Emerging Markets Debt: Navigating oil shocks, rates and the US Dollar

A differentiated playbook for a more uncertain world

Emerging Markets (EM) have proved resilient to recent market shocks from surging oil prices and higher interest rates—a combination that would once have resulted in widespread stress. EM assets have become less sensitive to global ‘risk-off’ events, reflecting the fiscal discipline and improved fundamentals demonstrated by many EM countries over the past decade. Emerging Markets Debt (EMD) continues to offer a compelling investment opportunity, with attractive yields, solid credit quality, and a favourable risk–reward profile. The segment remains well positioned for growth in a shifting macroeconomic environment, offering investors both return potential and diversification benefits.

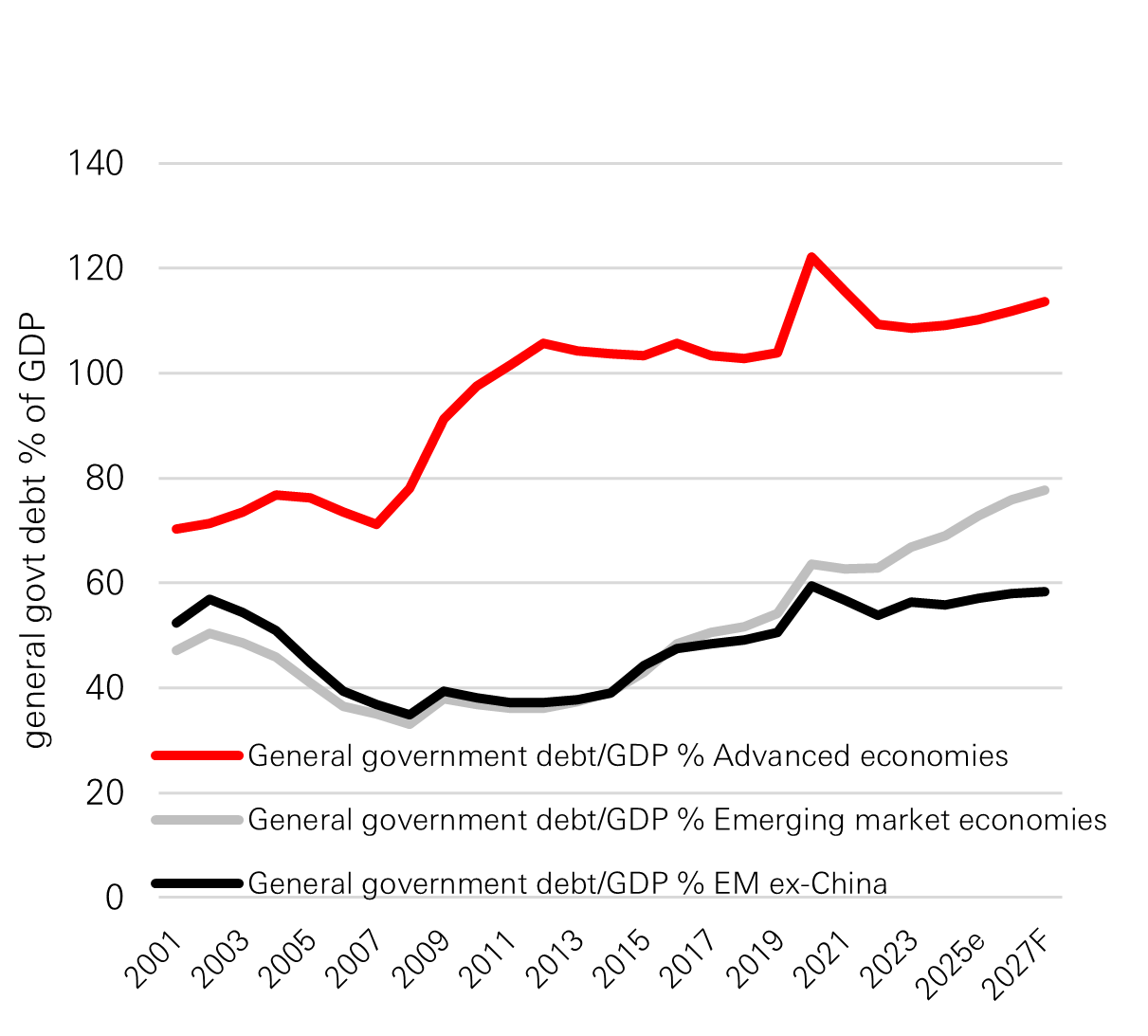

1. Fiscal discipline has led to improved fundamentals

Central to EM’s appeal is the marked improvement in fundamentals, driven by the fiscal discipline demonstrated by many emerging market (EM) countries. Global growth leadership is steadily shifting towards EM, with many countries exhibiting stronger trend growth, improving resilience, and more disciplined macroeconomic frameworks than in past cycles. Fiscal discipline is evident. Over the past 25 years, public debt dynamics have diverged sharply: EM countries have generally maintained stable balances, in contrast to the surge in advanced economies. In addition, a greater share of debt is now denominated in local currency, reducing overall currency risk and, in turn, volatility.

As a result, EM economies are better positioned to absorb external shocks than in earlier decades, supported by stronger external accounts, higher reserves, and more credible monetary policy.

Public debt has not grown at the same pace in EM

Click image to enlarge

Source: HSBC Asset Management, IMF, WEO, JP Morgan. As of December 2025, IMF WEO Oct 2025. Any views expressed were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way, HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target.

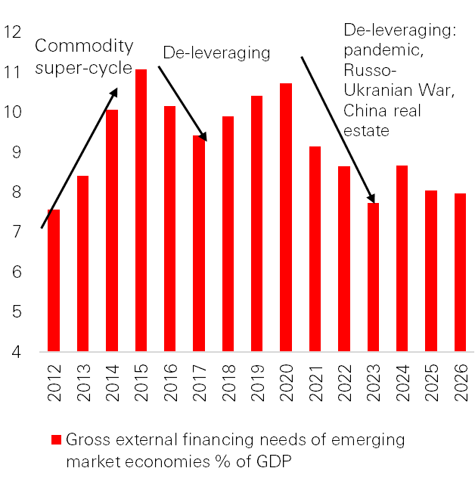

2. Fiscal discipline drives ratings momentum

Following the pandemic, EM sovereigns benefited from high nominal GDP growth to re-anchor fiscal accounts and deleveraging through debt restructurings and IMF programmes, helping to keep external financing needs modest and manageable. As a result, compared with the pre-Global Financial Crisis era, EM economies are absorbing stress more effectively today. Capital outflows have been muted, currency weakness has translated into less inflation, and the overall impact on growth has generally been smaller. In other words, EM is behaving less like a fragile, pro-cyclical bloc and more like a set of economies anchored by stronger and more credible policy frameworks.

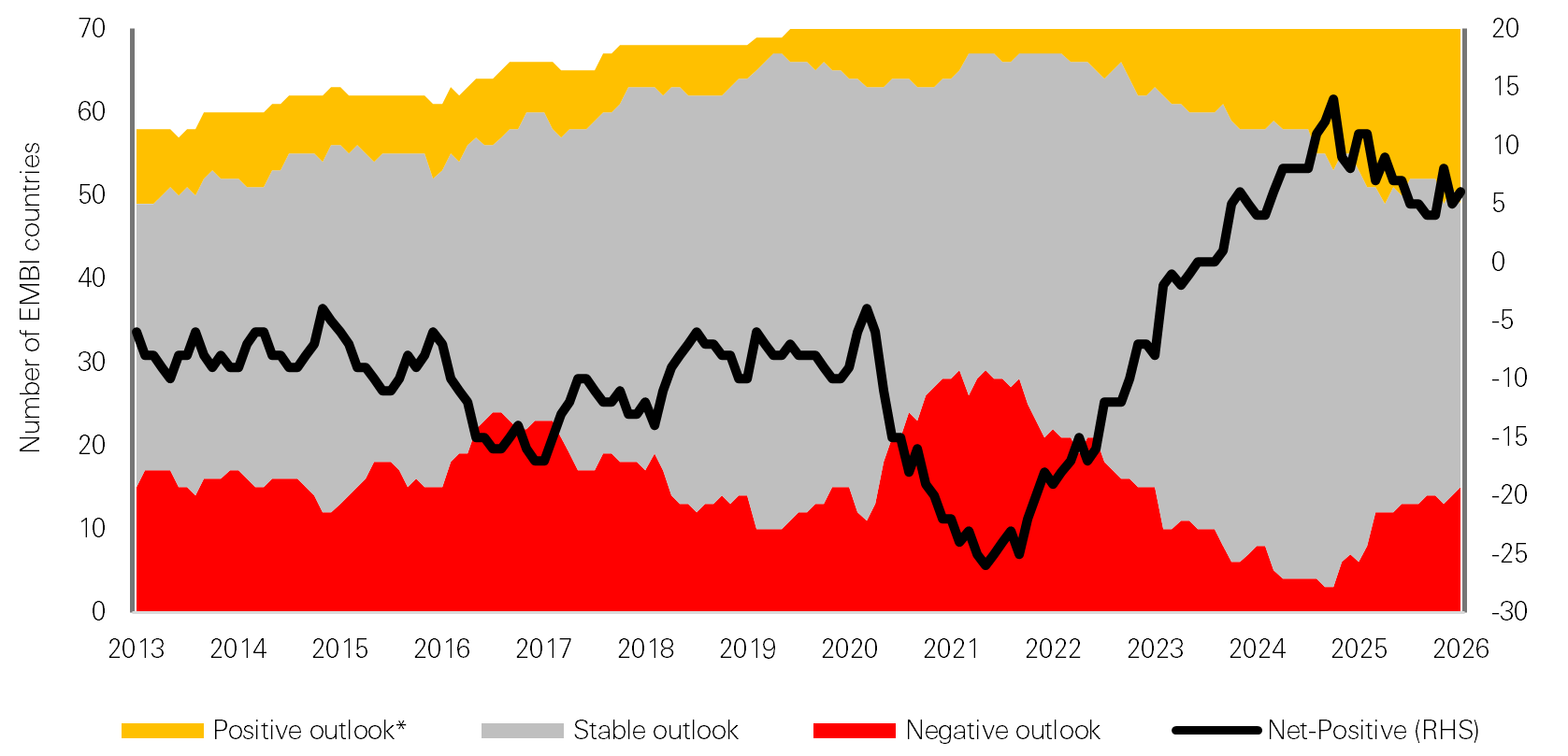

This has led to improving credit ratings and record levels of positive outlooks, supporting asset class performance. Even Frontier markets, often seen as higher risk, now have manageable current account deficits and robust foreign currency reserves, further underpinning resilience.

Mid-cycle with manageable external financing needs

Click image to enlarge

Source: HSBC Asset Management, IMF, WEO, JP Morgan. As of December 2025.

EM index countries’ ratings outlook skew

Click image to enlarge

Source: HSBC Asset Management, Moody's, S&P, Fitch, January 2026.

For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way, HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target.

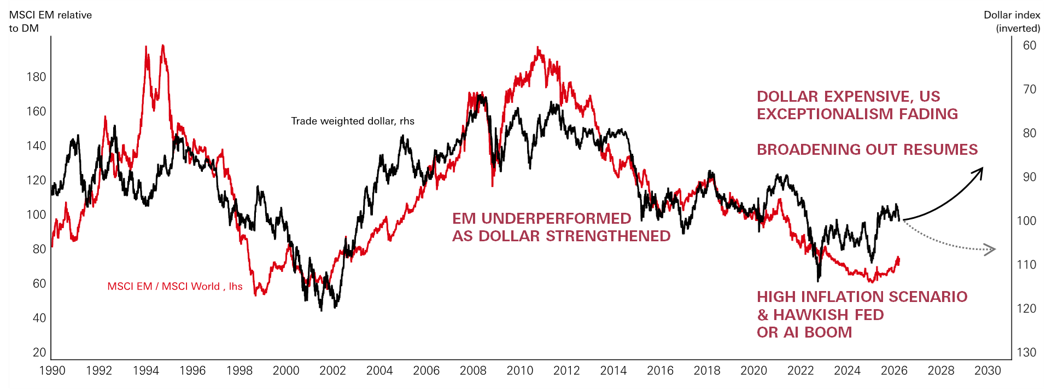

3. US Dollar trends and EM resilience

A weaker dollar—alongside an improving global liquidity cycle and a Federal Reserve that is cutting interest rates—tends to support emerging markets as an asset class. It can improve performance and encourage investors to re-engage with EM investment opportunities. This is broadly what we observed through 2025 and into January and February 2026, with a weaker dollar supporting renewed investor participation and a “broadening out” across markets.

More recently, in the context of the oil shock, dollar strength has re-emerged as an important theme and a challenge for emerging markets to navigate. However, early signs are encouraging, while the dollar has risen, public debt stocks that have been de-risked of currency mismatch, credible and independent central banks, and comfortable levels of foreign currency reserves have helped many parts of emerging markets have remained resilient. This is supportive of the view that the risk-adjusted return characteristics of the emerging market asset class have evolved.

Weaker dollar (black) correlates with strong EM (red)

Click image to enlarge

Past performance does not predict future returns.

Source: Refinitiv, MSCI, HSBC Asset Management, March 2026. The commentary and analysis presented in this document reflect the opinion of HSBC Asset Management on the markets, according to the information available to date. They do not constitute any kind of commitment from HSBC Asset Management. Consequently, HSBC Asset Management will not be held responsible for any investment or disinvestment decision taken on the basis of the commentary and/or analysis in this document. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target. Index returns assume reinvestment of all distributions and do not reflect fees or expenses.

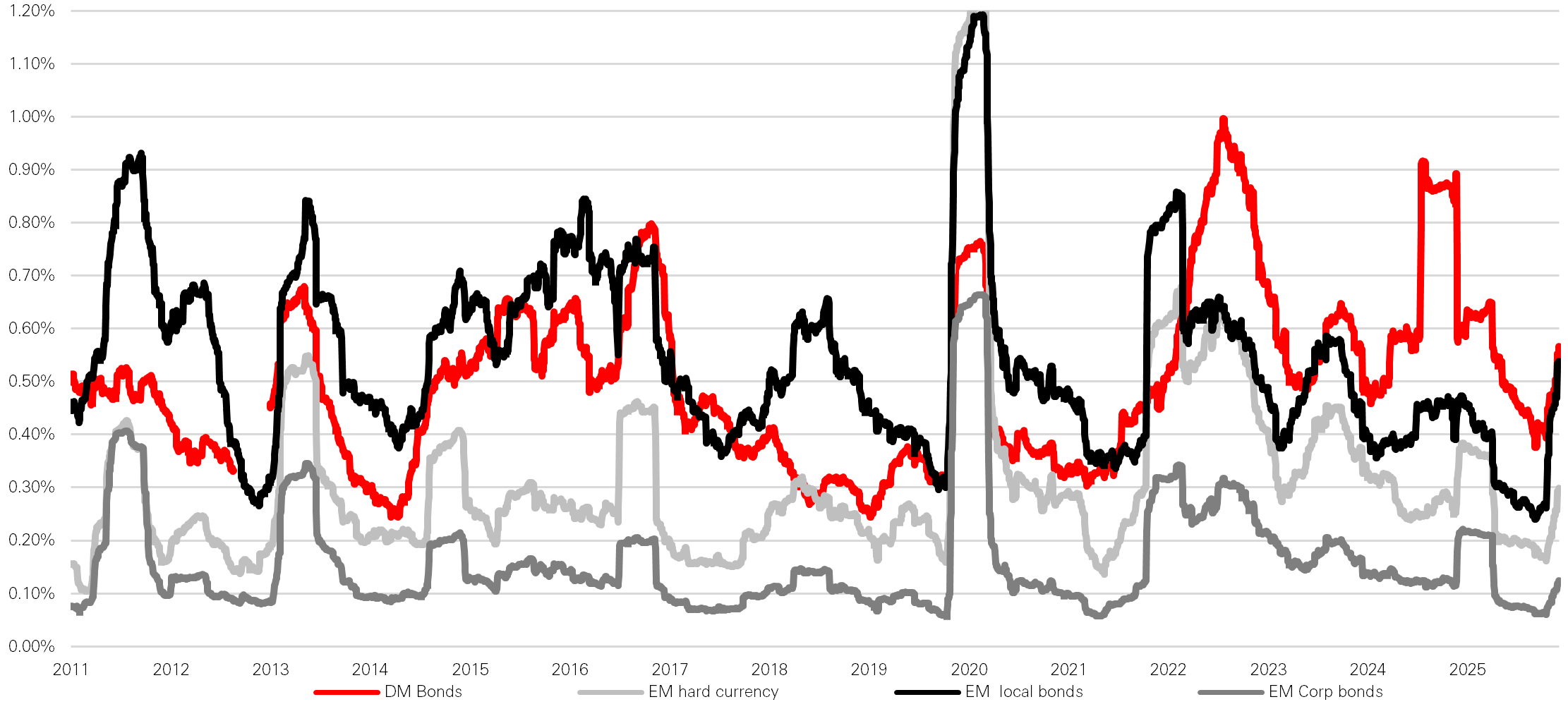

4. EM bonds are less volatile than DM bonds

Historically, emerging market bonds have been seen as vulnerable during global risk-off episodes, with capital outflows, inflation spikes, and financial stress. It was assumed volatility would be significantly higher than developed market (DM) rates volatility—often multiples higher during periods of stress. Even amid current market turmoil, the improved fundamental picture for emerging market bonds is evidenced by the EMD asset classes displaying lower volatility than their DM counterparts.

In practical terms, EM is behaving less like a fragile bloc and more like a set of economies supported by stronger policy frameworks and improved credibility. This matters for EMD because it changes the distribution of outcomes in volatile periods. Lower inflation pass-through can reduce the probability of forced, pro-cyclical tightening; muted outflows can reduce the likelihood of disorderly FX moves; and smaller growth impacts can support fiscal trajectories and credit quality.

Bond market total return volatility (90 day rolling measure)

5. Divergence and differentiation

Emerging market economies are now far more resilient to global shocks than in previous decades, but the range of outcomes across countries is widening significantly. The effects of a US$10 oil price shock, for instance, are highly asymmetric: energy importers experience headwinds to growth and upward pressure on inflation, while commodity-linked exporters often enjoy improved external balances and stronger terms of trade. Countries such as Brazil and Colombia have reaped the benefits of higher oil prices, and currencies in other oil-exporting economies—including the Kazakh tenge and Argentine peso—have remained supported despite challenging global conditions.

Importantly, even some oil-importing regions in Central America and the Caribbean have bolstered their resilience. This has been achieved through IMF-supported programmes that anchor structural reforms, investments in renewable energy that reduce oil import bills, and the adoption of orthodox macroeconomic frameworks. As a result, these economies are demonstrating greater stability than in previous adverse terms-of-trade cycles.

Elsewhere, tech-oriented markets like South Korea and Taiwan are riding the wave of global demand for artificial intelligence, while India—despite being a major energy importer—continues to benefit from robust structural growth drivers. This diversity of exposures within emerging markets helps to smooth overall volatility, as weakness in one segment can be offset by strength in another.

The key takeaway is clear: Emerging markets can no longer be approached as a single, uniform asset class. Success now depends on careful, country-by-country and segment-by-segment differentiation, rather than treating EM as a monolithic “beta” trade.

Past performance does not predict future returns.

Source: Refinitiv, MSCI, HSBC Asset Management, March 2026. The commentary and analysis presented in this document reflect the opinion of HSBC Asset Management on the markets, according to the information available to date. They do not constitute any kind of commitment from HSBC Asset Management. Consequently, HSBC Asset Management will not be held responsible for any investment or disinvestment decision taken on the basis of the commentary and/or analysis in this document. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index.

Outlook for EMD asset classes

- EM Hard Currency: Over the years, a commitment to sound fiscal management has bolstered their resilience. Credit rating agencies have increasingly recognized these improvements, with the average rating for EM sovereigns rising and issuers enjoying favorable outlooks, which has contributed to the lower volatility and stable credit spreads recently. In addition, the carry of EM bonds remains attractive thanks to a higher-for-longer rates environment in the US, meaning asset allocators are not too late to join the EMD trade.

- EM Local Currency. A weaker US dollar, partly driven by questions around the safe haven status of US assets and US exceptionalism, could further boost EM currency returns. We see three primary drivers for the weakening US dollar trend and continued support of the EMD currency trade:

- A Federal Reserve that is biased to ease policy, maintaining downward pressure on front end US yields;

- The relative quality differential between EM and DM with regard to lower debt ratios and more sustainable debt service capacity, external account improvements, and positive credit ratings momentum; and

- Ongoing negotiation of bilateral trade deals between the US and its major trading partners that increasingly offset tariffs in exchange for currency appreciation.

- EM Corporate debt: Continues to offer diversification, resilience, and attractive yields. In addition, EM companies demonstrate stronger financial discipline compared to their DM peers, on average. Corporate debt has a lower duration profile, and as a result, performance is less correlated to US Treasuries than other asset classes. Their higher yields, coupled with the prospect of capital gains from cyclically declining interest rates, present a prospect for strong returns.

Conclusion

Emerging Markets Debt has evolved into a more resilient and differentiated asset class, supported by stronger fiscal discipline, improved external buffers, and more credible monetary policy frameworks across many countries. Recent episodes of higher oil prices, a stronger US dollar, and elevated global rates—conditions that historically would have triggered broad-based stress—have instead highlighted a more muted EM response, reinforcing the improved quality of the asset class abroad-baseds well as the importance of country-by-country and segment-by-segment selection.

With attractive yields, improving credit quality, and diversification benefits across hard currency sovereigns, local currency markets, and corporates, EMD offers multiple ways to participate in a shifting macro environment. While country-specific risks remain and dispersion is widening, the combination of stronger fundamentals and a more mature opportunity set supports the case for EMD as a strategic building block in global portfolios.

Source: HSBC Asset Management, March 2026

For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. Any views expressed were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way, HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target.

Key risks

It is important to remember that the value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested.

- Counterparty Risk The possibility that the counterparty to a transaction may be unwilling or unable to meet its obligations.

- Credit Risk A bond or money market security could lose value if the issuer’s financial health deteriorates.

- Default Risk The issuers of certain bonds could become unwilling or unable to make payments on their bonds.

- Derivatives Risk Derivatives can behave unexpectedly. The pricing and volatility of many derivatives may diverge from strictly reflecting the pricing or volatility of their underlying reference(s), instrument or asset.

- Emerging Markets Risk Emerging markets are less established, and often more volatile, than developed markets and involve higher risks, particularly market, liquidity and currency risks.

- Exchange Rate Risk Changes in currency exchange rates could reduce or increase investment gains or investment losses, in some cases significantly.

- Interest Rate Risk When interest rates rise, bond values generally fall. This risk is generally greater the longer the maturity of a bond investment and the higher its credit quality.

- Investment Leverage Risk Investment Leverage occurs when the economic exposure is greater than the amount invested, such as when derivatives are used. A Fund that employs leverage may experience greater gains and/or losses due to the amplification effect from a movement in the price of the reference source.

- Liquidity Risk Liquidity Risk is the risk that a Fund may encounter difficulties meeting its obligations in respect of financial liabilities that are settled by delivering cash or other financial assets, thereby compromising existing or remaining investors.

- Operational Risk Operational risks may subject the Fund to errors affecting transactions, valuation, accounting, and financial reporting, among other things.

- Sustainability Risk Sustainability risk means an environmental, social or governance event or condition that, if it occurs, could cause an actual or a potential material negative impact on the value of the investment

For more detailed information on the risks associated, investors should refer to the offering document.

Important Information

For Professional Clients and intermediaries within countries and territories set out below and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager&rsquo s skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets: investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

All data from HSBC Asset Management unless otherwise specified. Any third-party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group).

In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws

- In Bermuda, this document is issued by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority

- In France, Belgium, Netherlands, Luxembourg, Portugal, Greece, Finland, Norway, Denmark and Sweden this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026)

- In Germany, this document is issued by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients)

- In Hong Kong, this document is issued by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This content has not been reviewed by the Securities and Futures Commission

- In India, this document is issued by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India

- In Italy and Spain, this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026) and through the Italian and Spanish branches of HSBC Global Asset Management (France), regulated respectively by Banca d&rsquo Italia and Commissione Nazionale per le Società e la Borsa (Consob) in Italy, and the Comisió n Nacional del Mercado de Valores (CNMV) in Spain

- In Japan, this document is issued by HSBC Asset Management (Japan) Ltd (JRN 3010001124868), regulated by the Financial Services Agengy

- In Malta, this document is issued by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act

- In Mexico, this document is issued by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversió n, Grupo Financiero HSBC which is regulated by Comisió n Nacional Bancaria y de Valores

- In the United Arab Emirates, this document is issued by HSBC Investment Funds (Luxembourg) S.A. &ndash Dubai Branch (Level 20, HSBC Tower, PO Box 66, Downtown Dubai, United Arab Emirates) regulated by the Capital Market Authority (CMA) in the UAE to conduct investment fund management, portfolios management, fund administration activities (CMA Category 2 license No.20200000336) and promotion activities (CMA Category 5 license No.20200000327).

- In the United Arab Emirates, this document is issued by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Capital Market Authority in the UAE under CMA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient&rsquo s country of residence and therefore may not be subject to supervision of the local regulator in the recipient&rsquo s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient&rsquo s country of residence.

- In Singapore, this document is issued by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore

- In Switzerland, this document is issued by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (&ldquo SBA&rdquo ) Brochure &ldquo Risks Involved in Trading in Financial Instruments&rdquo

- In Taiwan, this document is issued by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan)

- In Turkiye, this document is issued by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations.

- In the UK, this document is issued by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority

- In the US, this document is issued by HSBC Securities (USA) Inc., an HSBC broker dealer registered in the US with the Securities and Exchange Commission under the Securities Exchange Act of 1934. HSBC Securities (USA) Inc. is also a member of NYSE/FINRA/SIPC. HSBC Securities (USA) Inc. is not authorized by or registered with any other non-US regulatory authority. The contents of this document are confidential and may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose without prior written permission.

- In Chile, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Obtain information about the state guarantee to deposits at your bank or on www.cmfchile.cl

- In Colombia, HSBC Bank USA NA has an authorized representative by the Superintendencia Financiera de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution

- In Costa Rica, the Fund and any other products or services referenced in this document are not registered with the Superintendencia General de Valores (&ldquo SUGEVAL&rdquo ) and no regulator or government authority has reviewed this document, or the merits of the products and services referenced herein. This document is directed at and intended for institutional investors only.

- In Peru, HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Perú whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Perú and is not for public distribution

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy.

Copyright © HSBC Global Asset Management Limited 2026. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Asset Management.

Content ID: D070204_V1.0 Expiry date: 01.04.2027