Stablecoins and tokenised MMFs: opportunities and challenges

The financial landscape is undergoing a significant transformation with the emergence of digital assets, particularly stablecoins and tokenised investments. These innovations present both opportunities and challenges for traditional finance practitioners including corporate treasurers. This paper aims to provide a comprehensive overview of stablecoins and tokenised money market funds, highlighting their potential impact on the financial ecosystem, and comment on current developments in certain markets

Cryptocurrency

Before we discuss stablecoins, we need to understand cryptocurrencies. A cryptocurrency is a digital currency that doesn’t require a central bank or financial institution to verify transactions. Instead, this virtual currency is verified and recorded with blockchain technology, creating an unchangeable ledger (database) that tracks the purchase and sale of digital assets.

Some cryptocurrencies are speculative in nature, while others, known as stablecoins, seek to maintain a stable value and act as a digital version of cash.

Cryptocurrencies in general are moving closer to the mainstream, with a combination of increasing adoption by both retail and institutional investors as well as increased regulatory certainty. Part of the regulatory clarity has been a shift in restrictions global banking regulators had previously placed on banks exploring crypto-related product offerings. For example, in the United States, regulators announced in March 2025 that banks no longer require advance permission to engage in crypto-related activities, so long as the associated risks are managed. Given the global nature of stablecoins, regulators across the world are having to develop their own framework, at pace, to maintain some form of local guidelines for how these issuers and their transactions are governed. This has opened the door for traditional finance players to engage more fully in the digital asset landscape.

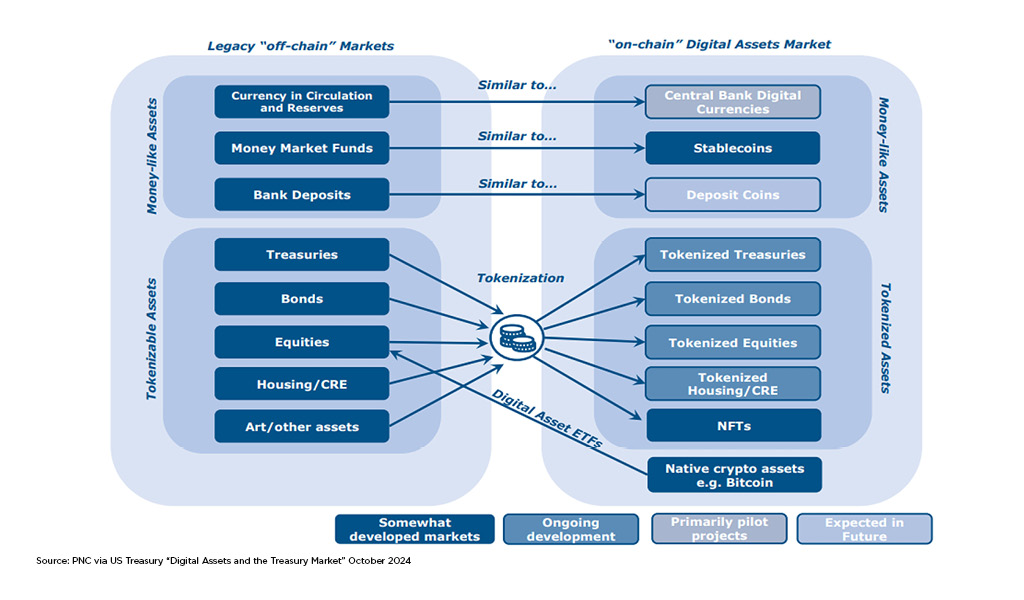

It is worth noting that while parts of the cryptocurrency industry appear completely foreign to a traditional asset manager, there are products that appear similar, and derive their value from or mimic traditional asset management products.

Stablecoins

A stablecoin can be viewed as a bridge between traditional finance and digital assets. They are used for trading on crypto exchanges as well as for payments and remittances. They exist on a blockchain, but their value is typically pegged to another asset, most commonly the US dollar, so stablecoins don’t experience the level of volatility of other cryptocurrencies.

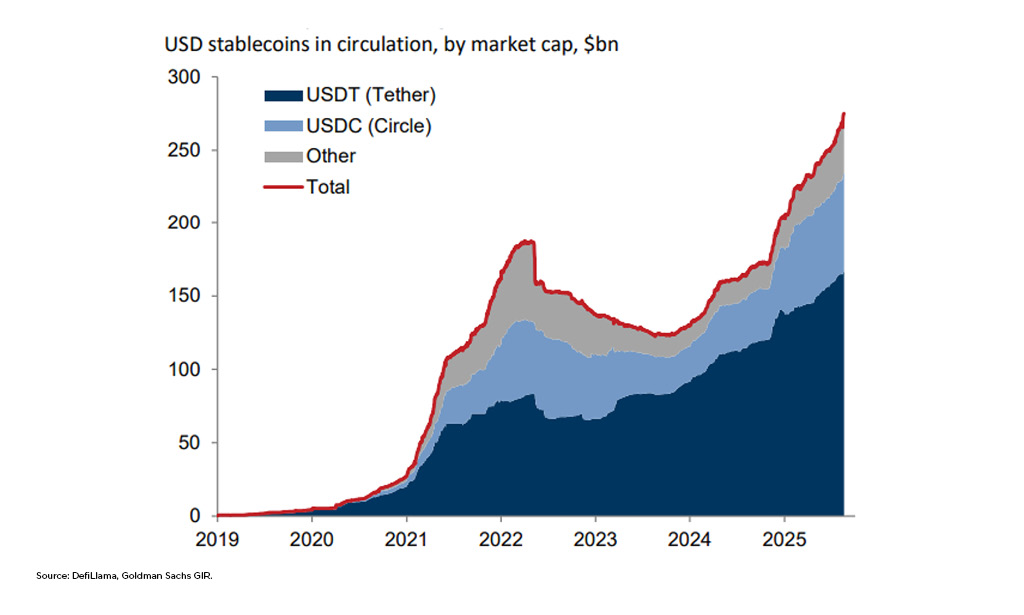

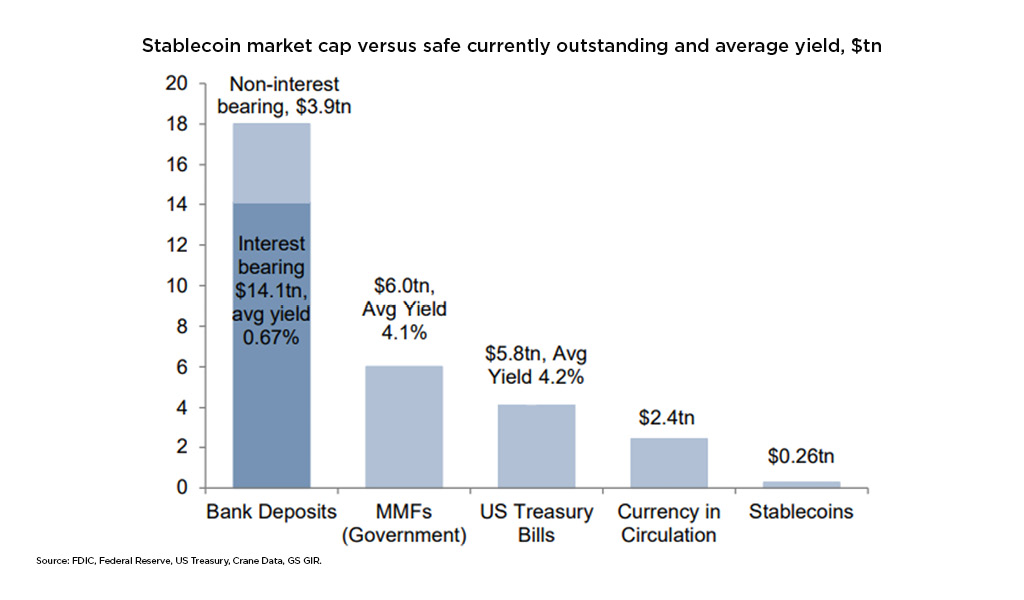

Stablecoins are close to USD300bn in market cap and reportedly reached USD28tn in transaction volume in 2024. The growth has been rapid but still pales in comparison to the scale of traditional finance alternatives to stablecoins, such as deposits and money market funds.

Tether (USDT) and Circle (USDC) make up 61 per cent and 25 per cent of the total market cap of stablecoins. USD stablecoins currently account for 99 per cent of the total market cap.

Today’s use cases

Stablecoin market cap has grown primarily due to its use as a convenient means to move between fiat and crypto currencies (commonly referred to as on-and off-ramp).

There is increased focus on the potential to use stablecoins for global payments on the blockchain. Consumers and businesses could benefit from more efficient settlement than traditional finance payment rails. Greater adoption of stablecoins for payment will require coordinated global regulation as well as user-friendly transaction interfaces. This use case poses a threat to existing payment rails such as bank payment systems and cards.

A stable and well-regulated stablecoin industry could use the power of the blockchain to facilitate cross border payments at scale, both faster and at a lower cost than existing banking frameworks 24 hours a day, seven days a week.

An additional use case for stablecoins, particularly those pegged to the US dollar, is that they provide hard currency exposure for those operating in countries with volatile currencies. The stablecoin could then be used for savings or transactions, such as remittances.

It is worth noting that stablecoins do not, and in most cases are not permitted by regulation, to pay any yield / return. This has been consistently reflected in existing regulation across multiple jurisdictions to distinguish stablecoins as a digital payment instrument and not an investment product. As a result, stablecoins in their current form are not likely to supplant MMFs or interest-bearing deposits as a cash investment vehicle.

Risks presented by stablecoins

Stability of the underlying reserves: the risk that the reserves backing the stablecoin are not sufficient to maintain the peg value of the stablecoin which exposes the holder to the credit risk of the issuer (in some cases, unregulated fintech companies)

Run risk: even if reserves are sufficient, the stablecoin could still be liable to a run if they face mass redemptions alongside other market shocks. For example, Circle’s USDC de-pegged from the US dollar following the collapse of Silicon Valley Bank in 2023 with market rumours about stablecoin deposits held at the bank (falling to 88c before recovering to 96c).

Regulation: regulators are tackling this emerging industry in different ways.

Financial crime risk: Chainalysis, a firm that monitors blockchain activity, estimates that around USD50bn was received by illicit wallet addresses in 2024, 63 per cent of which was in the form of stablecoins. Regulators around the globe will need to grapple with these risks as part of the regulatory rollout.

Selected current regulation of stablecoins

US: The GENIUS Act passed in July 2025 establishes the US regulatory framework for payment stablecoins. It requires US regulated stablecoins to invest their reserves in high quality liquid assets such as money funds, Treasuries and bank deposits.

Europe: MiCA, a set of rules that came into effect at the end of 2024 covering the wider crypto industry, set out specific rules for stablecoins. Issuers must be regulated in Europe as a credit institution, or an electronic money institution and reserves have to be in deposits with European financial institutions (they may also be able to hold EUR government bonds but not immediately clear). EURC (Circle’s EUR stablecoin) is only €200m in size and is fully backed by bank deposits with no other assets held in reserve.

Hong Kong: Legislation came into effect in August 2025 to establish a regulatory regime for issuers of stablecoins in Hong Kong. Issuers must maintain a pool of reserve assets that must be “of high quality and high liquidity with minimal investment risks” with a market value that must always be at least equal to the outstanding value of the stablecoin. MMFs are permitted as stablecoin reserves under the guidance published by the HKMA.

UK: The UK crypto regulatory framework was released in 2023 with an intention to finalise this year. Crypto assets and stablecoins will be incorporated into existing financial regulation rather than creating bespoke regulation. There is no clarity yet on permitted types of reserve assets for stablecoins.

Tokenisation

Distributed ledger technology (DLT) has long been associated with cryptocurrencies and in particular Bitcoin. The blockchain is one form of DLT and other forms have emerged as the usage of the technology extends. The terminology of blockchain and DLT are often used interchangeably.

The DLT operates based on one single immutable record that has been verified by consensus across a decentralised network. In traditional systems, each participant in an ecosystem operates their own independent database and they undertake reconciliations of their own records to counterparts. The DLT moves away from that concept of individual databases at each firm to the concept of a single decentralised record that participants access via nodes on a network. Each allowed node can view and validate activity. This creates a single view for all participants and an immutable record eliminating the duplication of records prevalent in legacy technology.

Tokenisation is the process of converting the ownership of assets or rights (including financial assets, physical assets, and even intangible assets) into digital tokens on the DLT, enabling these assets to be traded or transferred in the form of tokens on a blockchain network. In the case of a mutual fund, each token could represent a whole fund unit / share or a fraction thereof. Transactions are processed on the DLT by means of “smart contracts”, self-executing computer programs that are integral to the token. The smart contract will complete any operational, compliance, tax or accounting rules required to process and validate a transaction.

The tokenisation of MMF units has emerged as an early and important use case in the broader market wide push to tokenise different asset classes. The characteristics of the DLT to increase portability, deliver almost instantaneous settlement and reduce operational friction have the power to enhance the experience of a MMF investor and enable new use cases in the future.

The ability to transfer on-chain currency reserves into a tokenised MMF will offer an investor a return on their holding that is not currently available elsewhere on-chain within the digital ecosystem.

Observed approaches to tokenisation to date

The approach to the tokenisation of funds is still evolving with different models emerging in response to different use cases and / or regulatory and legal constraints. While the DLT may eventually replace most participants in the value chain, the focus of efforts to date has been limited to the activities of the transfer agent (TA). All other forms of the fund administration process remain untouched.

So far, two key approaches have emerged:

-

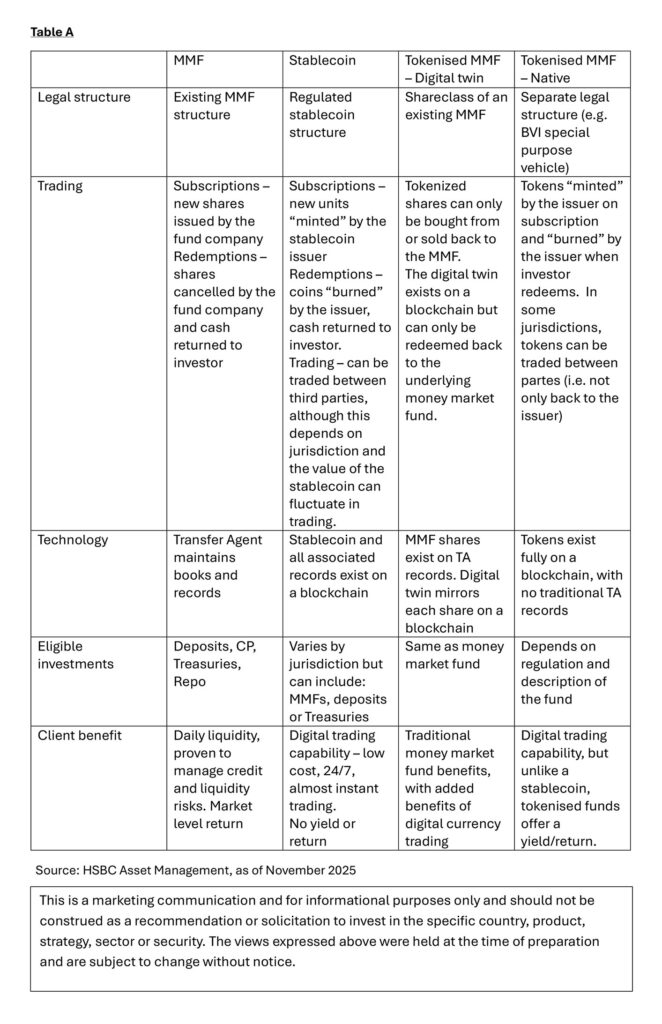

Digital twin (non-native tokenisation) – maintaining a digital record in parallel on the DLT

A token is created on the DLT that represents the ownership of the unit / share of a fund. Under this model, the fund still issues its units / shares in the traditional way, recording them on the analogue register at the TA, and the blockchain records an additional “mirror recording” or “twin” of that asset.This has the benefit of leveraging the scale of existing funds while maintaining the safety and regulatory framework MMF investors require.

There is no change to the existing operation of the fund, its regulatory status or construct. Investors in the fund must complete all normal AML/KYC onboarding processes as they do today. It is worth noting that the AML / KYC process has not yet moved on-chain.

In the MMF industry, we have seen this approach deployed in several areas, the collateral use case (see section below) is the most prevalent to date. It is worth noting that although there is a lot of activity, the scale of AUM remains a small fraction of the overall MMF industry.

-

Digitally native tokenisation

Under this model the fund’s register is recorded completely on the DLT and the fund issues digital tokens rather than units / shares. Subscription / redemption transactions are settled on-chain with digital currency. They often offer the ability to move off-ramp. Regulators are taking a cautious approach and often require the fund to maintain a parallel analogue record.

Today’s use cases

Collateral: Collateral managers deploying the blockchain as their recordkeeping system of choice. Until recently, the early adopters in this space have been limited to private closed networks. The collateral manager typically operates an omnibus structure, akin to a fund / platform distributor, whereby they make one investment to the fund via the traditional analogue route. They track beneficial ownership of the underlying holders by creating tokens. The DLT enables instant transfer of tokens between collateral giver and receiver accounts in real time. The units at the TA are under the control of the collateral agent, as with any omnibus platform today, and they create or redeem units on a net basis. While collateral managers have built these solutions, we have yet to see broader take-up with most transactions limited to proof of concept.

Tokenisation agents: the MMF puts a distribution agreement in place with an agent who again often operates an omnibus account structure and uses the DLT to record the interests of the underlying beneficial owner.

Distribution networks: at least one technology provider has built a distribution network solution which effectively provides a token conversion tool for on-chain investors. An investor will onboard directly with the underlying fund in the same way they do today, and the TA will maintain their holding on the share register. The network provider translates the blockchain originated transaction to a traditional format accepted by a TA (Swift, flat file) effectively replicating the trading portals common in the MMF industry today. Again, a parallel record is maintained on the DLT by the network provider. This opens the opportunity for new customer segments and channels.

Third party vs issuer tokenisation: Most of the tokenisation to date has been implemented by third parties and not the managers or the funds themselves. There are various drivers for this, some are constrained by regulation in their jurisdiction, some may have a very narrow use case or see it as a valuable way to start their tokenisation journey. Regulatory clarity in Luxembourg has enabled one MMF manager to go as far as tokenising a share class of an existing fund although we understand this is again achieved through the maintenance of a parallel record.

Selected current regulation of tokenised funds

There continues to be a divergence in legislative and regulatory frameworks across the globe. European managers are approaching tokenisation cautiously, building experience slowly by working with third parties in the first instance. We have observed a number of smaller launches from smaller money managers in jurisdictions that have amended legislation to allow native tokenisation.

Ireland and Luxembourg are key jurisdictions for MMFs in Europe. Ireland has not yet progressed legislation to allow fund tokenisation and we understand there is little to no activity yet. By contrast, Luxembourg has been proactive in creating legislative and regulatory frameworks to facilitate the launch of digitally native funds. This enabled Franklin Templeton to launch the first natively tokenised UCITS MMF, regulated under European Money Fund regulation, in Luxembourg, in October 2024. There is no publicly available data on AUM but we understand this is small at approximately USD10m.

Other European jurisdictions such as France and Germany have also progressed their frameworks. The AMF has authorised one MMF in France which is targeting crypto investors. Growth to date has been modest, and since its launch in 2024 the Spiko fund has grown to USD114m.

Hong Kong and Singapore see digital enablement as a differentiating factor and have been proactive in opening sandboxes to facilitate the launch of digitally native funds. In Q4 2024 UBS and Standard Chartered & Wellington launched their own fully native funds in Singapore targeting web3.0 investors and the collateral use cases. Both funds have been working with Ondo Finance to offer off-ramp solutions. In February 2025, a Chinese asset manager, China AMC, launched an HKD Digital Money Market Fund in Hong Kong targeting retail customers. It has grown to HK USD 970m.

The US has seen little activity from managers to date with activity focused on collaborations with collateral platforms who are placing their collateral management processes on-chain operating the omnibus models highlighted earlier. The SEC still designates any instrument that is issued on the blockchain as a crypto asset security. Publicly registered funds are heavily intermediated by the Broker Dealers and they are prohibited from taking custody of a crypto based security which effectively blocks distribution of a tokenised fund. This may change quickly but at present we understand this is not a priority for the current administration. Consequently, US use cases for digitally native funds have focused on limited distribution of private funds, like BlackRock’s BUIDL, domiciled in the British Virgin Islands.

Summary

Distributed ledger technology represents an opportunity to revisit the way in which treasurers can invest their surplus funds in line with their board approved risk appetites. It offers significant savings in costs, reduced FTE effort, improved risk management and controls (while recognising the emergence of new risks), reduced counterparty risks, faster settlement and greater transparency. We expect a gradual progression in fund tokenisation as confidence in the technology grows and participation increases.

From a money market fund user perspective, the ability to move (transfer, trade, pledge) units without necessarily redeeming offers significant advantages. Their use as collateral pledged to third parties but also intercompany transfers can only enhance the utility of a money fund holding.

We have yet to see scale solutions for the custody of wallets that will keep secure the DLT private keys necessary to secure the holding for institutional investors. For these reasons, we anticipate it will take some time to reach a point where the full advantages of DLT can be harnessed.

There is also a way to go before AML / KYC processes and controls can move on-chain to the satisfaction of risk managers and regulators. At present, liquidating a holding requires the token holder to return the token to the fund or the platform provider.

Another impediment is the lack of regulatory clarity and consistency in approach is driving multiple different routes which we expect to continue for the foreseeable future.

So, while for most treasurers, the use of DLT products remains theoretical, there is a growing number actively exploring them (and in fact a few using them). As such, it is important for treasurers to understand the technology and terminology and to keep abreast of developments in this sector so that they are ready to engage with the market when they feel it is appropriate.

Explore our Liquidity Solutions

Important information

For Professional Clients and intermediaries within countries and territories set out below; and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager’s skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in Emerging Markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation and are subject to change at any time. These views may not necessarily indicate current portfolios’ composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients’ objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets. Investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

All data from HSBC Asset Management unless otherwise specified. Any third-party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group). The above communication is distributed by the following entities:

- In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws;

- in Bermuda by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority;

- in Chile: Operations by HSBC’s headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Obtain information about the state guarantee to deposits at your bank or on www.cmfchile.cl;

- in Colombia: HSBC Bank USA NA has an authorized representative by the Superintendencia Financiers de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution;

- in France, Belgium, Netherlands, Luxembourg, Portugal, Greece, Finland, Norway, Denmark and Sweden by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026);

- in Germany by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients);

- in Hong Kong by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This video/content has not be reviewed by the Securities and Futures Commission;

- in India by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India;

- in Italy and Spain by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026) and through the Italian and Spanish branches of HSBC Global Asset Management (France), regulated respectively by Banca d'Italia and Commissione Nazionale per le Societa e la Borsa (Consob) in Italy, and the Comisión Nacional del Mercado de Valores (CNMV) in Spain;

- in Malta by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act;

- in Mexico by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversion, Grupo Financiero HSBC which is regulated by Comisión Nacional Bancaria y de Valores;

- United Arab Emirates, Qatar, Bahrain & Kuwait by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Securities and Commodities Authority in the UAE under SCA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient’s country of residence and therefore may not be subject to supervision of the local regulator in the recipient’s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient’s country of residence.

- in Peru: HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Peru whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Peru and is not for public distribution;

- in Singapore by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore;

- In Switzerland by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website; if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (“SBA”) Brochure “Risks Involved in Trading in Financial Instruments;

- in Taiwan by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan);

- Turkiye by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations.

- in the UK by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority;

- and in the US by HSBC Global Asset Management (USA) Inc. which is an investment adviser registered with the US Securities and Exchange Commission

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy

Copyright © HSBC Global Asset Management Limited 2025. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Global Asset Management Limited.

Content ID: D059881_V1.0; Expiry Date: 26.11.2026