Beyond Developed Markets: The Case for Emerging Market Local Debt Today

Executive Summary

- High real yields: EM local debt offers high real income (inflation-adjusted) versus developed country bonds

- Policy credibility: Many EM central banks reacted early and decisively to anchor inflation expectations during the post-pandemic inflation shock

- Attractive EM FX Valuations: EM FX is relatively inexpensive versus the US dollar and external balances are improving

- More resilient EM: Stronger EM institutions and policy frameworks have improved durability versus past cycles

- Multiple Sources of Returns: EM local debt offers high carry, EM local bond duration, and EM currency exposure, offering an attractive risk/reward profile, especially for diversified active strategies

Emerging market (EM) local currency debt has become an increasingly compelling investment opportunity in the global fixed income landscape that has changed dramatically over the last few years. While developed market central banks have raised interest rates sharply from their post-pandemic lows, the improvement in nominal yields has not always translated into attractive real income once inflation is considered. At the same time, many developed market economies are dealing with deteriorating fiscal positions, aging populations, and weaker long term growth prospects. Against this backdrop, EM local debt stands out as an area where investors can still find high real yields, improving fundamentals, and diversified sources of return.

Source: HSBC Asset Management. The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and not guaranteed in any way.

A New Era for EM Local Debt

A key shift in this cycle has been the behavior of EM central banks. Historically, they were often perceived as lagging their developed markets peers—slow to respond to inflation and quick to ease policy at the expense of currency and price stability. However, in the most recent cycle, many EM central banks reacted earlier and more aggressively than the Federal Reserve (Fed) or the European Central Bank (ECB) when inflation surged. Policy rates in several EM economies were raised decisively to anchor inflation expectations, in some cases into double digits. As a result, inflation in EM economies normalized more rapidly than in many developed market economies, creating a compelling opportunity in EM local bonds: high real income with potential for capital gains as yields decline alongside monetary policy easing in developed market economies.

Why has the pattern changed? EM central banks can act more independently of the Fed and the ECB than in past cycles due to the following factors:

- Increased financial depth – larger pension pools serving as dedicated buyers of local debt, underpinning liquidity and volumes

- Greater financial sophistication – larger financial sectors, with banks and insurance companies acting as intermediaries that improve monetary policy transmission

- De-dollarization – a higher money supply relative to GDP and a shift in savings and wealth away from hard currencies and into local-currency assets

We believe this means we are not going back to the previous world, and EM currencies and interest rates will behave more idiosyncratically going forward.

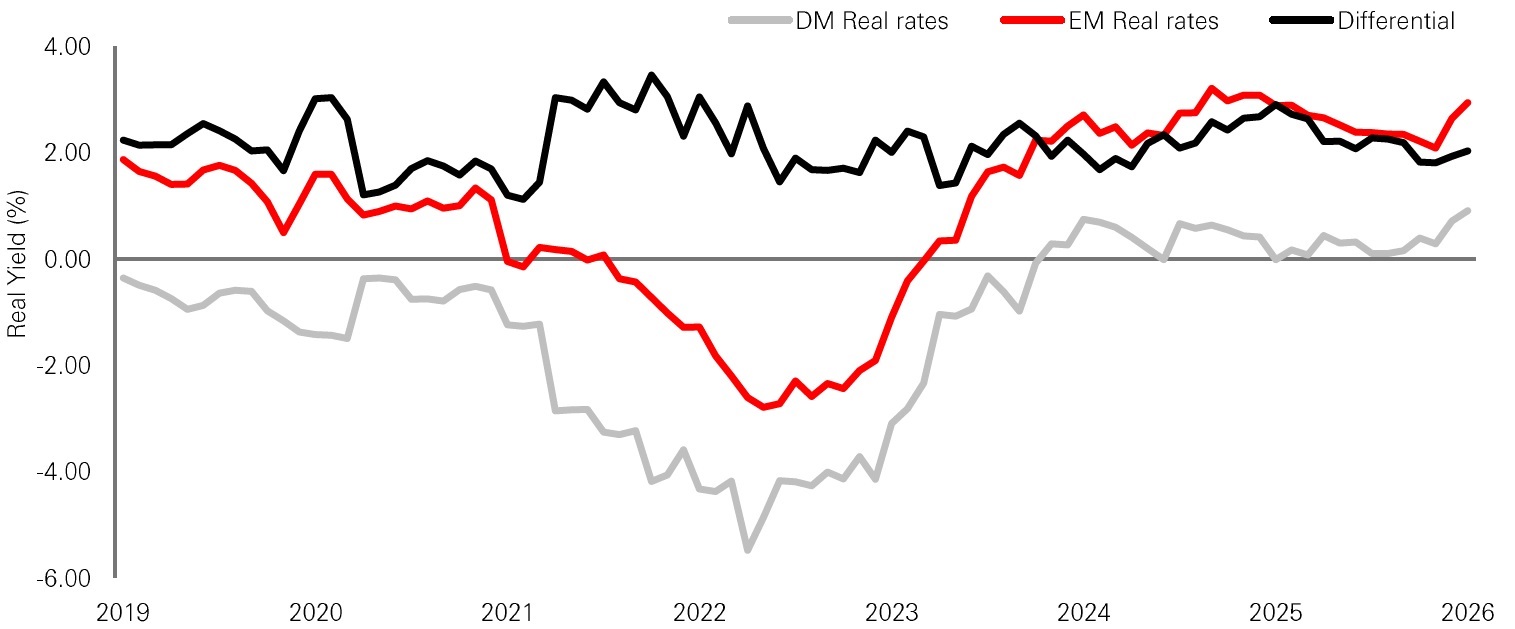

Restrictive monetary policy in many developed market economies has caused global yields to remain elevated. In comparison, the carry of EM local bonds is attractive and can be a powerful driver of returns over time. High carry can provide a margin of safety, compensating investors for taking on credit, liquidity, and political risk, and offering a cushion against adverse shocks in global rates or risk sentiment.

EM Premium over DM

Click to enlarge image

Sources: HSBC Asset Management, Bloomberg, JP Morgan, as of 31 March 2026.

Source: Bloomberg, HSBC Asset Management as of 31 March 2026. The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. The level of yield is not guaranteed and may rise or fall in the future.

Multiple drivers of return

EM currency exposure is another source of potential returns when investing in EM local debt. After a decade of US dollar strength, many EM currencies are relatively inexpensive. Although we saw the US dollar begin to weaken last year, it is still well off historical lows and continued weakening could be supportive for EM FX. Against this backdrop, external balances have improved in many EM countries, as can be seen with shrinking current account deficits and higher levels of foreign exchange reserves. EM FX may have room to appreciate over the medium term if EM fundamentals continue on this improving trend and the US dollar experiences further weakness.

Weaker dollar (black) correlates with strong EM (red)

Click to enlarge image

Source: Refinitiv, MSCI, HSBC Asset Management, March 2026.

Policy Improvements and Growth Drivers

The structural backdrop in EM has also evolved meaningfully. Today's EM local debt is not the same asset class it was 20 years ago. Many EM countries have strengthened their institutional and policy frameworks, granting greater independence to central banks, adopting explicit inflation targeting regimes, and introducing more disciplined fiscal and debt management practices. These changes have helped anchor inflation expectations, reduced the incidence of extreme inflation episodes, and increased investor confidence in local bond markets and currencies. As a result, EM economies have become more resilient to periods of US dollar strength, higher global interest rates, and episodes of global risk aversion. While risks remain in specific countries, the overall quality and resilience of the asset class have improved.

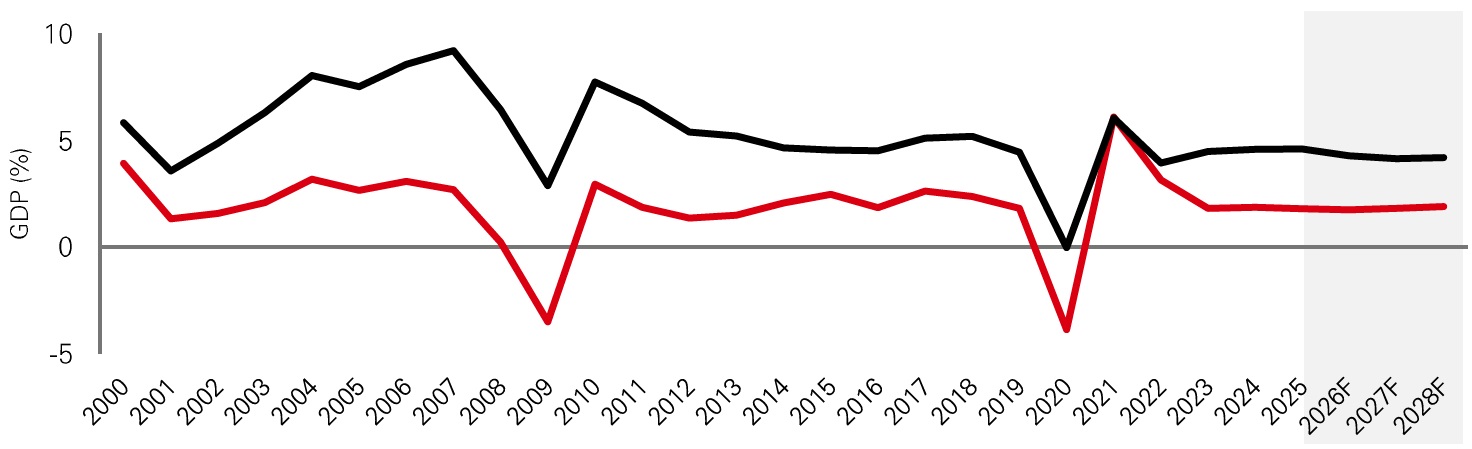

Looking ahead, the macroeconomic case for EM local debt remains robust. Many EM economies continue to offer higher long term growth potential than their developed counterparts, supported by younger and growing populations in some regions, ongoing urbanization and industrialization, productivity catch up, and structural reforms. On average, EM economies have delivered around 3 per cent higher GDP growth than Developed Markets. Higher trend growth can support better debt sustainability, healthier tax bases, and stronger domestic savings, which in turn deepen local capital markets. Over time, stronger growth and productivity can also support real currency appreciation, reinforcing the case for local currency exposure.

The post-pandemic global inflation shock of 2021-2022 served as a major test for EM central banks. Many passed that test by responding early and decisively with meaningful rate hikes. Credible monetary policy should give investors greater confidence that EM central banks will keep inflation expectations anchored and high real yields are not a precursor to renewed instability, but instead an attractive value proposition.

Annual GDP: Developed vs. Emerging Markets

Click to enlarge image

Source: Bloomberg, as of April 2026

Source: Bloomberg, HSBC Asset Management as of 31 March 2026. The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and not guaranteed in any way.

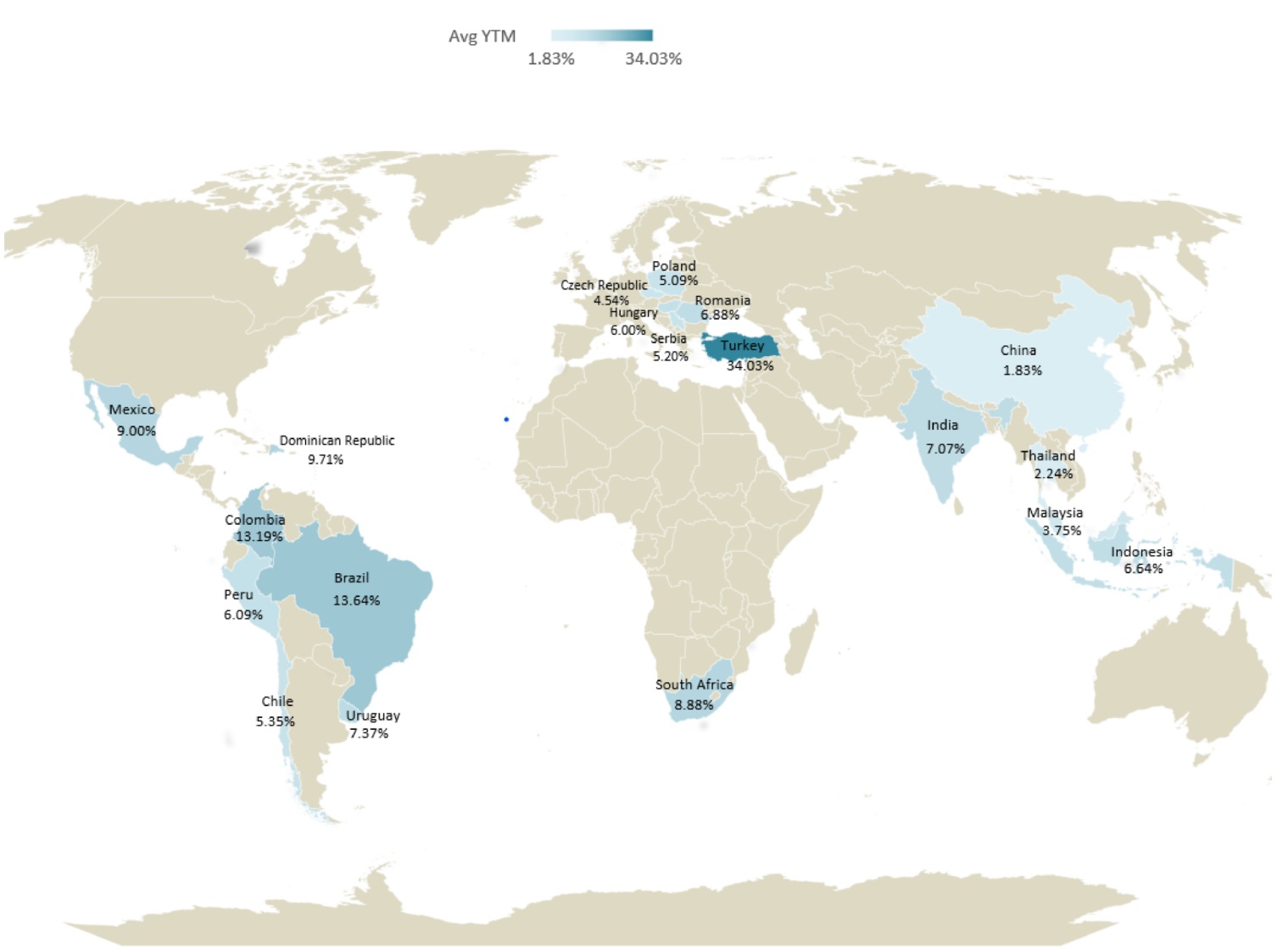

Average Yield to Maturity of countries in our EM local debt portfolio

Click to enlarge image

Sources HSBC Asset Management, Bloomberg, as of 24 April 2026

Conclusion

EM local currency debt stands out in today's markets by offering high real yields and attractive carry, delivering meaningful income and a margin of safety for investors. Improved policy and institutional frameworks have strengthened resilience, while exposure to a range of relatively inexpensive currencies adds diversification. Structural fundamentals are notably stronger than in previous cycles, further supporting the asset class.

Risks remain and should not be understated, but current valuations provide ample compensation—especially when accessed through diversified, actively managed portfolios. For investors willing to look beyond traditional developed market bonds, EM local debt presents a compelling opportunity to enhance income, diversify risk, and participate in the long-term growth and convergence of emerging economies.

To learn more about HSBC's offerings on Emerging Market Local Debt, please contact your local HSBC representative.

Source: HSBC Asset Management as of 31 March 2026. The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. The level of yield is not guaranteed and may rise or fall in the future.