Uncertainty: A Practitioner's Guide

Introduction

Uncertainty is a fundamental aspect of the economic landscape, and it is as high as it has ever been. This paper aims to provide an overview of the current state of uncertainty in markets, the economy and treasurer decision making. We will assess its impact on economic activity, and our views on portfolio positioning and expectations.

The Nature of Uncertainty

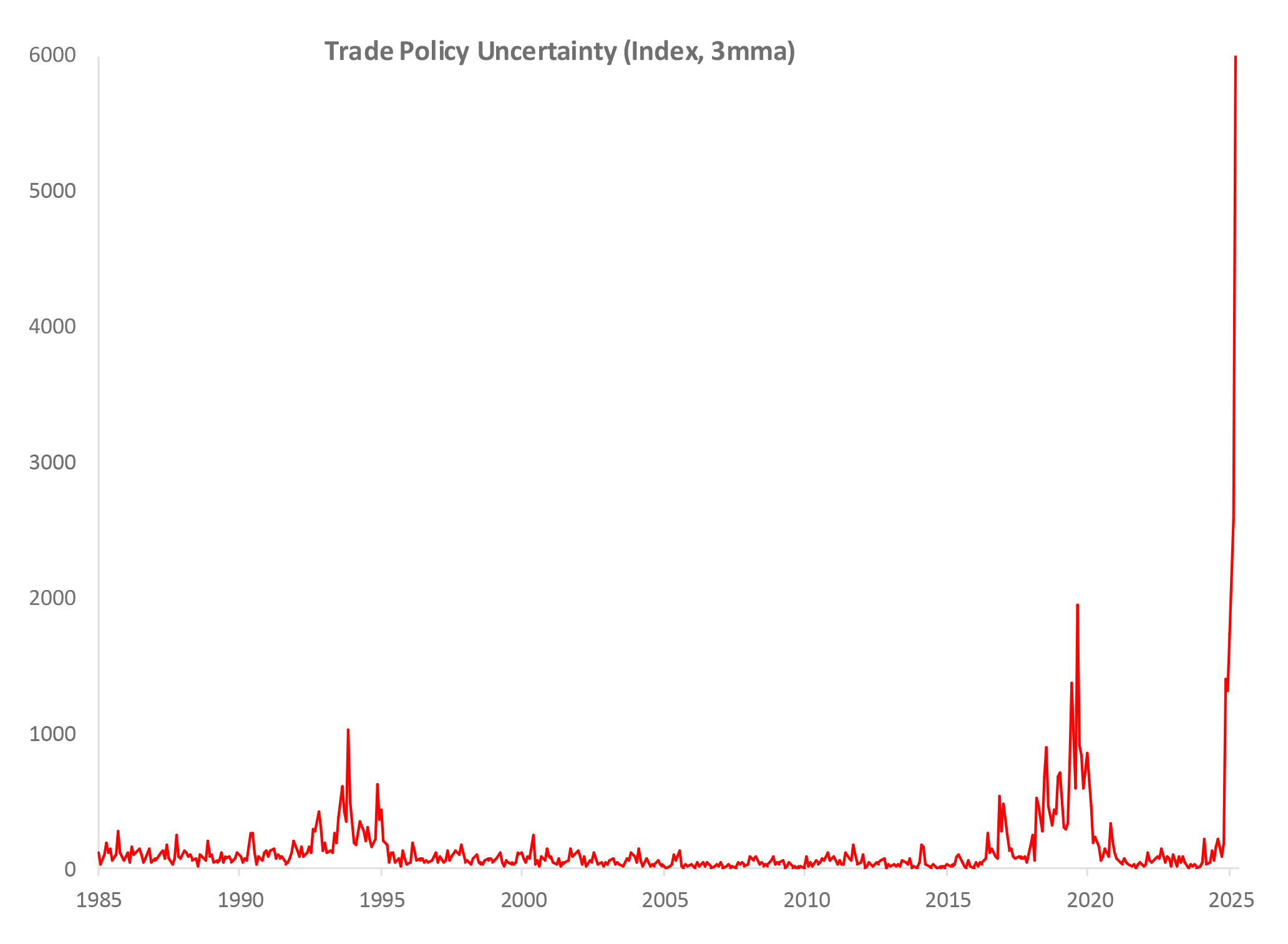

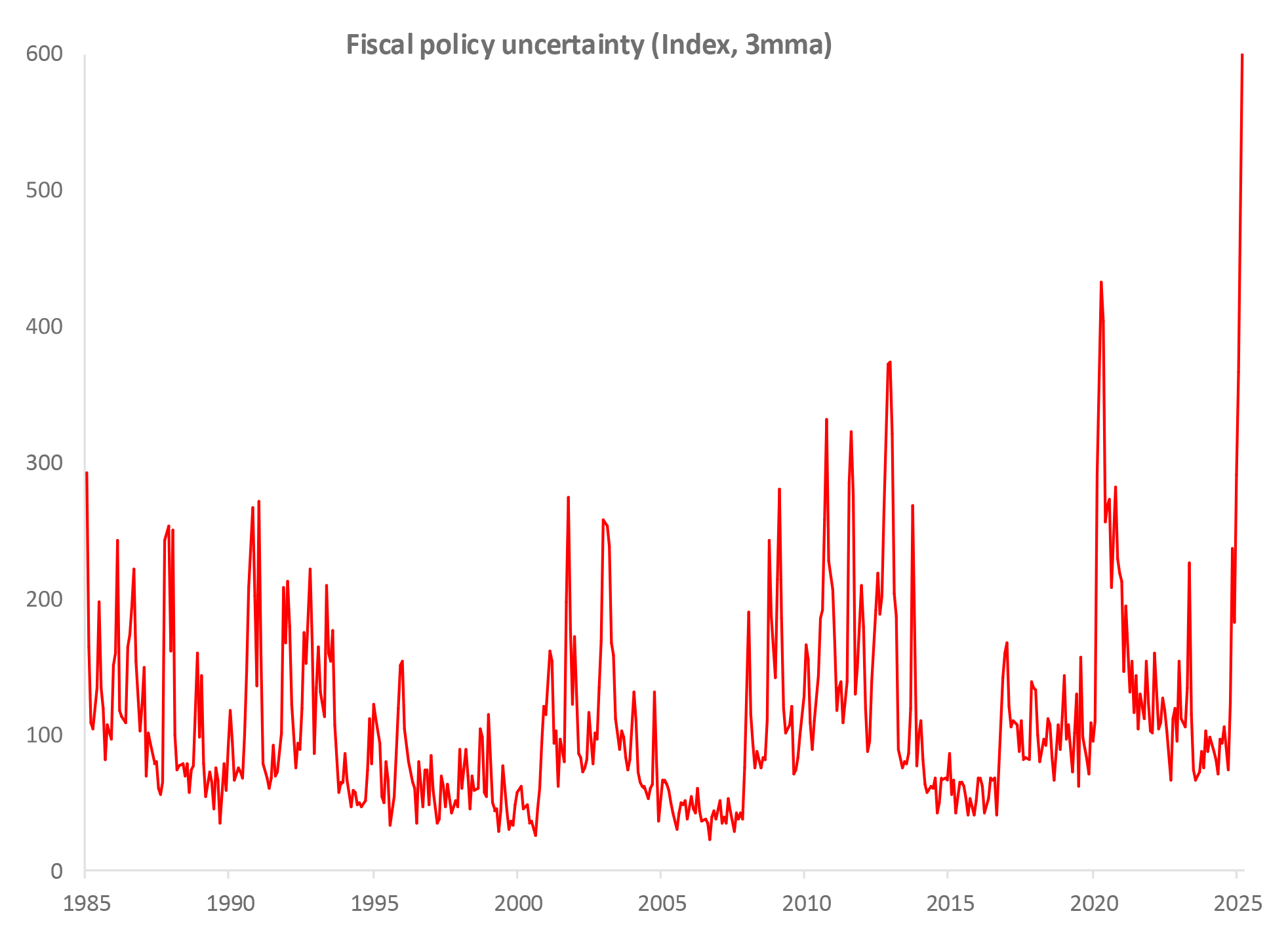

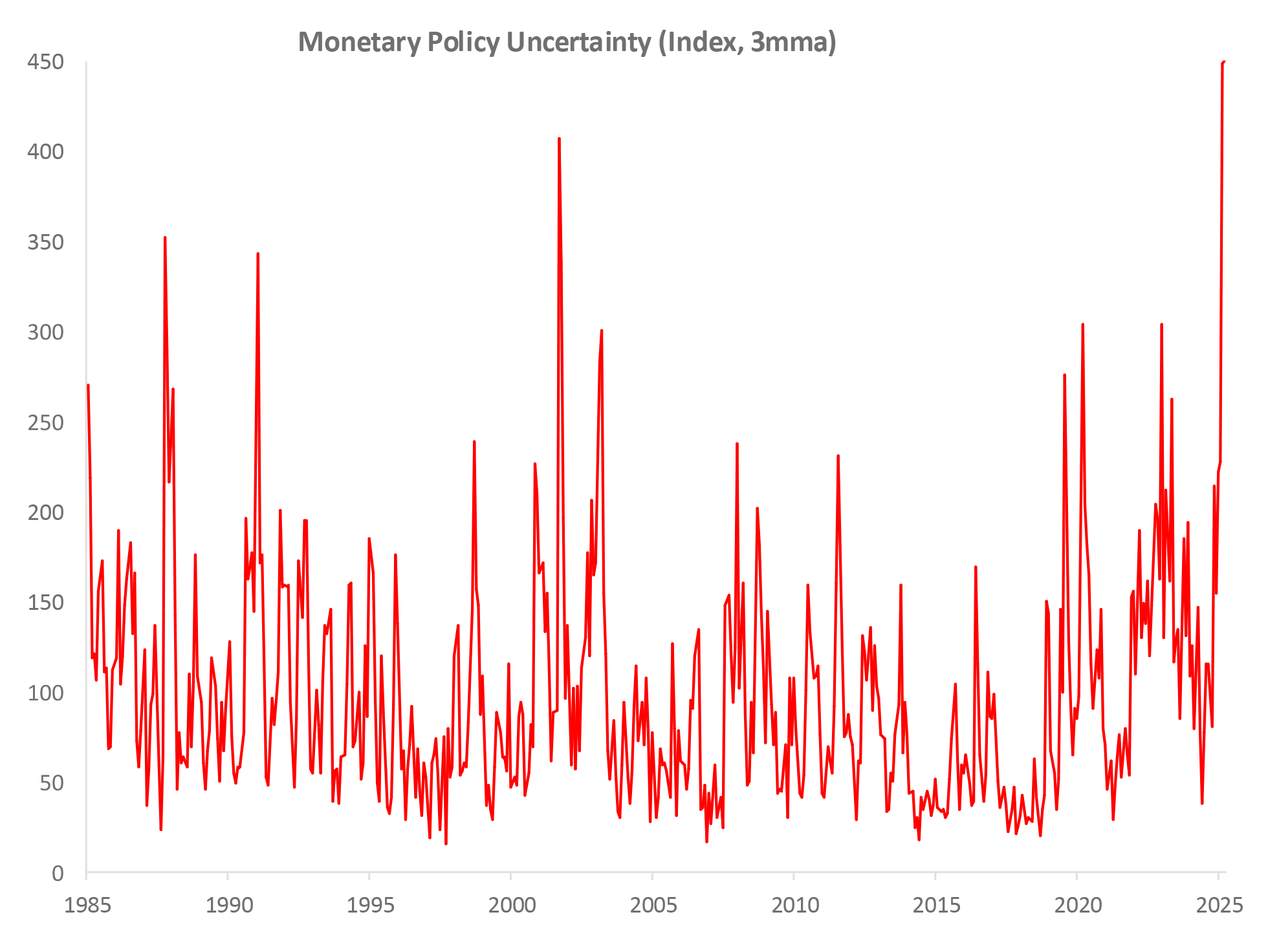

Uncertainty can be proxied through various surveys and quantitative measures to construct indices to compare previous episodes of political or economic tension (Fig.1). Looking back to the mid 1980’s we have witnessed numerous events that have contributed to heightened geopolitical and market uncertainty, including Black Monday, two Gulf wars, a Russian default, the collapse of Long-Term Capital Management, the dotcom bubble, 9/11, the Asian financial crisis, the global financial crisis, the Eurozone sovereign crisis, and the global COVID-19 pandemic. Yet today, as the charts below demonstrate, uncertainty is, in the words of chair of the European Central Bank, exceptional.

Fig.1 Measures Of Policy Uncertainty Have Spiked

Policy uncertainty typically means:

- Higher stock market volatility,

- Wider credit spreads,

- Higher equity premium

Click image to enlarge.

Click image to enlarge.

Click image to enlarge.

Source: Macrobond, Bloomberg, HSBC Asset Management, May 2025. The commentary and analysis presented in this document reflect the opinion of HSBC Asset Management on the markets, according to the information available to date. They do not constitute any kind of commitment from HSBC Asset Management. Consequently, HSBC Asset Management will not be held responsible for any investment or disinvestment decision taken on the basis of the commentary and/or analysis in this document. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target. The views expressed above were held at the time of preparation and are subject to change without notice.

Despite the varied nature of the events noted above, the common thread is that uncertainty affects every economic actor, from individual investors to corporate decision-makers. The very existence of uncertainty leads to mechanically lower growth as decisions are deferred, and bets are hedged.

Impact on Economic Activity

The impact of uncertainty on economic activity is profound. When faced with uncertainty, individuals and companies tend to postpone, delay, or hedge their decisions. This behaviour dampens economic activity and leads to slower growth. For example, higher macro uncertainty weighs on growth characterised by increased unemployment rates, lower job openings, and increased precautionary saving. Discretionary spending, particularly on large-ticket items and luxuries, is typically the first to be cut.

Uncertainty also affects investment decisions. Companies may delay or cancel investment projects due to the unpredictable economic future. This can lead to lower productivity growth and reduced innovation. Additionally, uncertainty can impact consumer confidence, leading to lower spending and higher savings rates. This behaviour further dampens economic activity and can lead to a slowdown in economic growth.

Moreover, the impact of uncertainty is not uniform across sectors. Some industries, such as technology and healthcare, may be more resilient to uncertainty due to their innovative nature and essential services. In contrast, sectors like manufacturing and retail, where capital expenditures are planned years in advance may be more vulnerable to changing economic winds.

This, of course, affects the treasury department of corporations on every level. Cash requirements become increasingly uncertain and forecasting exponentially more complicated. And that’s without trying to optimise with the backdrop of central banks facing the exact same uncertainties, but in aggregate.

Our View

Given the current state of uncertainty, our view is that it is essential to adopt a cautious approach to portfolio positioning. Central banks' decisions, or lack thereof, shape short-term investment strategies. Money market fund managers typically set their medium-term expectations on a six to twelve months pathway, and gradually tweak strategies based on tactical adjustments.

Our baseline macro scenario is for tariffs to settle close to current levels, leading to below-trend growth and above-target inflation in the US, while other major economies experience more trend-like growth and limited inflation pressures. Policy uncertainty remains high, and the data flow is likely to remain bumpy. Risk asset valuations are stretched in many areas, meaning that any deterioration in corporate fundamentals could add to market volatility.

In Europe, Germany's fiscal revolution is a significant development that should lead to a fiscal boost for the Eurozone. The new rules allow states to run deficits, and increased defence spending and infrastructure investment are expected to provide a much-needed fiscal boost. However, the deployment of investment-led fiscal expansion can take time, and the real picture may be less than the headlines suggest.

In the UK, the possibility of stagflation, characterised by high inflation and low growth, is a distinct concern. The UK economy has been defying pessimistic forecasts, but without government-produced GDP expenditure, growth has barely budged since COVID-19. The Beveridge curve, which tracks the relationship between employment and job openings, suggests that the UK is close to a transition point, moving from low unemployment and high vacancies to high unemployment and low vacancies. Structural dynamics such as skills mismatches, reduced labour mobility, and low productivity can exacerbate this situation, leading to higher unemployment, lower vacancies, and relatively high wages.

Strategy

Considering the current level of elevated uncertainty, our strategies currently place even greater emphasis on diversification (of credit risk but also interest rate positioning) and risk management. We believe that a well-diversified portfolio can not only reduce credit risk and increase portfolio liquidity characteristics but also help mitigate the impact of uncertainty on investment returns. By spreading investments across different maturities, instrument type (fixed or floating), and issuers, exposure to any one of a range of outcomes is reduced.

Regular review and adjustment of allocations based on changing market conditions and economic outlooks is vital. As is constant vigilance for the sort of idiosyncratic issuer credit that can reveal itself in volatile markets. The same volatility in central bank expectations can produce tactical opportunities to extend duration where our strategic views differ from the market.

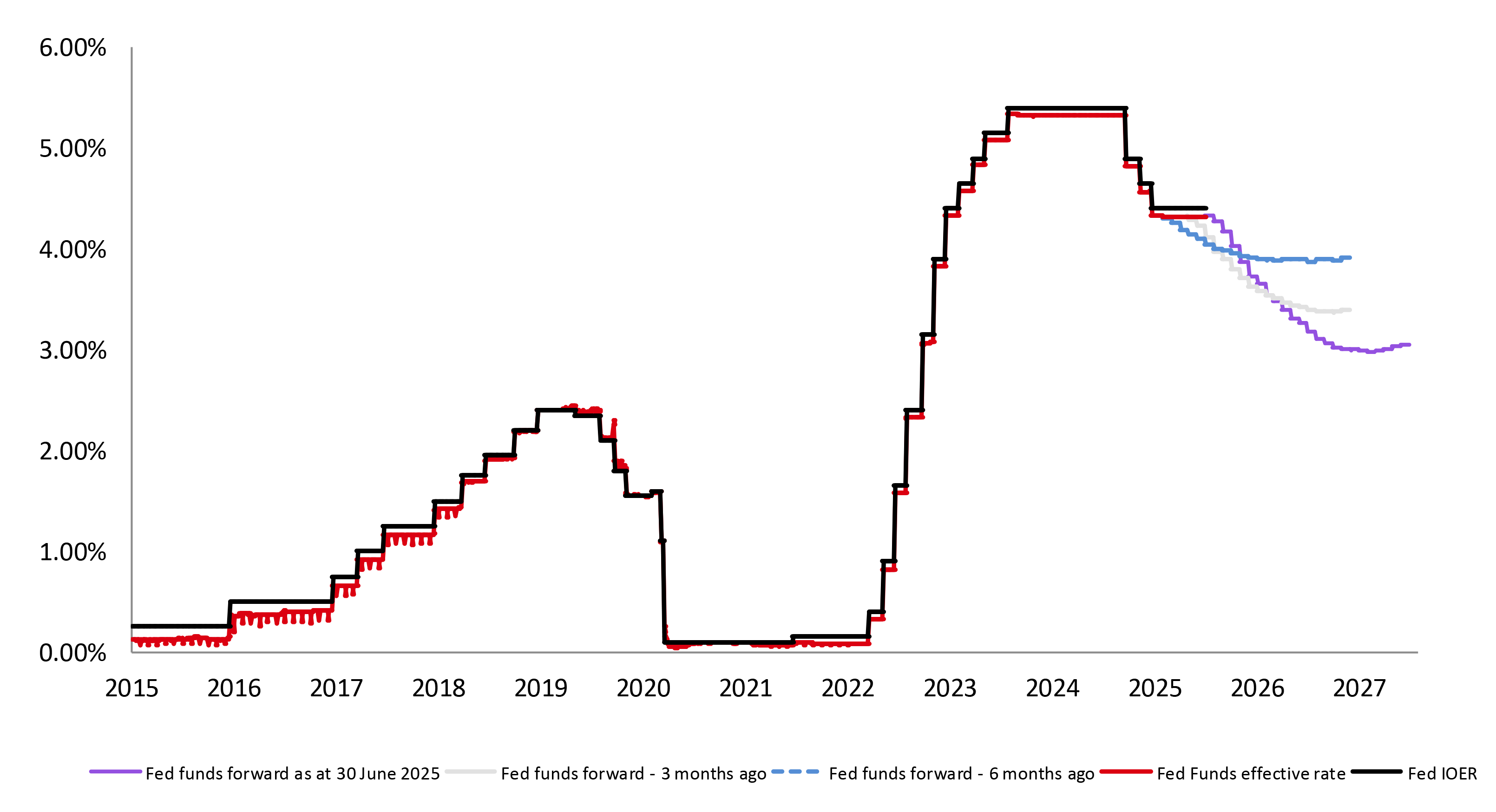

Money market rates in the United States

Click image to enlarge.

Sources: Bloomberg, HSBC Asset Management - FED funds forward rates are based on Fed Fund futures.

The above figures relate to the past and past performance should not be seen as an indication of future performance.

Any forecast, projection or target where provided is indicative only and is not guaranteed in a way. HSBC Asset Management (France) accepts no liability for any failure to meet such forecast, projection or target.

Expectations

Looking ahead, we expect uncertainty to remain a significant factor in the economic landscape. Our long held strategic view is that rates will ultimately be reduced by more than the market currently expects. i.e. slower growth will lead to renewed disinflation and, ultimately more central bank easing. Regarding specific markets this is certainly most true in the US, while the UK seems to be facing the greater risk of stagflation (high inflation, low or negative growth) creating significant challenges for monetary policy. The EU is probably closest to a neutral level of interest rates. The anticipated fiscal impulse and entrenched disinflation contrast favourably with the US and UK. Ongoing geopolitical tensions, trade disputes, and policy changes will continue to create an unpredictable environment for investors. In Asia, where certain money markets are pegged to the US dollar (China, Hong Kong) and those that are not have exposure to global trade flows and/ or a basket of currencies (Australian and Singapore dollars), effects can be amplified to an even greater extent, leading to significant interest rate volatility. Our local currency money market strategies are valued by investors for combing local technical know-how with a consistent global investment process.

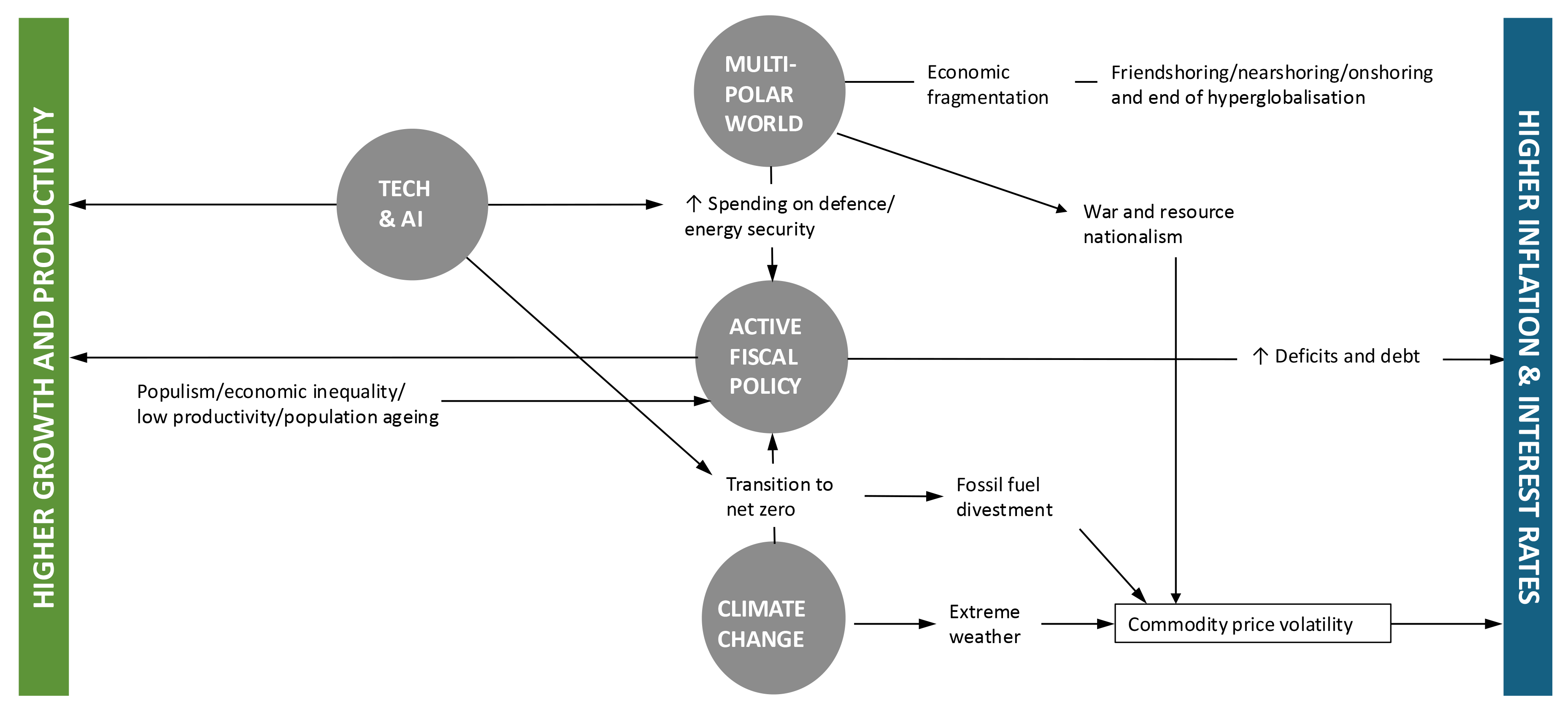

On a medium-term horizon, the shifting sands of technological innovation, active fiscal policy, economic fragmentation, and climate change create the potential of a new economic paradigm to replace that of a unipolar global economy anchored by US exceptionalism. This will create both threats and opportunities for economies around the world.

We are transitioning to a new economic paradigm

Click image to enlarge.

Source: HSBC Asset Management, April 2025. The commentary and analysis presented in this document reflect the opinion of HSBC Asset Management on the markets, according to the information available to date. They do not constitute any kind of commitment from HSBC Asset Management. Consequently, HSBC Asset Management will not be held responsible for any investment or disinvestment decision taken on the basis of the commentary and/or analysis in this document. For illustrative purposes only. The views expressed above were held at the time of preparation and are subject to change without notice.

Conclusion

In conclusion, uncertainty is an inherent part of the economic landscape, and its impact on economic activity is significant. Experience year to date in 2025 may be a foretaste of an extended period of structural uncertainty and, in the years to come, central banks may become less correlated than investors are used to.

Our view is that adopting a globally consistent, cautious, and diversified approach to liquidity strategy is essential to helping businesses to navigate this period of prolonged volatility. Regardless of how divergent country level economic and central bank policies become, our approach to managing the risks will be consistent. By understanding the nature of uncertainty and its effects, we can better position ourselves to manage our liquidity strategies and deliver on our core objectives. For treasurers, trying to manage risk and identify the opportunity, is becoming an increasingly complex activity. And trying to maintain a globally consistent set of principles across different jurisdictions with different rules only adds to compliance risks. It is therefore critical that treasurers lean into the expertise of their asset managers to ensure that the best tools and expertise are being applied to manage their liquidity.

A focus on risk management should always be the backbone of any liquidity strategy. Historically elevated levels of uncertainty underline this need more than ever.

Source: HSBC Asset Management, July 2025. The views expressed above were held at the time of preparation and are subject to change without notice. While any forecast, projection or target where provided is indicative only and not guaranteed in any way, HSBC Global Asset Management (UK) Limited accepts no liability for any failure to meet such forecast, projection or target. This information shouldn't be considered as a recommendation to invest in a particular sector or country shown.

Explore our Liquidity Solutions

Important Information

For Professional Clients and intermediaries within countries and territories set out below; and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager’s skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in Emerging Markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation, and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets. Investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This document is a global view of the recent evolution of the economic conditions. This is a marketing support which does not constitute neither an investment advice or a recommendation to buy or sell investment. This commentary is not the result of investment research and is not subject to legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

All data from HSBC Asset Management unless otherwise specified. Any third party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group). The above communication is distributed by the following entities:

- In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only, and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws;

- in Bermuda by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority;

- in Chile: Operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Obtain information about the state guarantee to deposits at your bank or on www.cmfchile.cl;

- in Colombia: HSBC Bank USA NA has an authorized representative by the Superintendencia Financiera de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution;

- in France, Belgium, Netherlands, Luxembourg, Portugal, Greece, Finland, Norway, Denmark and Sweden by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026);

- in Germany by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients);

- in Hong Kong by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This video/content has not be reviewed by the Securities and Futures Commission;

- in India by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India;

- in Italy and Spain by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026) and through the Italian and Spanish branches of HSBC Global Asset Management (France), regulated respectively by Banca d’Italia and Commissione Nazionale per le Società e la Borsa (Consob) in Italy, and the Comisión Nacional del Mercado de Valores (CNMV) in Spain;

- in Malta by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act;

- in Mexico by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversión, Grupo Financiero HSBC which is regulated by Comisión Nacional Bancaria y de Valores;

- in the United Arab Emirates, Qatar, Bahrain & Kuwait by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Securities and Commodities Authority in the UAE under SCA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient’s country of residence and therefore may not be subject to supervision of the local regulator in the recipient’s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient’s country of residence.

- in Peru: HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Perú whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Perú and is not for public distribution;

- in Singapore by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore;

- In Switzerland by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website; if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (“SBA”) Brochure “Risks Involved in Trading in Financial Instruments;

- in Taiwan by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan);

- in Turkiye by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations.

- in the UK by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority;

- and in the US by HSBC Global Asset Management (USA) Inc. which is an investment adviser registered with the US Securities and Exchange Commission.

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy.

Copyright © HSBC Global Asset Management Limited 2025. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Global Asset Management Limited.

Content ID: D048625; Expiry Date: 01.07.2026