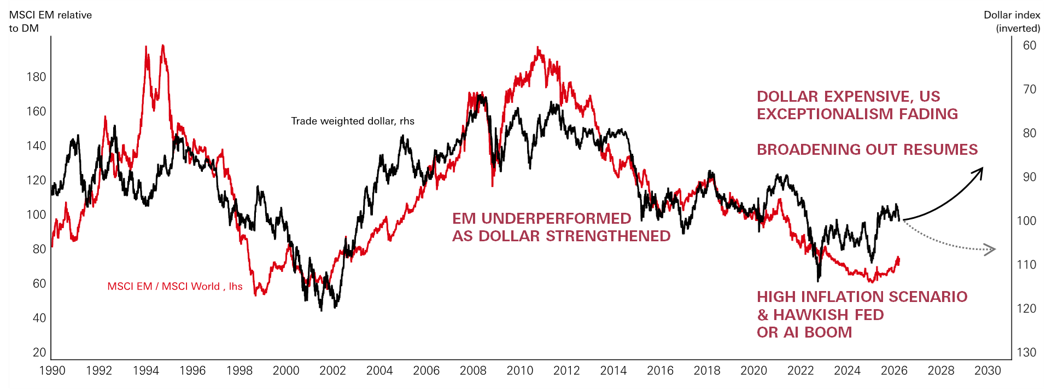

3. US Dollar trends and EM resilience

A weaker dollar—alongside an improving global liquidity cycle and a Federal Reserve that is cutting interest rates—tends to support emerging markets as an asset class. It can improve performance and encourage investors to re-engage with EM investment opportunities. This is broadly what we observed through 2025 and into January and February 2026, with a weaker dollar supporting renewed investor participation and a “broadening out” across markets.

More recently, in the context of the oil shock, dollar strength has re-emerged as an important theme and a challenge for emerging markets to navigate. However, early signs are encouraging, while the dollar has risen, public debt stocks that have been de-risked of currency mismatch, credible and independent central banks, and comfortable levels of foreign currency reserves have helped many parts of emerging markets have remained resilient. This is supportive of the view that the risk-adjusted return characteristics of the emerging market asset class have evolved.

Weaker dollar (black) correlates with strong EM (red)

Click image to enlarge

Past performance does not predict future returns.

Source: Refinitiv, MSCI, HSBC Asset Management, March 2026. The commentary and analysis presented in this document reflect the opinion of HSBC Asset Management on the markets, according to the information available to date. They do not constitute any kind of commitment from HSBC Asset Management. Consequently, HSBC Asset Management will not be held responsible for any investment or disinvestment decision taken on the basis of the commentary and/or analysis in this document. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target. Index returns assume reinvestment of all distributions and do not reflect fees or expenses.

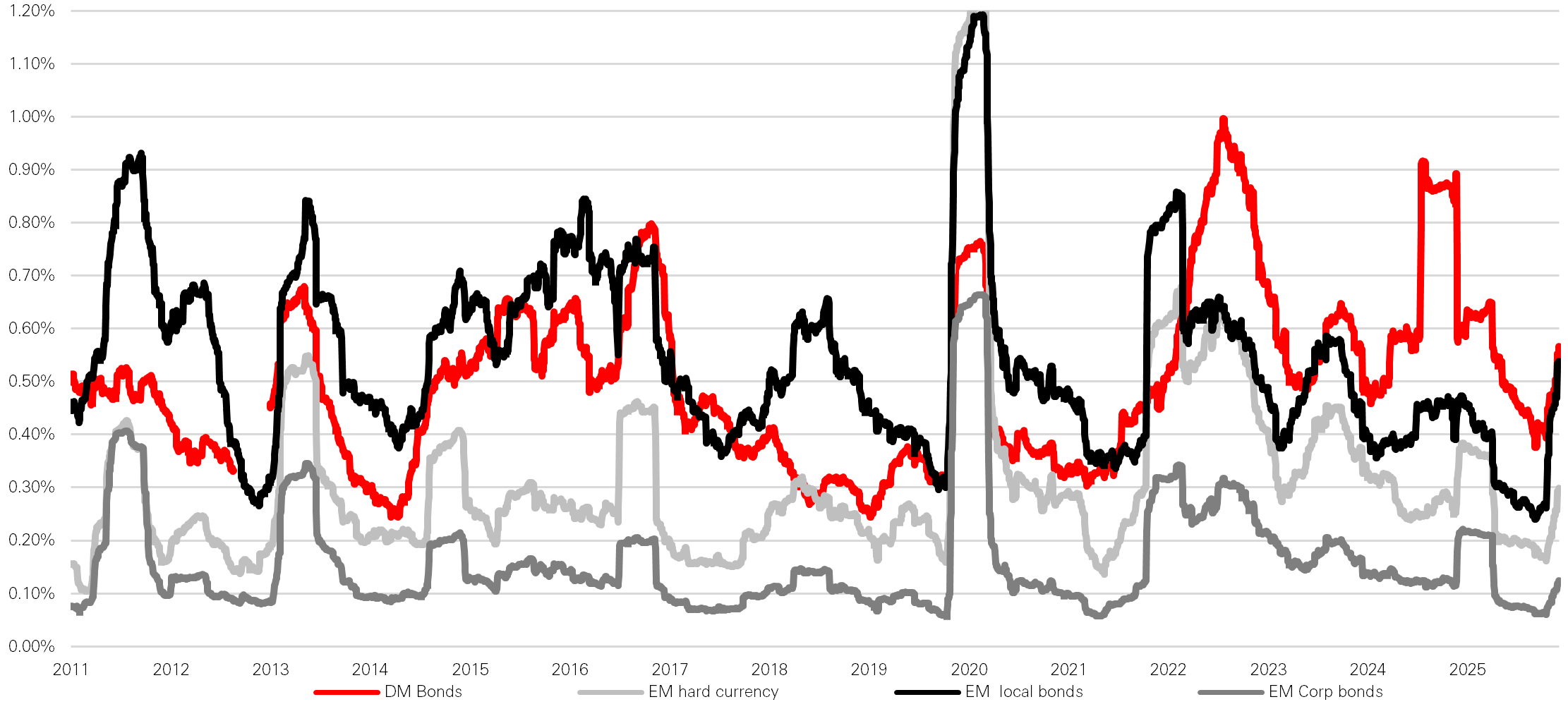

4. EM bonds are less volatile than DM bonds

Historically, emerging market bonds have been seen as vulnerable during global risk-off episodes, with capital outflows, inflation spikes, and financial stress. It was assumed volatility would be significantly higher than developed market (DM) rates volatility—often multiples higher during periods of stress. Even amid current market turmoil, the improved fundamental picture for emerging market bonds is evidenced by the EMD asset classes displaying lower volatility than their DM counterparts.

In practical terms, EM is behaving less like a fragile bloc and more like a set of economies supported by stronger policy frameworks and improved credibility. This matters for EMD because it changes the distribution of outcomes in volatile periods. Lower inflation pass-through can reduce the probability of forced, pro-cyclical tightening; muted outflows can reduce the likelihood of disorderly FX moves; and smaller growth impacts can support fiscal trajectories and credit quality.

Bond market total return volatility (90 day rolling measure)

5. Divergence and differentiation

Emerging market economies are now far more resilient to global shocks than in previous decades, but the range of outcomes across countries is widening significantly. The effects of a US$10 oil price shock, for instance, are highly asymmetric: energy importers experience headwinds to growth and upward pressure on inflation, while commodity-linked exporters often enjoy improved external balances and stronger terms of trade. Countries such as Brazil and Colombia have reaped the benefits of higher oil prices, and currencies in other oil-exporting economies—including the Kazakh tenge and Argentine peso—have remained supported despite challenging global conditions.

Importantly, even some oil-importing regions in Central America and the Caribbean have bolstered their resilience. This has been achieved through IMF-supported programmes that anchor structural reforms, investments in renewable energy that reduce oil import bills, and the adoption of orthodox macroeconomic frameworks. As a result, these economies are demonstrating greater stability than in previous adverse terms-of-trade cycles.

Elsewhere, tech-oriented markets like South Korea and Taiwan are riding the wave of global demand for artificial intelligence, while India—despite being a major energy importer—continues to benefit from robust structural growth drivers. This diversity of exposures within emerging markets helps to smooth overall volatility, as weakness in one segment can be offset by strength in another.

The key takeaway is clear: Emerging markets can no longer be approached as a single, uniform asset class. Success now depends on careful, country-by-country and segment-by-segment differentiation, rather than treating EM as a monolithic “beta” trade.

Past performance does not predict future returns.

Source: Refinitiv, MSCI, HSBC Asset Management, March 2026. The commentary and analysis presented in this document reflect the opinion of HSBC Asset Management on the markets, according to the information available to date. They do not constitute any kind of commitment from HSBC Asset Management. Consequently, HSBC Asset Management will not be held responsible for any investment or disinvestment decision taken on the basis of the commentary and/or analysis in this document. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index.

Outlook for EMD asset classes

- EM Hard Currency: Over the years, a commitment to sound fiscal management has bolstered their resilience. Credit rating agencies have increasingly recognized these improvements, with the average rating for EM sovereigns rising and issuers enjoying favorable outlooks, which has contributed to the lower volatility and stable credit spreads recently. In addition, the carry of EM bonds remains attractive thanks to a higher-for-longer rates environment in the US, meaning asset allocators are not too late to join the EMD trade.

- EM Local Currency. A weaker US dollar, partly driven by questions around the safe haven status of US assets and US exceptionalism, could further boost EM currency returns. We see three primary drivers for the weakening US dollar trend and continued support of the EMD currency trade:

- A Federal Reserve that is biased to ease policy, maintaining downward pressure on front end US yields;

- The relative quality differential between EM and DM with regard to lower debt ratios and more sustainable debt service capacity, external account improvements, and positive credit ratings momentum; and

- Ongoing negotiation of bilateral trade deals between the US and its major trading partners that increasingly offset tariffs in exchange for currency appreciation.

- EM Corporate debt: Continues to offer diversification, resilience, and attractive yields. In addition, EM companies demonstrate stronger financial discipline compared to their DM peers, on average. Corporate debt has a lower duration profile, and as a result, performance is less correlated to US Treasuries than other asset classes. Their higher yields, coupled with the prospect of capital gains from cyclically declining interest rates, present a prospect for strong returns.

Conclusion

Emerging Markets Debt has evolved into a more resilient and differentiated asset class, supported by stronger fiscal discipline, improved external buffers, and more credible monetary policy frameworks across many countries. Recent episodes of higher oil prices, a stronger US dollar, and elevated global rates—conditions that historically would have triggered broad-based stress—have instead highlighted a more muted EM response, reinforcing the improved quality of the asset class abroad-baseds well as the importance of country-by-country and segment-by-segment selection.

With attractive yields, improving credit quality, and diversification benefits across hard currency sovereigns, local currency markets, and corporates, EMD offers multiple ways to participate in a shifting macro environment. While country-specific risks remain and dispersion is widening, the combination of stronger fundamentals and a more mature opportunity set supports the case for EMD as a strategic building block in global portfolios.

Source: HSBC Asset Management, March 2026

For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way, HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target.