Islamic Funds Monthly Market Overview - June

Monthly Market Overview - Equities

- Global equities delivered solid gains in May as investors took comfort from robust earnings and ongoing momentum in technology. The strongest support continued to come from the rapid expansion of AI-related investment, which has kept demand for semiconductors elevated and underpinned expectations for further profit growth. Risk appetite also improved as markets judged that Middle East tensions were less likely to spill over into broader economic disruption

- Equity market gains remained concentrated in tech-heavy markets such as the US and, within emerging markets, South Korea and Taiwan. In the second half of the month, participation broadened, pointing to a potential widening of the rally beyond the AI leadership. Japan also performed strongly, supported by AI-related technology names, while the UK lagged other developed markets due to its lower exposure to the sector. Emerging markets outperformed developed markets, driven by the tech-heavy Asian markets

- Within Islamic global equities Technology was the largest contributor while Energy detracted slightly. Region wise, North America drove performance during the month, while EMEA and Asia also contributed to performance. Within specific stock names, Micron Technology, Apple and SK Hynix drove returns, while Walmart and Alphabet weighed on performance

- Within Islamic EM equities, South Korea and Taiwan, contributed the most to performance. IT drove performance from a sector perspective, while Consumer Staples were a drag on returns. Within specific securities, SK Hynix and Samsung drove returns, while Xiaomi Corporation and Reliance Industries weighed on performance

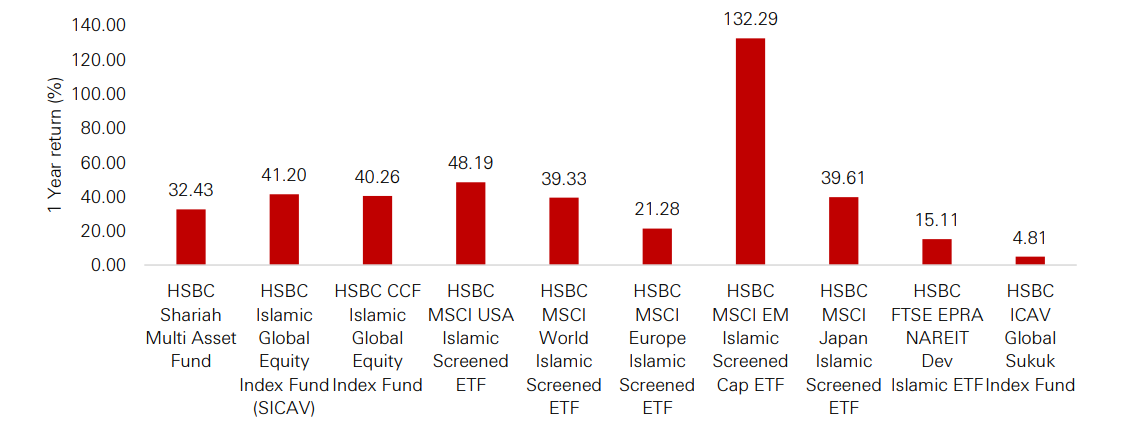

Chart 1: 1 Year Fund performance (Gross of fees)

Click the image to enlarge

Past performance does not predict future returns. Source: Bloomberg, LSEG Refinitiv, HSBC Asset Management as of 31 May 2026. Past performance is shown gross of fees, meaning any potential returns will be reduced by the deduction of investment management fees and any other expenses incurred. Returns denominated in USD and may vary with fluctuations in the exchange rate. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Shariah investment restrictions may result in the funds performing less well than funds with similar objectives which are not subject to these restrictions. The views expressed above were held at the time of preparation and are subject to change without notice

Fixed Income / Sukuk

- Across global fixed income markets, yields remained volatile amid shifting expectations around a potential US–Iran peace agreement but growing optimism around an eventual resolution appeared to support a gradual decline in rates towards month-end. Credit markets were positive for the month, and spreads tightened due to investors focusing on growth remaining resilient despite inflation concerns

- The US 10-year Treasury rose over the month by 7bps at 4.44 per cent in May, the German Bund fell by 10bps to 2.94 per cent and the UK 10-year Gilt also fell by 20bps to 4.81 per cent. Investment grade global corporate spreads tightened by 5bps at 0.76 per cent, global high yield corporate spreads tightened by 11bps to 2.77 per cent

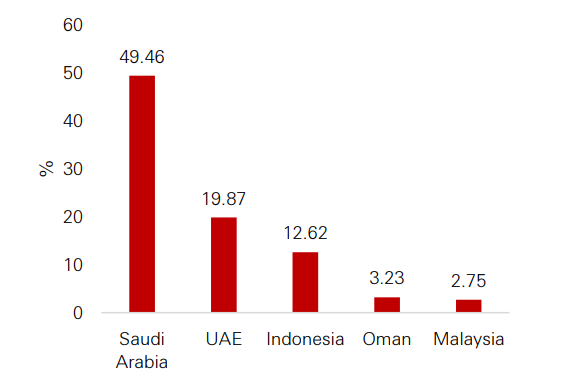

- The FTSE IdealRatings Sukuk Index holds investment grade Sukuks, with an average coupon of 4.69 per cent and average maturity of 5.83 years. Top exposures are to Saudi Arabia, UAE and Indonesia

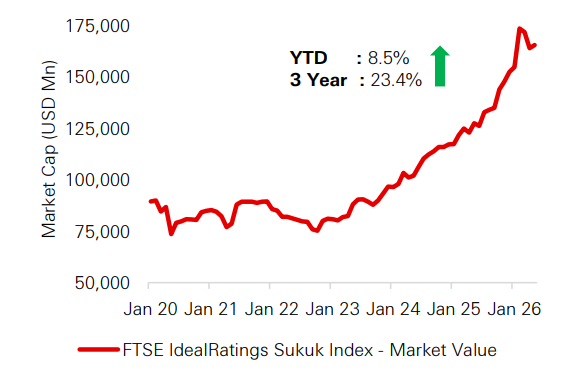

- Sukuk issuance continues to be strong in 2026

- Sukuk issuance continues to grow steadily, signalling growing interest in the asset class. Issuance growth rates are expected to moderate this year as investors keep a close eye on developments on the Middle East war

Chart 2: Country exposure (Top 5)

Click the image to enlarge

Chart 3: Market Value continues to grow

Click the image to enlarge

Commodities

- In commodity markets, brent crude fell by nearly 20 per cent—its steepest monthly decline since March 2020—despite the ongoing geopolitical stalemate in the Middle East. Gold prices also fell for a third consecutive month, weighed down by a stronger US dollar and shifting interest rate expectations

Currencies

- The US dollar strengthened against both Sterling and the euro, supported by shifting expectations for the Fed, resilient US economic data, and intermittent geopolitical tensions. Ongoing concerns about slowing growth and higher inflation in the Eurozone weighed on the euro, while domestic political uncertainty pressured Sterling

Past performance does not predict future returns. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. The views expressed above were held at the time of preparation and are subject to change without notice. Shariah investment restrictions may result in the funds performingless well than funds with similar objectives which are not subject to these restrictions. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index.

Source: Bloomberg, LSEG Refinitiv, HSBC Asset Management as of 31 May 2026.

Multi Asset Investment Team Views and Portfolio Positioning

- Outlook: While there are signs of progress towards reopening the Strait of Hormuz, geopolitical risk remains elevated. With oil prices still elevated and supply constraints for some other commodities, inflation pressures are likely to persist, acting as a headwind to growth. However, the situation remains fluid with potential for wide ranging outcomes. Our baseline scenario is for more balanced, trend-like US economic growth. Policy uncertainty remains high and real household income growth is weak, which should weigh on demand. Despite this, we do not anticipate a sharp slowdown, as investment in AI-related capital expenditure continues to provide strong support. We assume the oil price shock moderates, although tariffs could still add inflation pressure in the US and we expect global growth to converge, with inflation falling further outside the US

- Portfolio Positioning: Markets remain supported by strong corporate profits and AI-related investment, but the Middle East energy shock and a more volatile interest rate outlook keep macroeconomic risks elevated. Given this backdrop, we keep overall equity exposure close to neutral at this stage

- We prefer higher gold exposure, as we view the recent headwind in gold price as temporary and used the weakness to add exposure at more attractive levels. We remain overweight emerging markets equities, where we further added in May, as our indicators for the region have improved more, helped by supportive financial conditions and continued strength in parts of Asian technology markets (e.g., Korea and Taiwan). During the month we also moved underweight Europe, due to sentiment being weighed down by higher oil prices and likelihood of rate hikes. We prefer Japanese equities, where we remain focused on its resilient economic growth and the potential for fiscal stimulus to boost growth

- In May we also closed the underweight to US equities, as we become less pessimistic on the region, with indicators for the region strengthening, including momentum, economic growth and labour market. During the month we reduced the gold overweight on weaker momentum

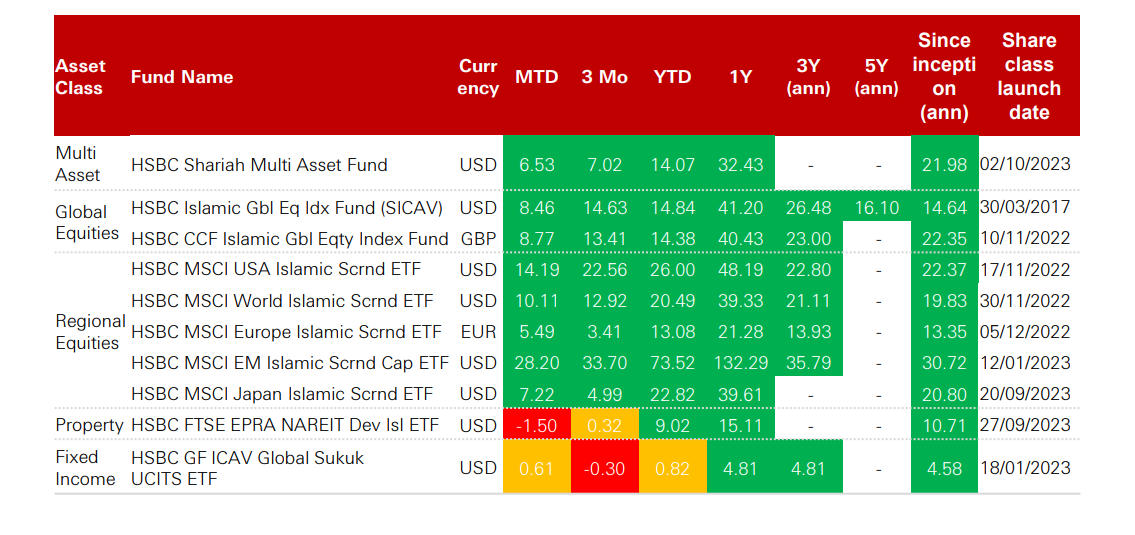

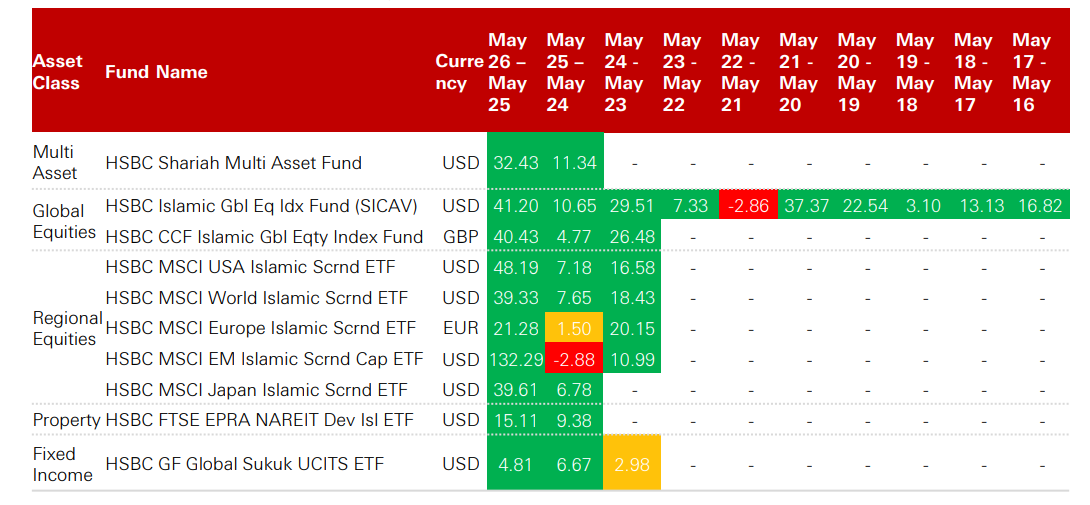

HSBC Islamic Product Suite - Returns (Gross of Fees per cent)

Click the image to enlarge

Past performance does not predict future returns. . For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. The views expressed above were held at the time of preparation and are subject to change without notice. Past performance is shown gross of fees, meaning any potential returns will be reduced by the deduction of investment management fees and any other expenses incurred. Returns not denominated in GBP may vary with fluctuations in the exchange rate. Shariah investment restrictions may result in the funds performing less well than funds with similar objectives which are not subject to these restrictions.

Source: HSBC Asset Management as of 31 May 2026.

HSBC Islamic Product Suite - Rolling 1 Year Returns (Gross of fees per cent)

Click the image to enlarge

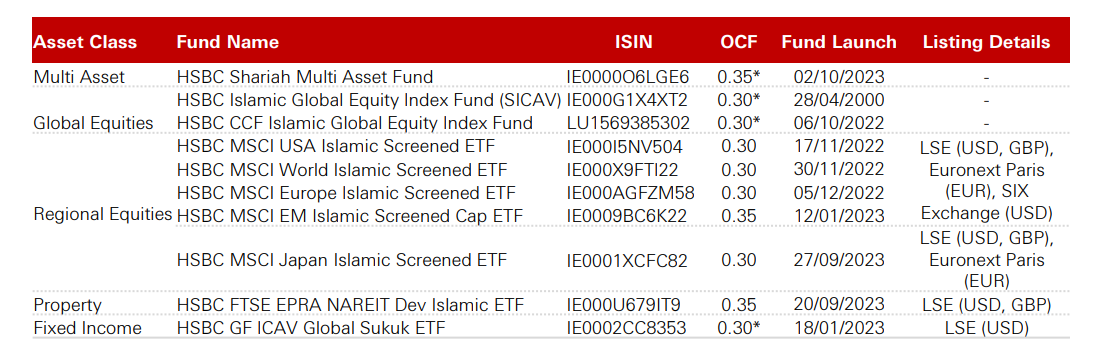

Key Information

Click the image to enlarge

* For more information including all available share classes, please contact your relationship manager.

Key Risks

The value of an investment in the portfolios and any income from them can go down as well as up and as with any investment you may not receive back the amount originally invested.

- Counterparty Risk: The possibility that the counterparty to a transaction may be unwilling or unable to meet its obligations

- Exchange Rate Risk: Changes in currency exchange rates could reduce or increase investment gains or investment losses, in some cases significantly

- Index Tracking Risk: To the extent that the Fund seeks to replicate guarantee that its composition or performance will exactly match that of the target index at any given time (“tracking error”)

- Investment Leverage Risk: Investment Leverage occurs when the economic exposure is greater than the amount invested, such as when derivatives are used. A Fund that employs leverage may experience greater gains and/or losses due to the amplification effect from a movement in the price of the reference source

- Liquidity Risk: Liquidity Risk is the risk that a Fund may encounter difficulties meeting its obligations in respect of financial liabilities that are settled by delivering cash or other financial assets, thereby compromising existing or remaining investors.

- Operational Risk: Operational risks may subject the Fund to errors affecting transactions, valuation, accounting, and financial reporting, among other things.

- Sustainability risk: Means an environmental, social or governance event or condition that, if it occurs, could cause an actual or potential material negative impact on the value of the investment.

Further information on the potential risks can be found in the Key Investor Information Document (KIID) and/or the Prospectus of the relevant Fund before making any final investment decisions

Past performance does not predict future returns. Past performance is shown gross of fees, meaning any potential returns will be reduced by the deduction of investment management fees and any other expenses incurred. Returns not denominated in GBP may vary with fluctuations in the exchange rate. Shariah investment restrictions may result in the funds performing less well than funds with similar objectives which are not subject to these restrictions.

Source: HSBC Asset Management as of 31 May 2026.

Important Information

For Professional Clients only and should not be distributed to or relied upon by Retail Clients.

The material contained herein is for marketing purposes and is for your information only. This document is not contractually binding nor are we required to provide this to you by any legislative provision. It does not constitute legal, tax or investment advice or a recommendation to any reader of this material to buy or sell investments. You must not, therefore, rely on the content of this document when making any investment decisions

This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe to any investment

The contents are confidential and may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. This presentation is intended for discussion only and shall not be capable of creating any contractual or other legal obligations on the part of HSBC Global Asset Management (UK) Limited or any other HSBC Group company

The document is based on information obtained from sources believed to be reliable but which have not been independently verified. HSBC Global Asset Management (UK) Limited and HSBC Group accept no responsibility as to its accuracy or completeness. Care has been taken to ensure the accuracy of this presentation but HSBC Global Asset Management (UK) Limited accepts no responsibility for any errors or omissions contained therein

This document and any issues or disputes arising out of or in connection with it (whether such disputes are contractual or non-contractual in nature, such as claims in tort, for breach of statute or regulation or otherwise) shall be governed by and construed in accordance with English law

Any views expressed were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way. HSBC Global Asset Management (UK) Limited accepts no liability for any failure to meet such forecast, projection or target.

HSBC ETFs is a sub-fund of HSBC ETFs plc (“the Company”), an investment company with variable capital and segregated liability between sub-funds, incorporated in Ireland as a public limited company, and is authorised by the Central Bank of Ireland. The company is constituted as an umbrella fund, with segregated liability between sub-funds. Shares purchased on the secondary market cannot usually be sold directly back to the Company. Investors must buy and sell shares on the secondary market with the assistance of an intermediary (e.g. a stockbroker) and may incur fees for doing so. In addition, investors may pay more than the current Net Asset Value per share when buying shares and may receive less than the current Net Asset Value per Share when selling them. UK based investors in HSBC ETFs plc are advised that they may not be afforded some of the protections conveyed by the Financial Services and Markets Act (2000), (“the Act”). The Company is recognised in the United Kingdom by the Financial Conduct Authority under section 264 of the Act. The shares in HSBC ETFs plc have not been and will not be offered for sale or sold in the United States of America, its territories or possessions and all areas subject to its jurisdiction, or to United States Persons. Affiliated companies of HSBC Global Asset Management (UK) Limited may make markets in HSBC ETFs plc. All applications are made on the basis of the current HSBC ETFs plc Prospectus, relevant Key Investor Information Document (“KIID”), Supplementary Information Document (SID) and Fund supplement, and most recent annual and semi-annual reports, which can be obtained upon request free of charge from HSBC Global Asset Management (UK) Limited, 8 Canada Square, Canary Wharf, London, E14 5HQ. UK, or from a stockbroker or financial adviser. The indicative intra-day net asset value of the sub-fund[s] is available on at least one major market data vendor terminal such as Bloomberg, as well as on a wide range of websites that display stock market data, including www.reuters.com. Investors and potential investors should read and note the risk warnings in the prospectus, relevant KIID and Fund supplement (where available) and additionally, in the case of retail clients, the information contained in the supporting SID.

HSBC ISLAMIC FUNDS - HSBC ISLAMIC GLOBAL EQUITY INDEX FUND is a sub-fund of the HSBC Islamic Funds, a Luxembourg domiciled Société d'investissement à Capital Variable (SICAV). UK based investors in HSBC Islamic Funds are advised that they may not be afforded some of the protections conveyed by the provisions of the Financial Services and Markets Act 2000. HSBC Islamic Funds is recognised in the United Kingdom by the Financial Conduct Authority under section 264 of the Act. The shares in HSBC Islamic Funds have not been and will not be offered for sale or sold in the United States of America, its territories or possessions and all areas subject to its jurisdiction, or to United States Persons. All applications are made on the basis of the current HSBC Islamic Funds Prospectus, Key Investor Information Document (KIID), Supplementary Information Document (SID) and most recent annual and semi-annual reports, which can be obtained upon request free of charge from HSBC Global Asset Management (UK) Limited, 8 Canada Square, Canary Wharf, London, E14 5HQ. UK, or the local distributors. Investors and potential investors should read and note the risk warnings in the prospectus and relevant KIID and additionally, in the case of retail clients, the information contained in the supporting SID.

Shariah investment restrictions may result in the funds performing less well than funds with similar objectives which are not subject to these restrictions.

HSBC Global Funds ICAV – Shariah Multi Asset Fund are sub-funds of HSBC Global Funds ICAV, an open-ended Irish Collective Asset-Management Vehicle which is constituted as an umbrella fund with segregated liability between sub-funds and with variable capital. This information does not constitute an offer or solicitation to buy shares in the Fund. Access to the information contained on this is restricted to persons who are residents of jurisdictions in which the distribution and the offering of shares in the Fund is authorised by the laws of the particular jurisdiction. The information contained herein is not for distribution to and does not constitute an offer to sell or solicitation of any offer to buy any securities in the United States of America to or for the benefit of any United States person(s). This material is not a solicitation, an offer, a recommendation or advice to buy or sell investment products, or to engage in other transactions. It explicitly does not take account the investment objectives, knowledge, experience or financial situation of any person. You should not act upon this information in any way and you are advised to obtain professional advice which does take account of your particular circumstances. You should carefully read the Fund’s Prospectus and Key Investor Information Document (the “KIID”), as well as consult with your advisers before making a decision to buy Fund shares. Investing in the Fund involves risk, including without limitation risk of total investment loss and other risks noted in the Fund’s Prospectus and KIID.

The HSBC UCITS Common Contractual Fund is an Open-Ended Umbrella Common Contractual Fund established under the laws of Ireland pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations 2011 (as amended). There can be no guarantee that the CCF or any of its Funds investment objectives will be achieved and investment results may vary substantially over time. Prospective Unit holders should carefully consider whether an investment in Units is suitable for them in light of their circumstances and financial resources and should carefully review the Prospectus and the relevant Supplement, including the sections entitled “Risk Factors” and “Portfolio Transaction and Conflicts of Interest”, before investing in the CCF. NATURAL PERSONS MAY NOT BE UNITHOLDERS IN THE CCF OR ANY OF ITS FUNDS. Investors and potential investors should read and note the risk warnings in the prospectus and relevant KIID.

The decision to invest in the fund should take account of all the characteristics or objectives as described in the prospectus or equivalent document. Detailed information for article 8 and 9 sustainable investment products, as categorised under the Sustainable Finance Disclosure Regulation (SFDR), including; description of the environmental or social characteristics or the sustainable investment objective; methodologies used to assess, measure and monitor the environmental or social characteristics and the impact of the selected sustainable investments and; objectives and benchmark information, can be found at: https://www.assetmanagement.hsbc.co.uk/en/intermediary/capabilities/esg-and-ri-strategies/sustainability-related-disclosures

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Where overseas investments are held the rate of currency exchange may also cause the value of such investments to fluctuate. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Stock market investments should be viewed as a medium to long term investment and should be held for at least five years. Any performance information shown refers to the past and should not be seen as an indication of future returns.

To help improve our service and in the interests of security we may record and/or monitor your communication with us. HSBC Global Asset Management (UK) Limited provides information to Institutions, Professional Advisers and their clients on the investment products and services of the HSBC Group.

Approved for issue in the UK by HSBC Global Asset Management (UK) Limited, who are authorised and regulated by the Financial Conduct Authority.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities provided through our local regulated entity, HSBC Global Asset Management (UK) Limited.

www.assetmanagement.hsbc.co.uk

Copyright © HSBC Global Asset Management (UK) Limited 2026. All rights reserved.

Content ID: D073914 ; Expiry Date: 31.12.2026