Investment Monthly

Key Takeaways:

House Views

- Markets and economists describe diverging worlds: with strong corporate profits and AI enthusiasm lifting markets, while the oil shock and elevated macro risks present significant economic headwinds. That means bursts of episodic volatility are expected to be a recurring theme

- A broadening out of market returns across regions is still possible in 2026. In particular, emerging and frontier market equities offer a potentially attractive blend of value and profits growth, with strong exposure to the AI and tech themes

- Investors should also “diversify the diversifiers” by tilting to alternatives like hedge funds and real assets

Macro Outlook

- Geopolitical uncertainty remains in focus with the blockade of the Strait of Hormuz pushing oil back above USD 100/barrel. The futures curve is starting to price a more persistent supply problem, implying higher-for-longer inflation and a greater the likelihood of a negative growth shock

- US growth is solid but uneven – “K shaped” dynamics remain in play. AI investment is booming, but other forms of capex are soft, and consumers’ real incomes are being squeezed. European growth is weak

- In China, macro policies, the tech cycle and industrial competitiveness are supporting growth. Korea is benefitting from the AI boom, but the high oil price is a headwind for some other EM Asia economies

Policy Outlook

- Policy uncertainty remains high amid ongoing geopolitical and trade tensions, high government debt levels in some major economies, and central banks caught between upside inflation and downside growth risks

- The Fed should have room to look through a near-term inflation bump and cut modestly from late 2026. But the ECB and BoE have signalled a bias to hike reflecting concerns over inflation expectations

- China will continue to focus on fiscal policy to boost domestic demand. Reforms are needed to enhance strategic objectives (technology innovation, self-reliance, and economic rebalancing). EM Asia economies are adopting varying policy approaches, reflecting relative exposure to AI and the oil shock

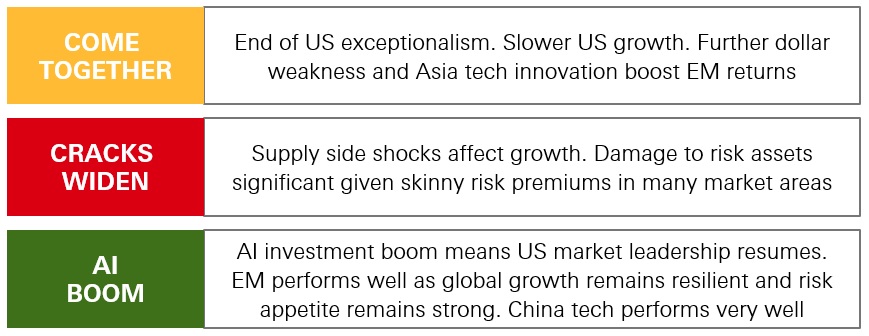

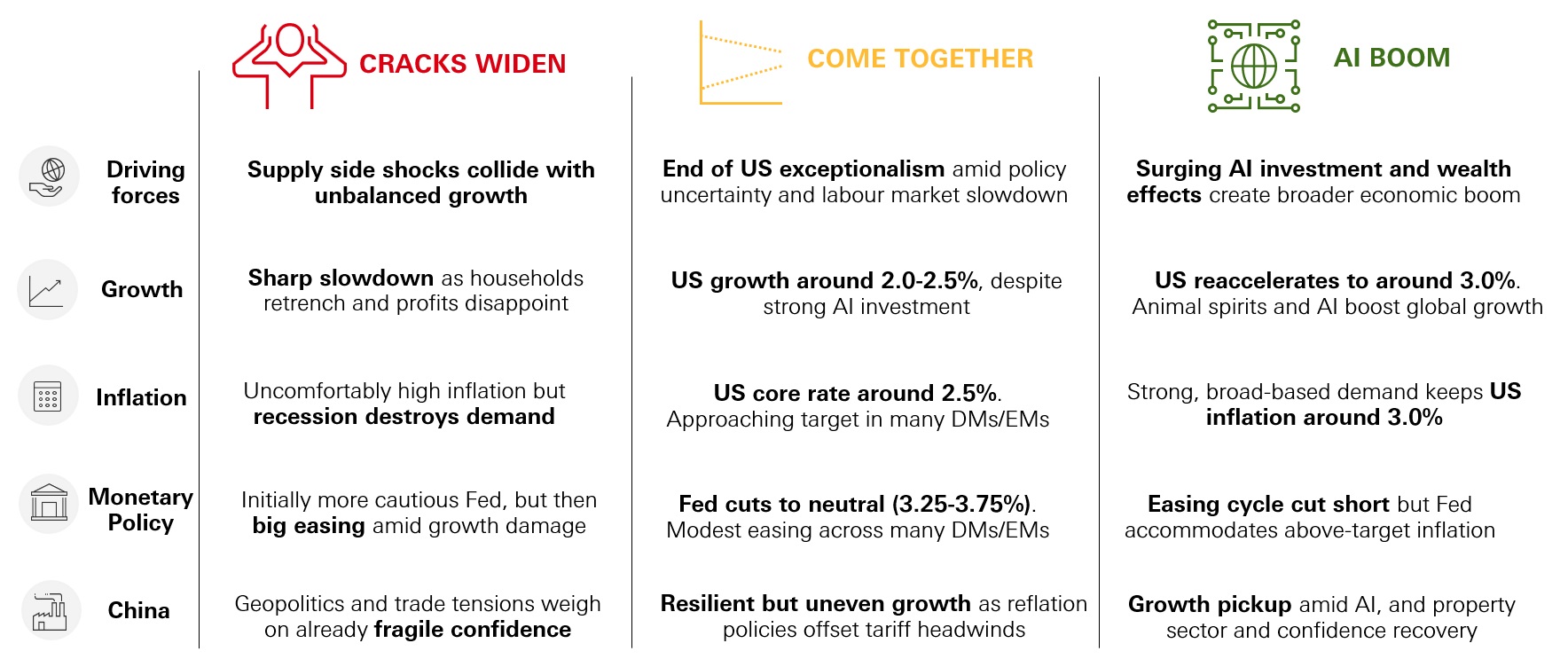

Scenarios

Click the image to enlarge

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. The views expressed above were held at the time of preparation and are subject to change without notice. Diversification does not ensure a profit or protect against loss. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security.

Source: HSBC Asset Management as at May 2026.

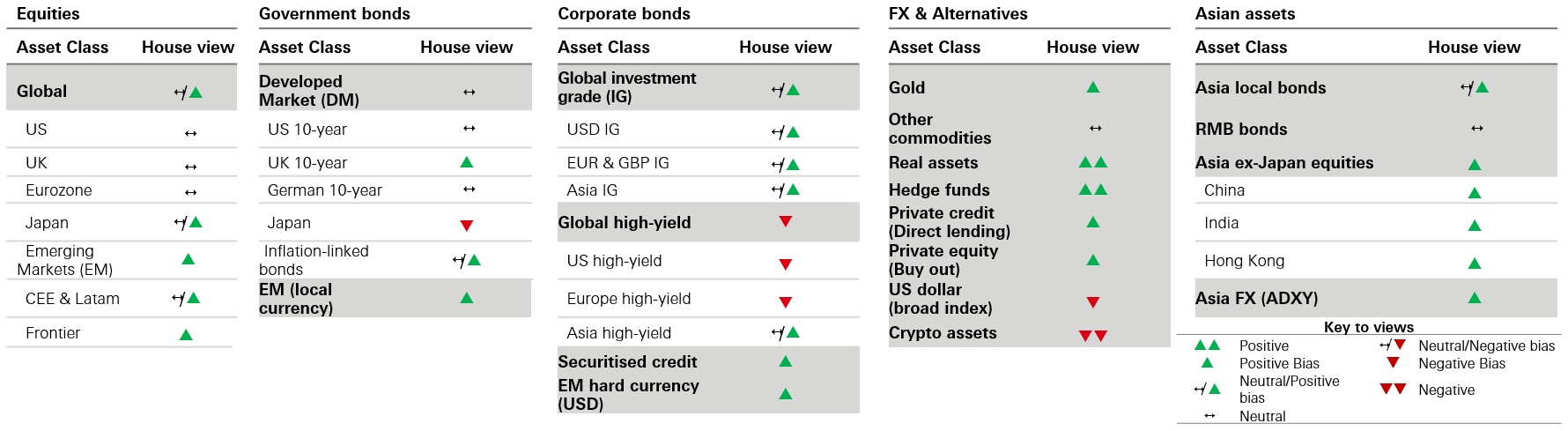

House View

Exceptional profits growth is driving stock market performance, but economic headwinds from higher oil prices and sticky inflation may translate to episodic bursts of volatility. Emerging markets continue to impress, supported by an attractive combination of value and profits growth, and exposure to the AI/tech theme

- Equities – Higher energy prices have disrupted the past year’s theme of "broadening out“. But markets have rebounded from the Q1 sell-off, and could see a further broadening of profits and price performance beyond the US

- Government bonds – Yields remain elevated amid inflation concerns, geopolitical risks, and uncertainty over the path for policy rates. Ultimately, weaker growth could limit central bank tightening and push yields lower

- Corporate bonds – Investment grade credit spreads remain tight amid robust fundamentals. High yield credit faces pressure from uneven US growth and geopolitics. We maintain a preference for higher quality

Click the image to enlarge

The level of yield is not guaranteed and may rise or fall in the future. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. The views expressed above were held at the time of preparation and are subject to change without notice. Diversification does not ensure a profit or protect against loss. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. House view represents a >12-month investment view across major asset classes in our portfolios. Source: HSBC Asset Management as at May 2026.

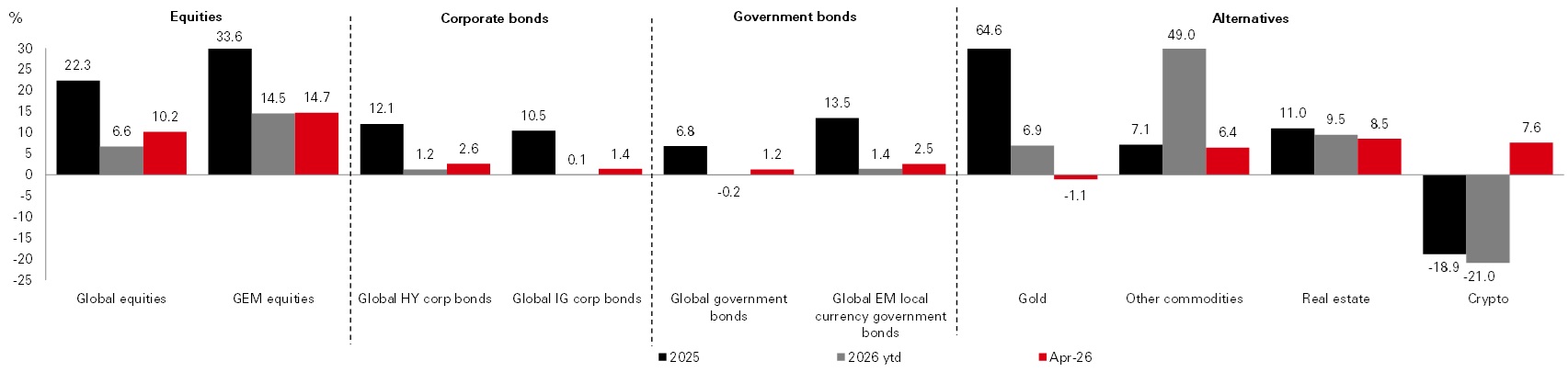

Asset class performance at a glance

Global stocks rallied in April, with markets in the US and parts of Asia reaching new highs, driven by strong profits growth. Sovereign bonds were steady as investors weighed the impact of geopolitical tensions, fiscal concerns, and potentially higher-for-longer rates. The US dollar ended the month lower, with gold also weaker

- Government bonds – US 10-year Treasury yields were largely range-bond but closed the month higher on the ongoing closure of the Strait of Hormuz and a more hawkish tone from the US Fed. Thirty-year UK Gilt yields rose steeply

- Equities – Global stock markets rallied on evidence of a strong Q1-26 earnings season. Tech and AI remain a key driver, particularly in the US and Asia. Hong Kong, UK, and Latam markets were the main laggards

- Alternatives – Industrial metals, led by copper, experienced a strong month, but precious metals came under pressure. Listed real estate and infrastructure both delivered a robust performance. Digital assets enjoyed a rebound

Click the image to enlarge

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. This information shouldn’t be considered as a recommendation to invest in the country or sector shown. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. The views expressed above were held at the time of preparation and are subject to change without notice. Source: Bloomberg, all data above as at close of business 30 April 2026 in USD, total return, month-to-date terms. Note: Asset class performance is represented by different indices. Global Equities: MSCI ACWI Net Total Return USD Index. Global Emerging Market Equities: MSCI Emerging Market Net Total Return USD Index. Corporate Bonds: Bloomberg Barclays Global HY Total Return Index value unhedged. Bloomberg Barclays Global IG Total Return Index unhedged. Government bonds: Bloomberg Barclays Global Aggregate Treasuries Total Return Index. JP Morgan EMBI Global Total Return local currency. Commodities and real estate: Gold Spot $/OZ, Other commodities: S&P GSCI Total Return CME. Real Estate: FTSE EPRA/NAREIT Global Index TR USD. Crypto: Bloomberg Galaxy Crypto Index. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index.

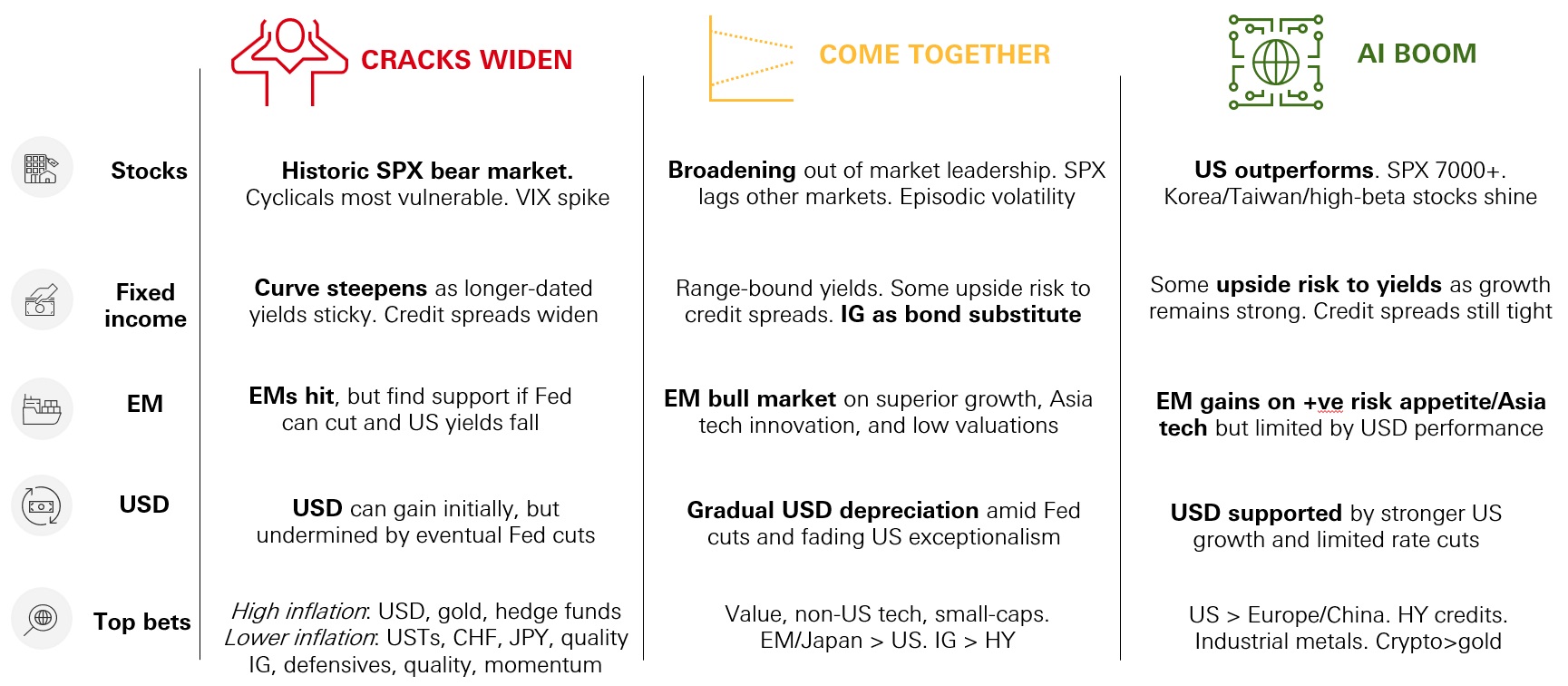

Macro scenarios

Click the image to enlarge

Market scenarios

Click the image to enlarge

The commentary and analysis presented in this document reflect the opinion of HSBC Asset Management on the markets, according to the information available to date. They do not constitute any kind of commitment from HSBC Asset Management. Consequently, HSBC Asset Management will not be held responsible for any investment or disinvestment decision taken on the basis of the commentary and/or analysis in this document. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security.

Source: HSBC Asset Management, May 2026.

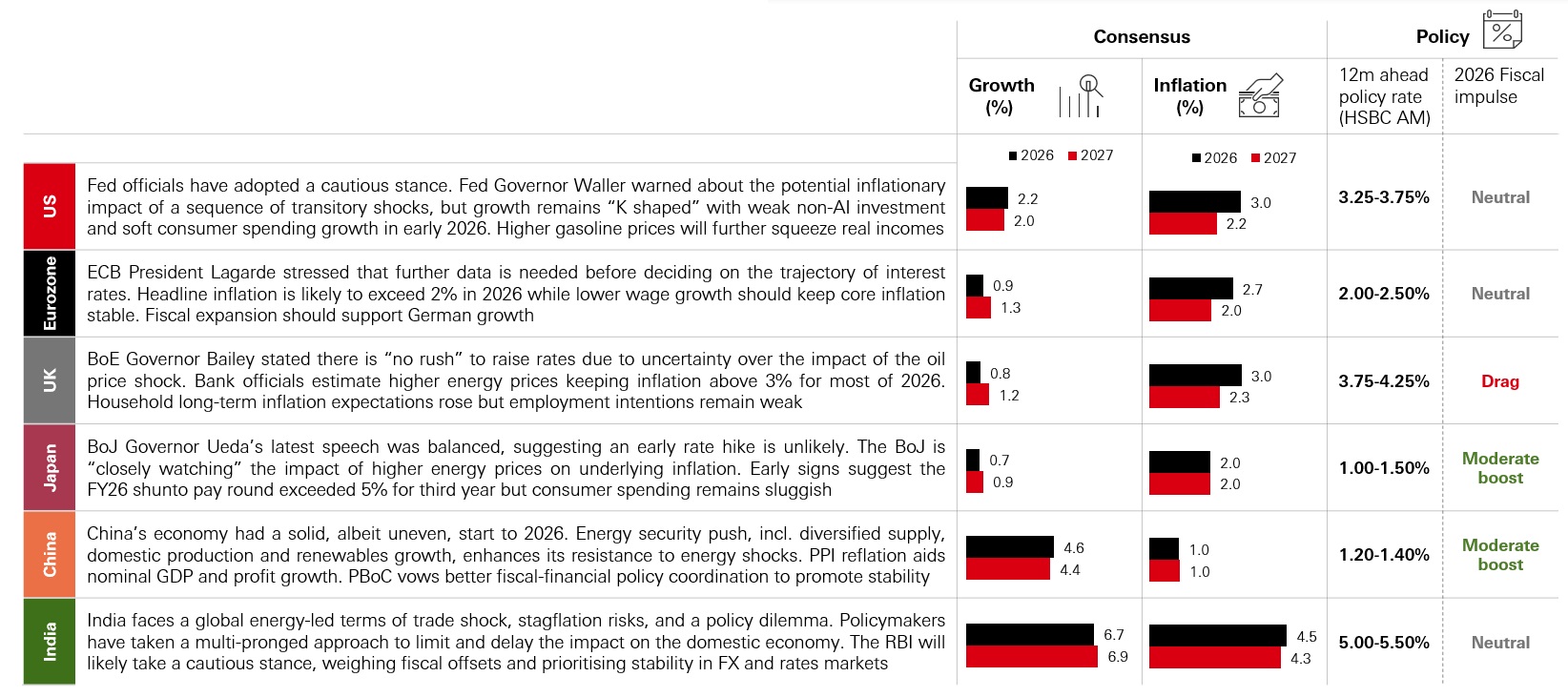

Economic outlook

Fed in wait-and-see mode, ECB and BoE bias to hike

Click the image to enlarge

Past performance does not predict future returns. Any views expressed were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way. HSBC Asset Management Limited accepts no liability for any failure to meet such forecast, projection or target. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security.

Source: HSBC Asset Management, consensus numbers from Bloomberg, May 2026.

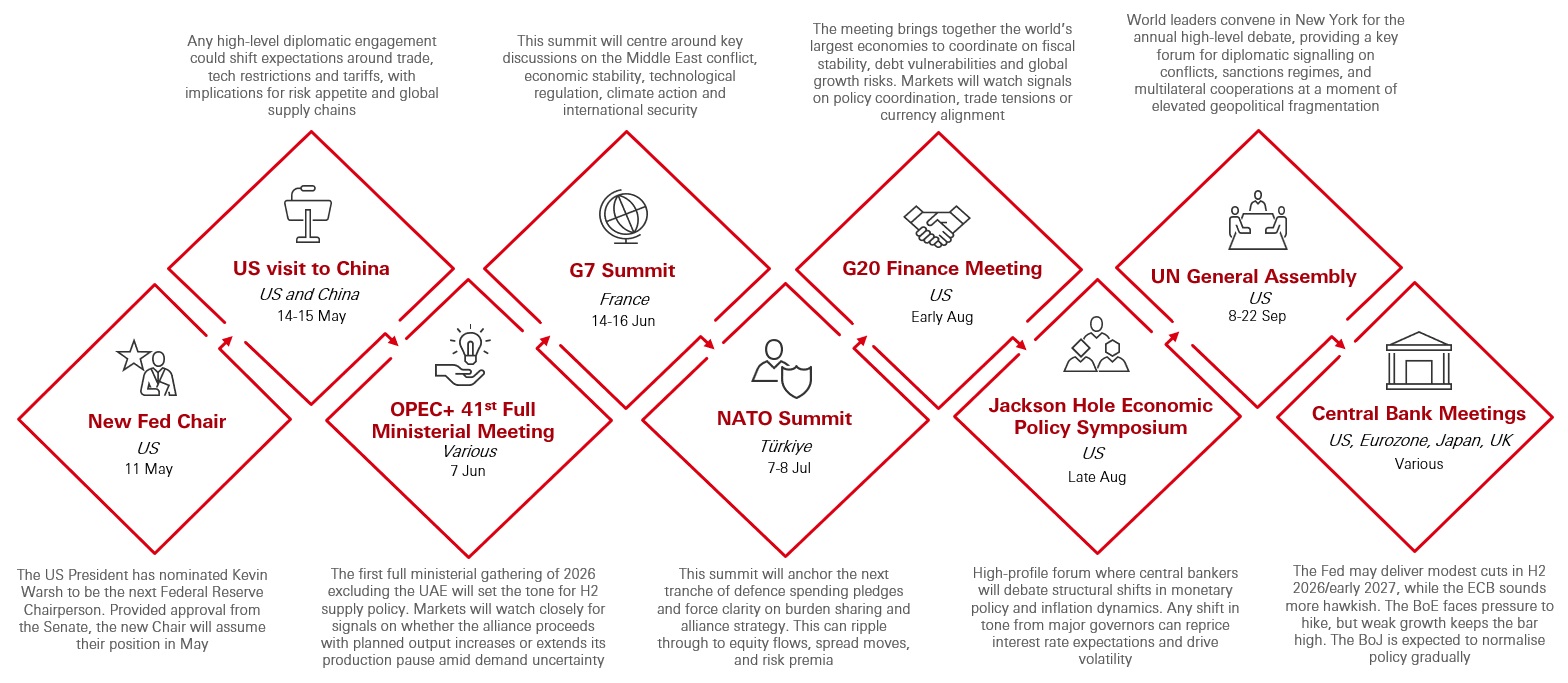

Events calendar 2026 - 6-month forward looking

Click the image to enlarge

The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target. Past performance does not predict future returns. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security.

Source: HSBC Asset Management, May 2026.

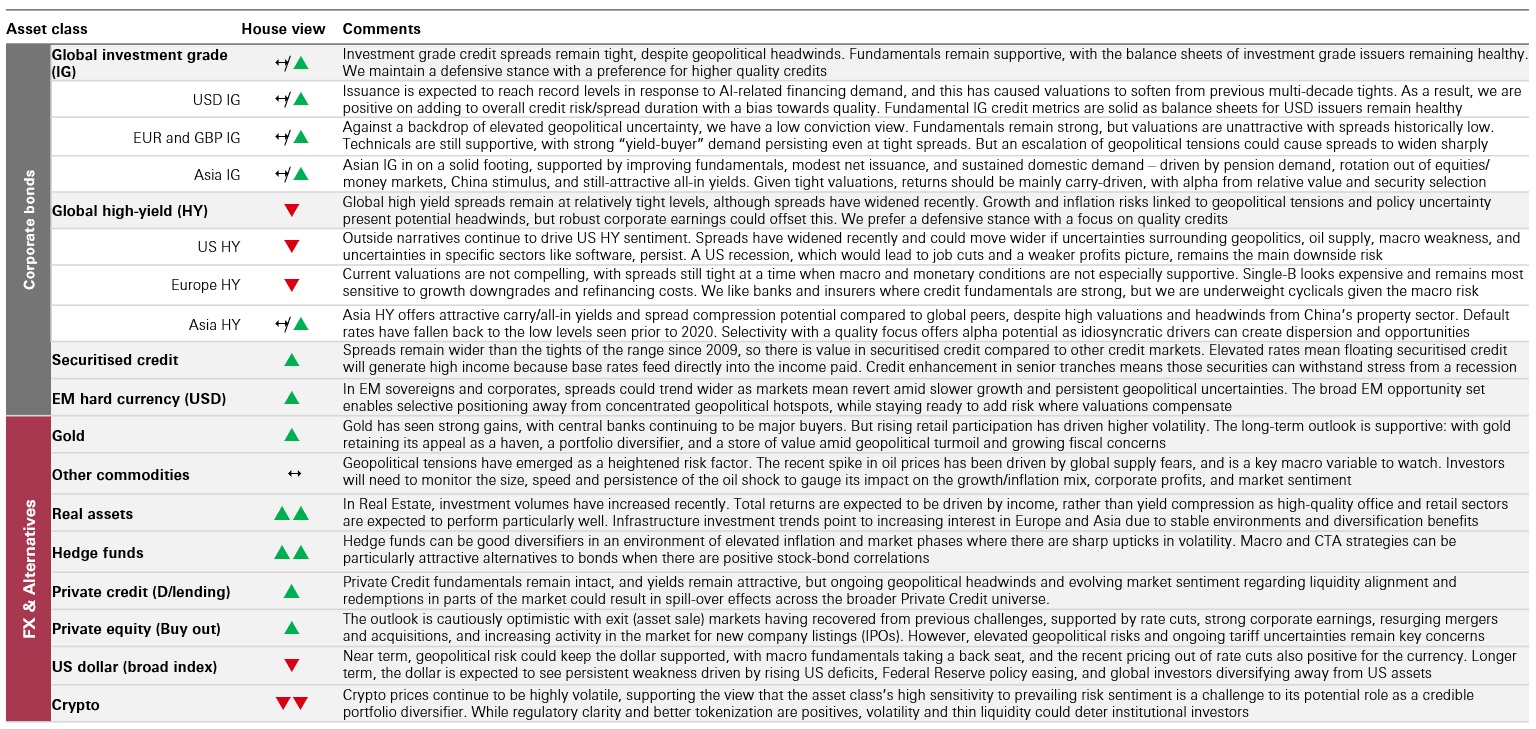

Investment Views

Asset class positioning

Click the image to enlarge

Click the image to enlarge

Click the image to enlarge

The level of yield is not guaranteed and may rise or fall in the future. Diversification does not ensure a profit or protect against loss. The views expressed above were held at the time of preparation and are subject to change without notice. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index.

Source: HSBC Asset Management as at May 2026.

On Top of Investors’ Minds

Markets rallied in April. What should investors be watching now?

April’s rally after the US/Iran ceasefire has left markets and economists describing two completely different worlds: strong corporate profits are lifting markets, while the oil shock and unresolved Hormuz disruption keep recession-style macro risks in play. There are three factors to pay attention to:

Profits vs rates. Earnings – especially in US tech and energy – are doing the heavy lifting in driving market performance. The main threat is higher policy rates. If they keep moving higher, it will put pressure on valuations – and that’s when the balance breaks.

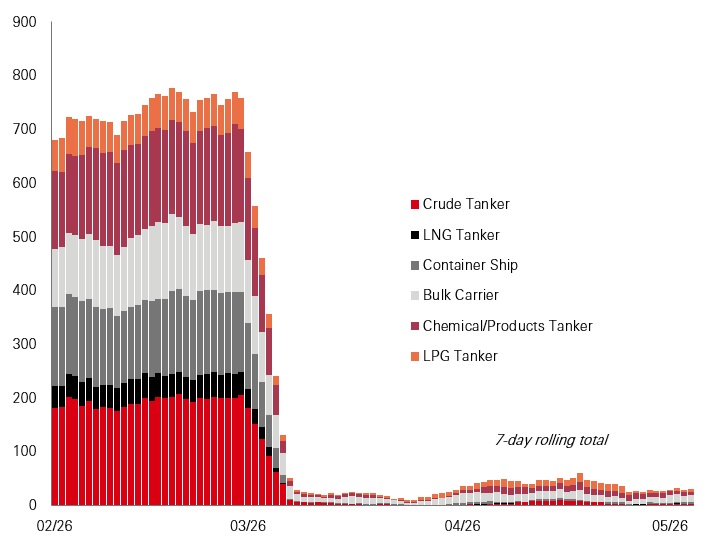

The Strait of Hormuz is the key macro tell. Investors should track vessel crossings through the strait. A clear, sustained rise would support risk assets even if broader geopolitical issues linger.

Oil and central banks. Spot oil has eased, but an elevated spot–futures spread signals ongoing supply stress. If disruptions fade, the futures curve should flatten, giving the Fed/BoE/ECB more room to “look through” the shock rather than hike.

In 2026, profits are the engine and rates are the constraint; macro risk matters most when it threatens either. Meanwhile, episodic bursts of volatility are likely to be a recurring feature in markets. Investors should stay diversified, disciplined, and data-led.

Number of vessels crossing the Strait of Hormuz

Click the image to enlarge

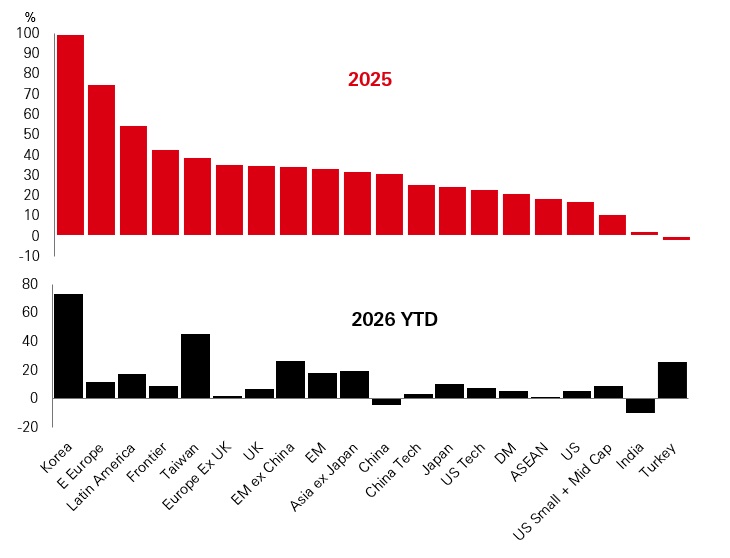

What now for broadening out?

A broadening out of returns was a key market development in 2025. This was achieved via a combination of a weaker dollar, global central bank policy easing, steady GDP growth across economies and stronger profits growth outside of US mega-cap tech. The Hormuz crisis is a challenge to this theme in 2026. With US energy independence and the AI boom helping keep US growth supported, other regions may face more significant GDP and profits downgrades. Recent US tech earnings have been very solid. And the bar to further central bank rate cuts looks high.

But there are plenty of factors that can keep the broadening out trade alive in 2026. Central banks outside of the US may end up being more hawkish, keeping the dollar-down trend intact. EM is also a well-recognised play on the tech and AI theme, given the big exposure to Korea and Taiwan. This is reflected in year-to-date performance. Meanwhile, the recent surge in commodity prices not only benefits many EMs (mainly LatAM) and Frontiers, but also energy and materials names.

And although the AI boom continues to benefit mega-cap tech, the broader infrastructure build-out remains a major boost to industrials, utilities, and materials, while the AI adoption and productivity story is a positive for sectors outside of core tech.

MSCI performance by region

Click the image to enlarge

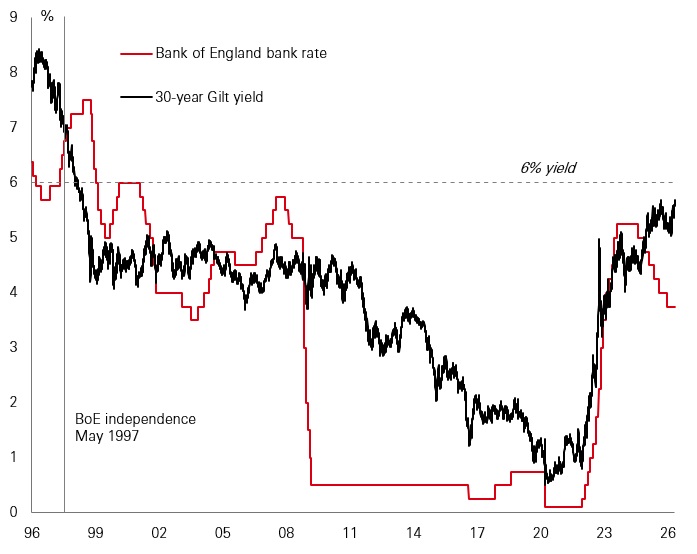

Gilt yields have risen sharply. Should investors fear bond vigilantes, or welcome the income opportunity?

While 30-year Gilt yields are back at levels last seen in the late 1990s, most of the recent action in Gilts has been at the short end. In March, rate expectations surged, forecasting three hikes from the Bank of England in 2026. In April, that’s dropped back to just over two hikes. So, what happens to long term Gilts if those rate hikes are delivered?

One possibility is that long-term bonds would sell off even more. After all, investors are worrying about high UK debt, the inflation-prone economy, and less policy co-ordination than in Europe. But there is also a lot of bad news already baked in. And that means that yields themselves can shape the short term.

The long end can rally, even if the BoE is hiking. That can happen if growth concerns begin to dominate, if inflation credibility is restored, or if investors are attracted by the income opportunity. And finance theory tells us that high starting yields and upward sloping curves are the two best predictors of high future bond returns. The quantitative signals are starting to look good for Gilts.

So, while the yield curve can steepen further, the carry in Gilts is hard for investors to ignore.

Bank of England bank rate and 30-year Gilt yields

Click the image to enlarge

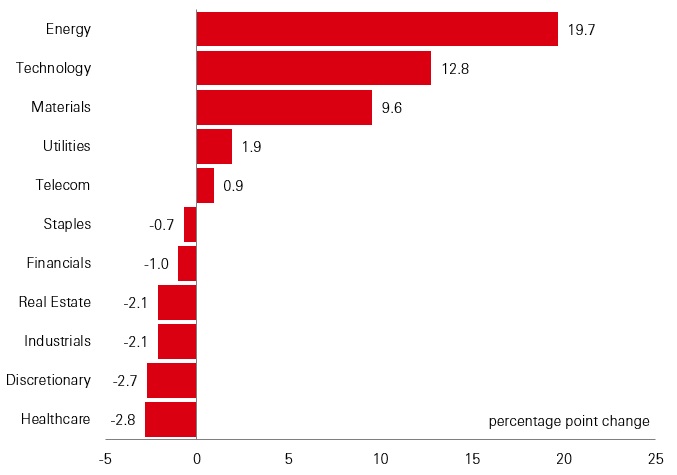

With Q1 2026 earnings season under way, what’s the outlook for corporate profits?

With the Middle East conflict unresolved, but the S&P 500 rallying hard, Q1 earnings season comes at a pivotal time. The early signs are positive – but there are reasons for caution.

There have been some powerful profits upgrades in the S&P since the start of 2026. Consensus year-on-year estimates stand at 13 per cent for Q1, and high double-digits for the full year. Energy leads the way in the upgrades race this quarter, with profits set to rise sharply. Technology and Communications have also seen strong upgrades on AI enthusiasm. They are jointly set to contribute 64 per cent of total index profits this year.

But there are catches. One is that concentration in profits in Tech and Comms could be an increasing risk if questions persist over capex spending and eventual AI productivity gains. A second is that recent data implies consumer spending could be close to flat for Q1, not helped by a soft labour market. Add to that higher oil prices and higher-for-longer rates on inflation fears, and it could hurt profits in cyclical and consumer-facing sectors.

Overall, Q1 profits should be good, but uncertainties around tech and AI, geopolitics, and the consumer, mean it’s worth being wary.

Three-month change in IBES 2026 earnings estimates (end-March 2026)

Click the image to enlarge

The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. Past performance does not predict future returns. Diversification does not ensure a profit or protect against loss. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index.

Source: HSBC Asset Management as at May 2026.

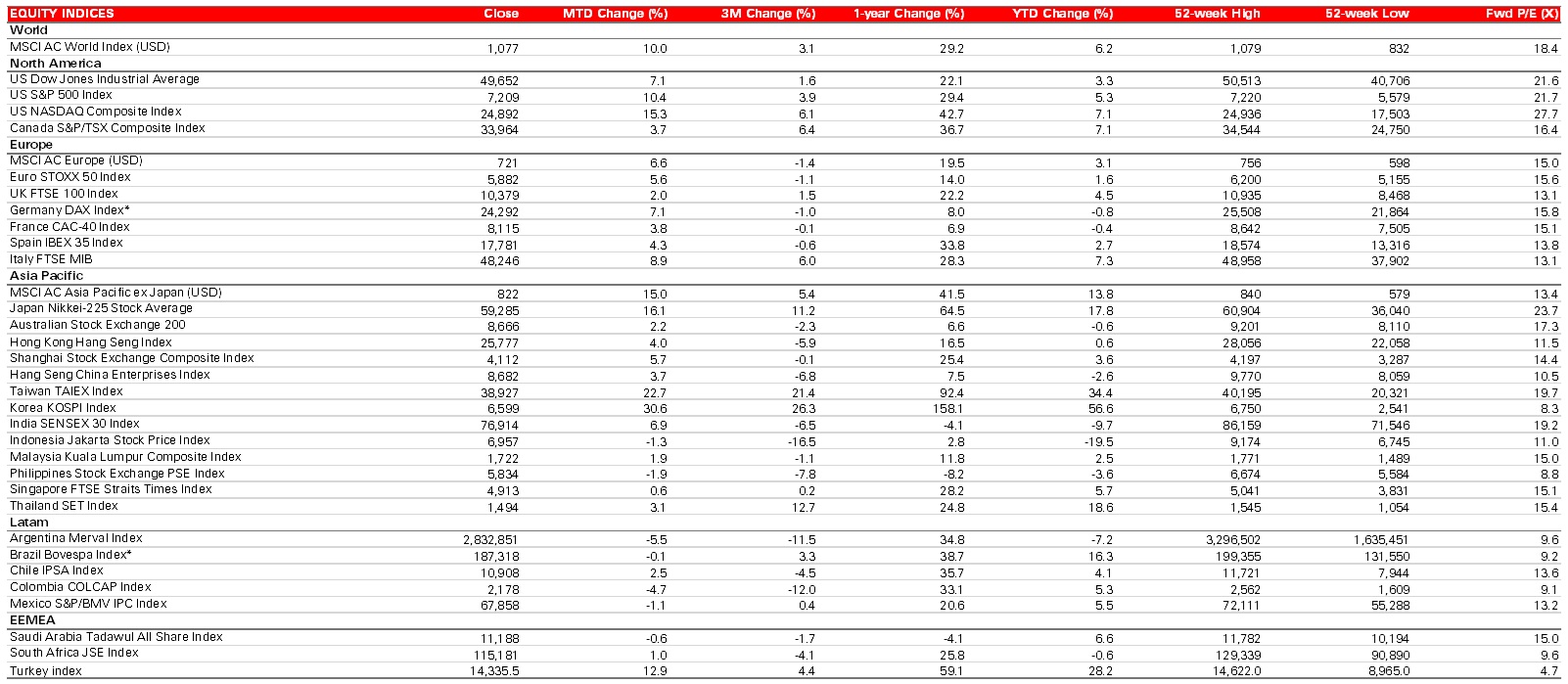

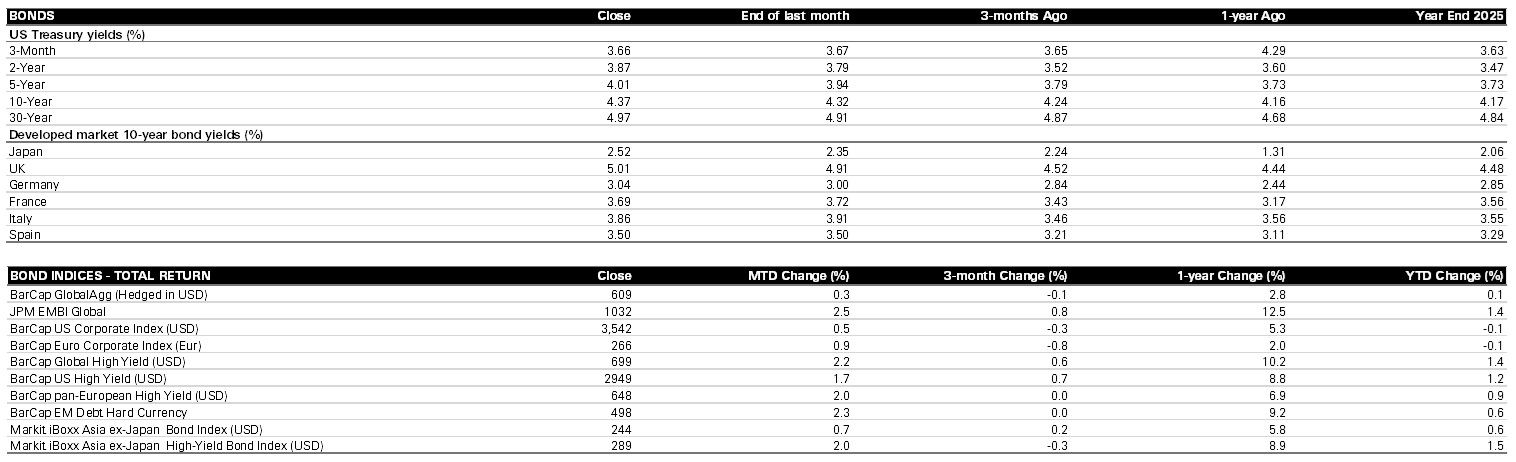

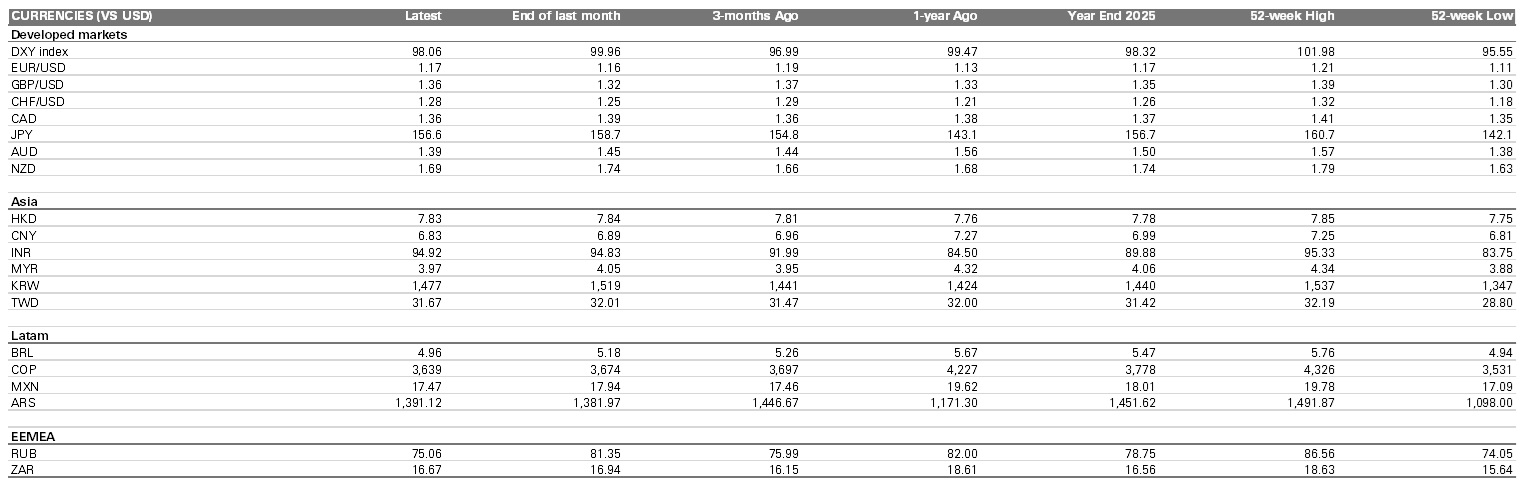

Market Data

April 2026

Click the image to enlarge

Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index.

Sources: Bloomberg, HSBC Asset Management. Data as at close of business 30 April 2026. (*) Indices expressed as total returns. All others are price returns.

Click the image to enlarge

All total returns quoted in USD terms.

Data sourced from MSCI AC World Total Return Index, MSCI USA Total Return Index, MSCI AC Europe Total Return Index, MSCI AC Asia Pacific ex Japan Total Return Index, MSCI Japan Total Return Index, MSCI Latam Total Return Index and MSCI Emerging Markets Total Return Index.

Click the image to enlarge

Click the image to enlarge

Click the image to enlarge

Total return includes income from dividends and interest as well as appreciation or depreciation in the price of an asset over the given period. Past performance does not predict future returns. The level of yield is not guaranteed and may rise or fall in the future. This information shouldn’t be considered as a recommendation to invest in the country or sector shown. Index returns assume reinvestment of all distributions and do not reflect fees or expenses. You cannot invest directly in an index.

Sources: Bloomberg, HSBC Asset Management. Data as at close of business 30 April 2026.

Important Information

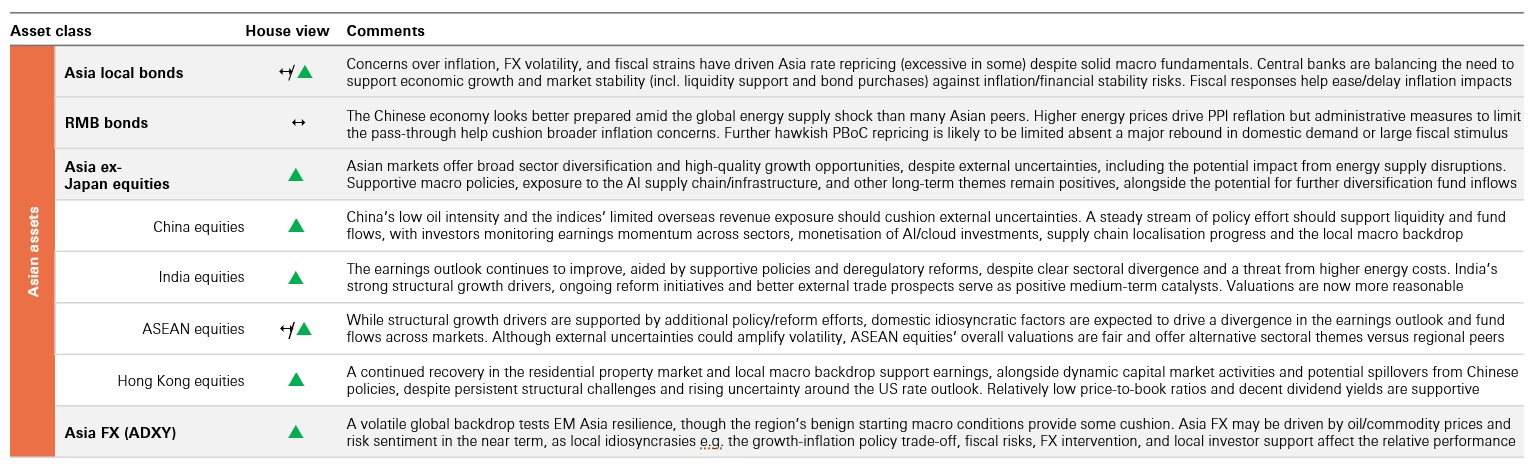

Basis of Views and Definitions of 'Asset class positioning' tables

- Views are based on regional HSBC Asset Management Asset Allocation meetings held throughout April 2026, HSBC Asset Management’s long-term expected return forecasts which were generated as at 31 March 2026, our portfolio optimisation process and actual portfolio positions

- Icons: ↑ View on this asset class has been upgraded – No change ↓ View on this asset class has been downgraded

- Underweight, overweight and neutral classifications are the high-level asset allocations tilts applied in diversified, typically multi-asset portfolios, which reflect a combination of our long-term valuation signals, our shorter-term cyclical views and actual positioning in portfolios. The views are expressed with reference to global portfolios. However, individual portfolio positions may vary according to mandate, benchmark, risk profile and the availability and riskiness of individual asset classes in different regions

- "Overweight" implies that, within the context of a well-diversified typically multi-asset portfolio, and relative to relevant internal or external benchmarks, HSBC Global Asset Management has (or would have) a positive tilt towards the asset class

- "Underweight" implies that, within the context of a well-diversified typically multi-asset portfolio, and relative to relevant internal or external benchmarks, HSBC Global Asset Management has (or would) have a negative tilt towards the asset class

- "Neutral" implies that, within the context of a well-diversified typically multi-asset portfolio, and relative to relevant internal or external benchmarks HSBC Global Asset Management has (or would have) neither a particularly negative or positive tilt towards the asset class

- For global investment-grade corporate bonds, the underweight, overweight and neutral categories for the asset class at the aggregate level are also based on high-level asset allocation considerations applied in diversified, typically multi-asset portfolios. However, USD investment-grade corporate bonds and EUR and GBP investment-grade corporate bonds are determined relative to the global investment-grade corporate bond universe

- For Asia ex Japan equities, the underweight, overweight and neutral categories for the region at the aggregate level are also based on high-level asset allocation considerations applied in diversified, typically multi-asset portfolios. However, individual country views are determined relative to the Asia ex Japan equities universe as of 31 March 2026

- Similarly, for EM government bonds, the underweight, overweight and neutral categories for the asset class at the aggregate level are also based on high-level asset allocation considerations applied in diversified, typically multi-asset portfolios. However, EM Asian Fixed income views are determined relative to the EM government bonds (hard currency) universe as of 30 April 2026

For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector, or security. The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. Diversification does not ensure a profit or protect against loss.

For Professional Clients and intermediaries within countries and territories set out below; and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager's skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in Emerging Markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets: investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

All data from HSBC Asset Management unless otherwise specified. Any third-party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group).

- In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws;

- In Bermuda, this document is issued by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority;

- In France, Belgium, Netherlands, Luxembourg, Portugal, Greece, Finland, Norway, Denmark and Sweden this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026);

- In Germany, this document is issued by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients);

- In Hong Kong, this document is issued by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This content has not been reviewed by the Securities and Futures Commission;

- In India, this document is issued by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India;

- In Italy and Spain, this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026) and through the Italian and Spanish branches of HSBC Global Asset Management (France), regulated respectively by Banca d’Italia and Commissione Nazionale per le Società e la Borsa (Consob) in Italy, and the Comisión Nacional del Mercado de Valores (CNMV) in Spain;

- In Japan, this document is issued by HSBC Asset Management (Japan) Ltd (JRN 3010001124868), regulated by the Financial Services Agency;

- In Malta, this document is issued by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act;

- In Mexico, this document is issued by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversión, Grupo Financiero HSBC which is regulated by Comisión Nacional Bancaria y de Valores;

- In the United Arab Emirates, this document is issued by HSBC Investment Funds (Luxembourg) S.A. – Dubai Branch (Level 20, HSBC Tower, PO Box 66, Downtown Dubai, United Arab Emirates) regulated by the Capital Market Authority (CMA) in the UAE to conduct investment fund management, portfolios management, fund administration activities (CMA Category 2 license No.20200000336) and promotion activities (CMA Category 5 license No.20200000327).

- In the United Arab Emirates, this document is issued by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Capital Market Authority in the UAE under CMA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient’s country of residence and therefore may not be subject to supervision of the local regulator in the recipient’s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient’s country of residence.

- In Singapore, this document is issued by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore;

- In Switzerland, this document is issued by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website; if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (“SBA”) Brochure “Risks Involved in Trading in Financial Instruments”;

- In Taiwan, this document is issued by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan);

- In Turkiye, this document is issued by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations.

- In the UK, this document is issued by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority;

- In the US, this document is issued by HSBC Securities (USA) Inc., an HSBC broker dealer registered in the US with the Securities and Exchange Commission under the Securities Exchange Act of 1934. HSBC Securities (USA) Inc. is also a member of NYSE/FINRA/SIPC. HSBC Securities (USA) Inc. is not authorized by or registered with any other non-US regulatory authority. The contents of this document are confidential and may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose without prior written permission.

- In Chile, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Obtain information about the state guarantee to deposits at your bank or on www.cmfchile.cl;

- In Colombia, HSBC Bank USA NA has an authorized representative by the Superintendencia Financiera de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution;

- In Costa Rica, the Fund and any other products or services referenced in this document are not registered with the Superintendencia General de Valores (“SUGEVAL”) and no regulator or government authority has reviewed this document, or the merits of the products and services referenced herein. This document is directed at and intended for institutional investors only.

- In Peru, HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Perú whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Perú and is not for public distribution;

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abro ad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy.

Copyright © HSBC Global Asset Management Limited 2026. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Asset Management.

Content ID: D070323_V1.0; Expiry Date: 05.11.2026