Download the full report PDF, 540KB

Market spotlight: A maturing eurozone market

The eurozone is increasingly behaving less like a cyclical allocation and more like a structural investment destination. Cross-border portfolio flows since 2023 illustrate this shift. Elevated geopolitical risk, tariff uncertainty and diverging global monetary policies have triggered broad portfolio reallocation towards Europe.

Immediately after the pandemic, eurozone investors displayed a pronounced home bias, with roughly half of their fixed income allocations held in domestic sovereign and corporate debt. By mid-2025, however, widening yield differentials encouraged greater exposure to foreign bonds as investors searched for carry and duration. The change reflected diversification, rather than a loss of confidence.

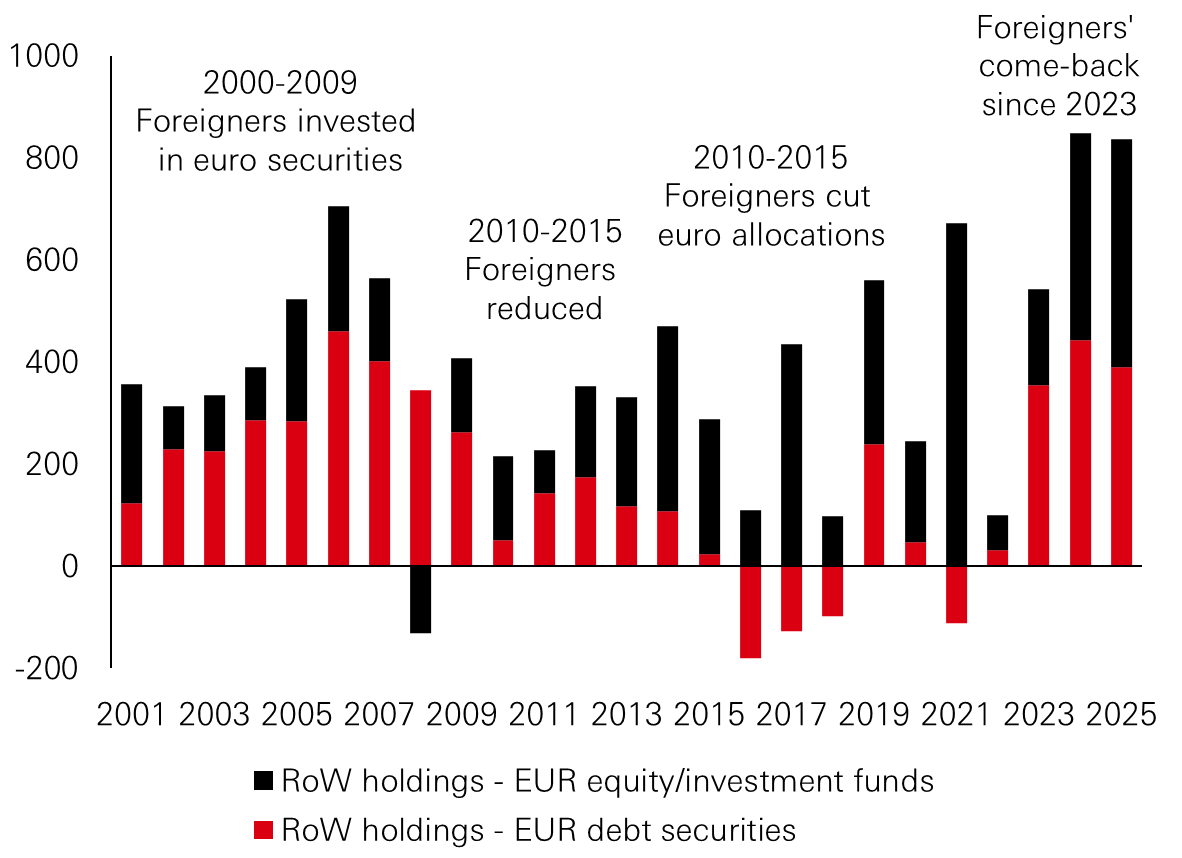

Crucially, outward allocation has not reduced foreign interest in Europe. Portfolio inflows reached almost EUR 850 billion in 2024 and remained close in 2025 at EUR 830 billion. The modest decline was driven mainly by lower debt purchases, while equity demand remained resilient, suggesting investors increasingly view Europe as a stable allocation, rather than a tactical macro trade.

Figure 1: Foreign investment in euro securities – change in portfolio positioning (billion euros)

Click the image to enlarge

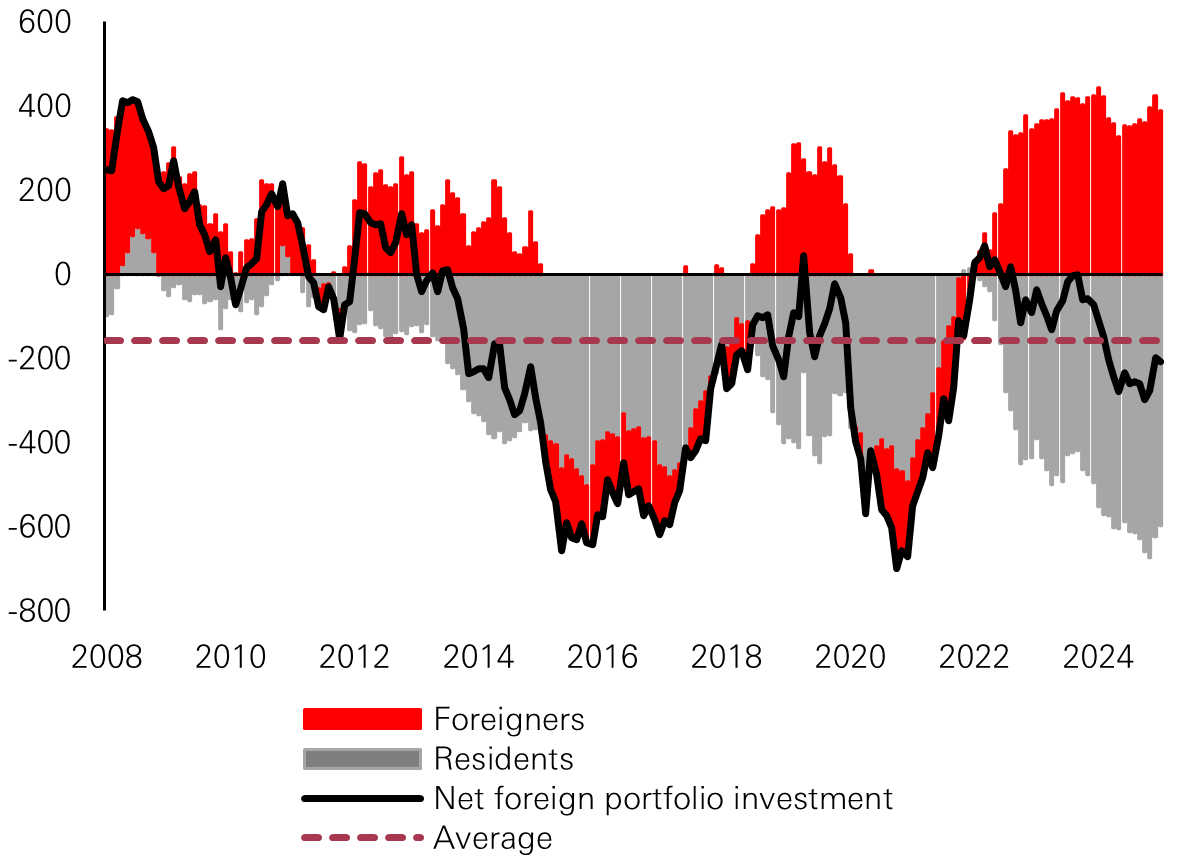

Figure 2: Foreign investment in eurozone debt securities (billion euros, 12 months sum)

Click the image to enlarge

Source: Refinitiv, European Central Bank, HSBC Asset Management. Data as of 9 March 2026.

Within sovereign markets, differentiation has become more pronounced. Germany has re-emerged as the region’s anchor safe asset, attracting record non-resident purchases of EUR 241 billion over the twelve months to November as positive yields returned to Bunds under ECB normalisation. France demonstrated the sensitivity of flows to politics, with inflows weakening during the 2024 election cycle before stabilising. Italy, by contrast, has seen sustained foreign participation following rating upgrades and improved stability, yet foreign ownership remains near one-third of outstanding bonds, leaving capacity for further inflows.

More revealing is the structure of capital flows. Cross-Atlantic allocation remains limited, with eurozone investors holding roughly a quarter of foreign US bonds, while US investors owning only about 8 per cent of eurozone bonds, but intra-European integration is deepening. French investors hold about 16 per cent of Italian debt and German investors roughly 13 per cent of French sovereign bonds, while regional ownership of Italian debt remains near 70 per cent.

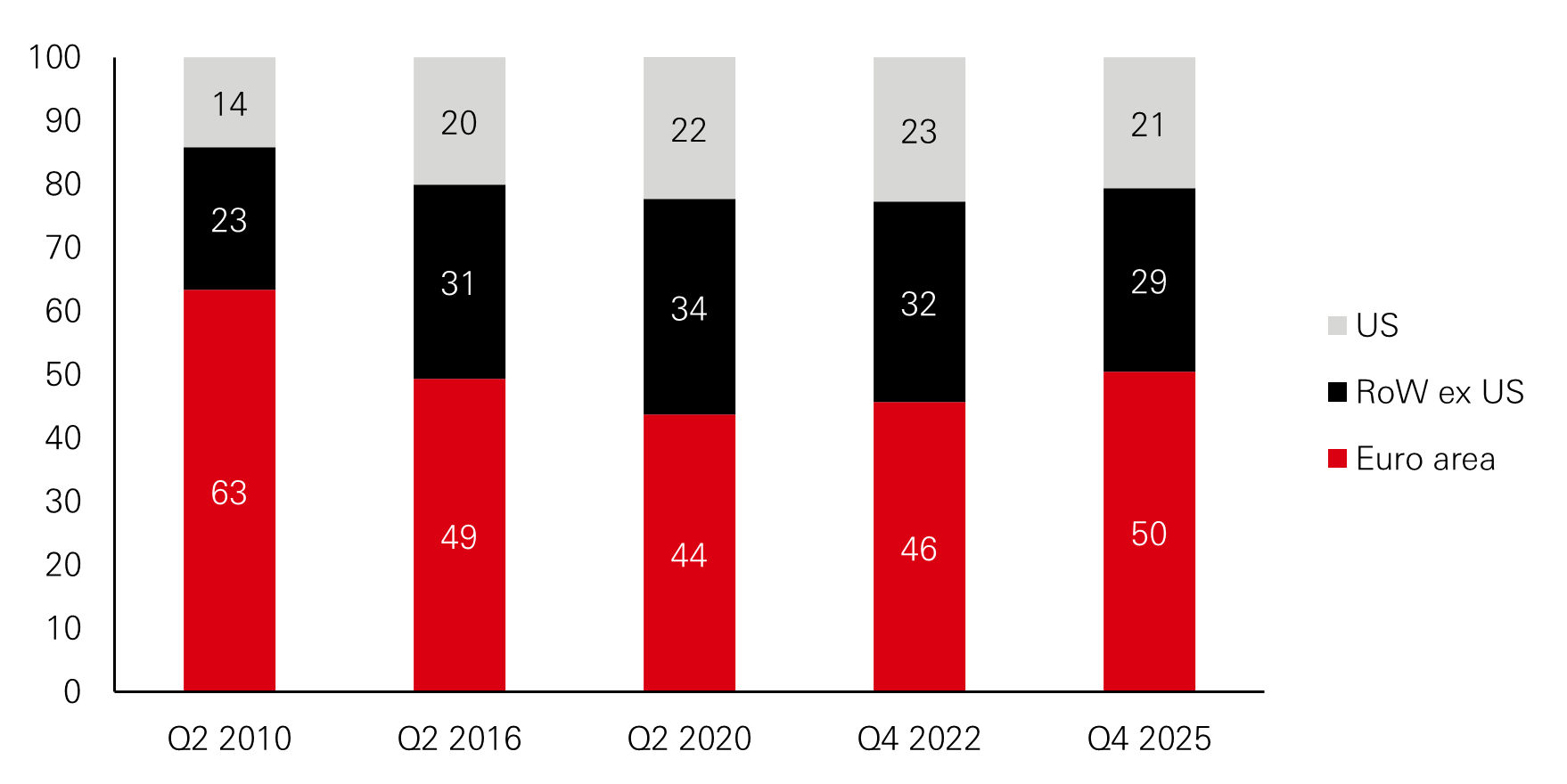

Figure 3: Debt securities held by euro area investment funds (%)

Click the image to enlarge

Source: Refinitiv, HSBC Asset Management. Data as of 12 February 2026

The broader implication is that allocation decisions now respond more to policy credibility, fiscal transparency and institutional coordination than to global risk sentiment. Inflation progress, EU funding programmes and coordinated fiscal initiatives have strengthened confidence in the policy framework. Europe is gradually transitioning from a recovery story into a maturing financial system whose diversification comes from internal dispersion rather than external capital dependence. That evolution provides the foundation for equity markets where Europe is re-establishing itself as a stable component within global portfolios as well as for fixed income markets where the definition of defensive assets itself is evolving.

European equities

Stabilisation rather than rotation

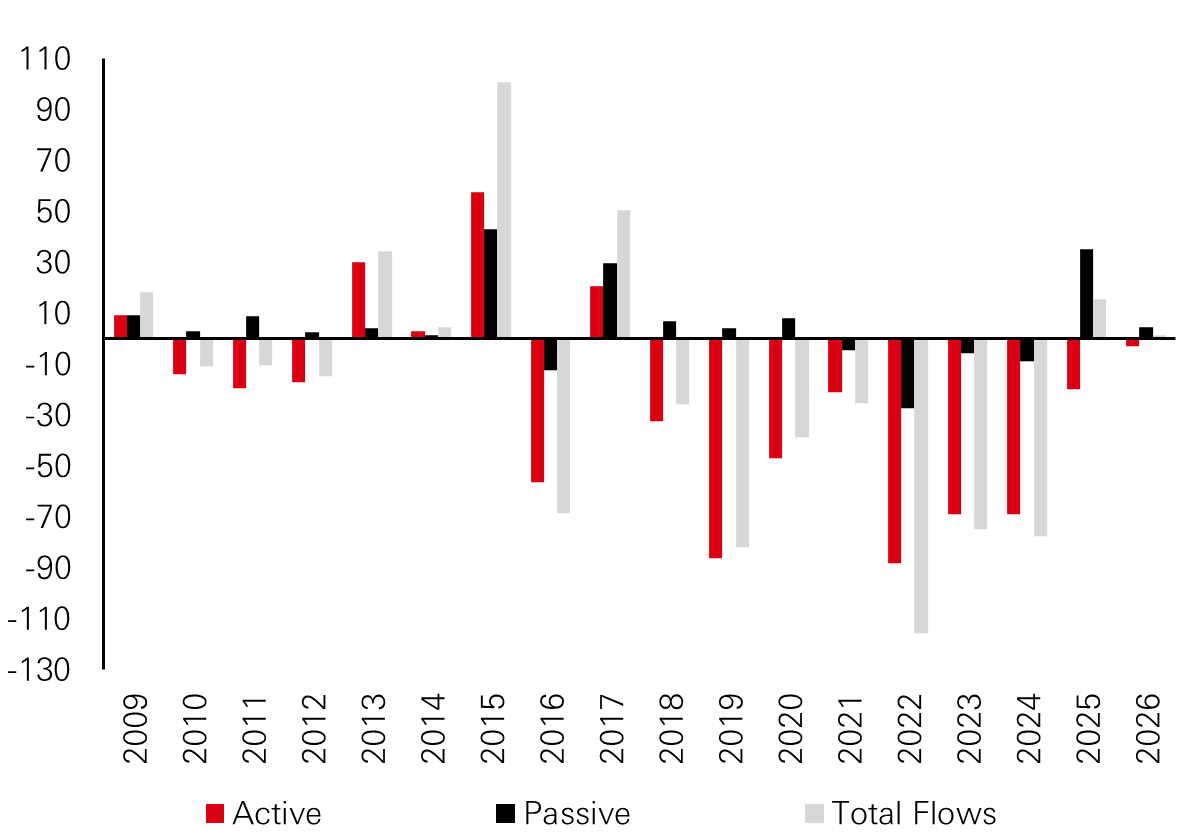

For over a decade, global portfolios steadily migrated toward US equities while Europe frequently acted as a funding source. Between 2009 and early 2026, US equity funds attracted roughly EUR 224 billion in net inflows, while European funds experienced EUR 316 billion of outflows - a divergence exceeding EUR 540 billion.

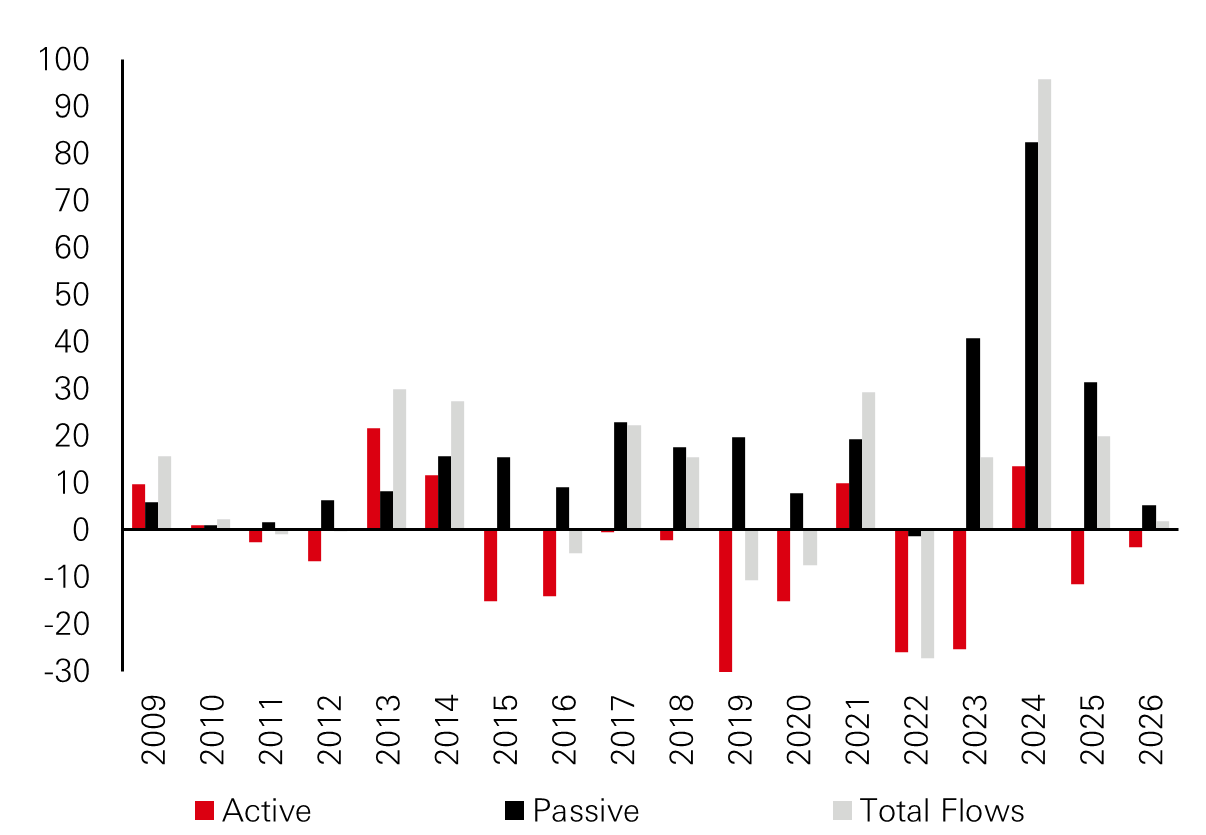

Two structural forces drove this imbalance. First was the shift from active to passive investing, where benchmark composition favoured US markets. Second was persistent US technology leadership. Although US active funds lost EUR 85 billion, passive vehicles attracted EUR 309 billion, producing strongly positive flows. Meanwhile, inflows into passive European funds of EUR 104 billion failed to offset the EUR 420 billion outflows from active funds.

Figure 1: US equity fund flows (2009 – YTD 2026)

Click the image to enlarge

Figure 2: Europe equity fund flows (2009 – YTD 2026)

Click the image to enlarge

Source: Refinitiv, Broadridge, HSBC Asset Management. Data as of February 2026

Recent data, however, has stabilised. Flows still favoured the US in 2023-24, but by 2025 and early 2026 the gap narrowed significantly. US equity funds received around EUR 19.9 billion and EUR 1.8 billion of inflows versus EUR 15.6 billion and EUR 1.7 billion into Europe. Crucially, the improvement in Europe is almost entirely passive. Investors are rebuilding exposure through index vehicles rather than discretionary stock selection, implying normalisation of asset allocation rather than renewed conviction in European alpha.

Euro area funds simultaneously increased US exposure from 18 per cent of assets in 2010 to 41 per cent by late-2025, yet a modest home bias has re-emerged since 2024. Investors are adding Europe alongside, not instead of, US holdings.

This matters because it confirms the shift identified in capital flow dynamics, which is that the Europe is no longer simply a cyclical trade. Valuation discounts, improving policy stability and steadier flows point toward equilibrium rather than rotation. Europe is becoming a complementary allocation – a diversification sleeve rather than a replacement for US growth exposure.

European fixed income

Redefining the defensive anchor

As eurozone market is maturing, European fixed income reveals where that maturation has the clearest portfolio implications. Historically, European bond framework had government bonds – especially German Bunds – for safety and corporate credit for incremental yield. That distinction is now less clear.

The starting point is supply. Germany’s historic fiscal pivot toward infrastructure and defence spending marks a break from decades of fiscal conservatism. Larger sovereign issuance reduces the scarcity premium that long underpinned Bund valuations. Government bonds remain liquid and systemically important, but they are no longer uniquely insulated from macro and fiscal dynamics. In practical terms, pure duration exposure now carries more policy and supply risk than in the past.

At the same time, corporate balance sheets entered this phase in relatively strong condition. Investment grade issuers maintain extended maturity profiles, healthy interest coverage and disciplined funding access. Credit spreads have remained contained despite tighter financial conditions, and total fixed income net supply is expected to stabilise, even as sovereign issuance increasingly crowds out corporate paper. That technical backdrop of constrained credit supply against structural institutional demand supports spread resilience.

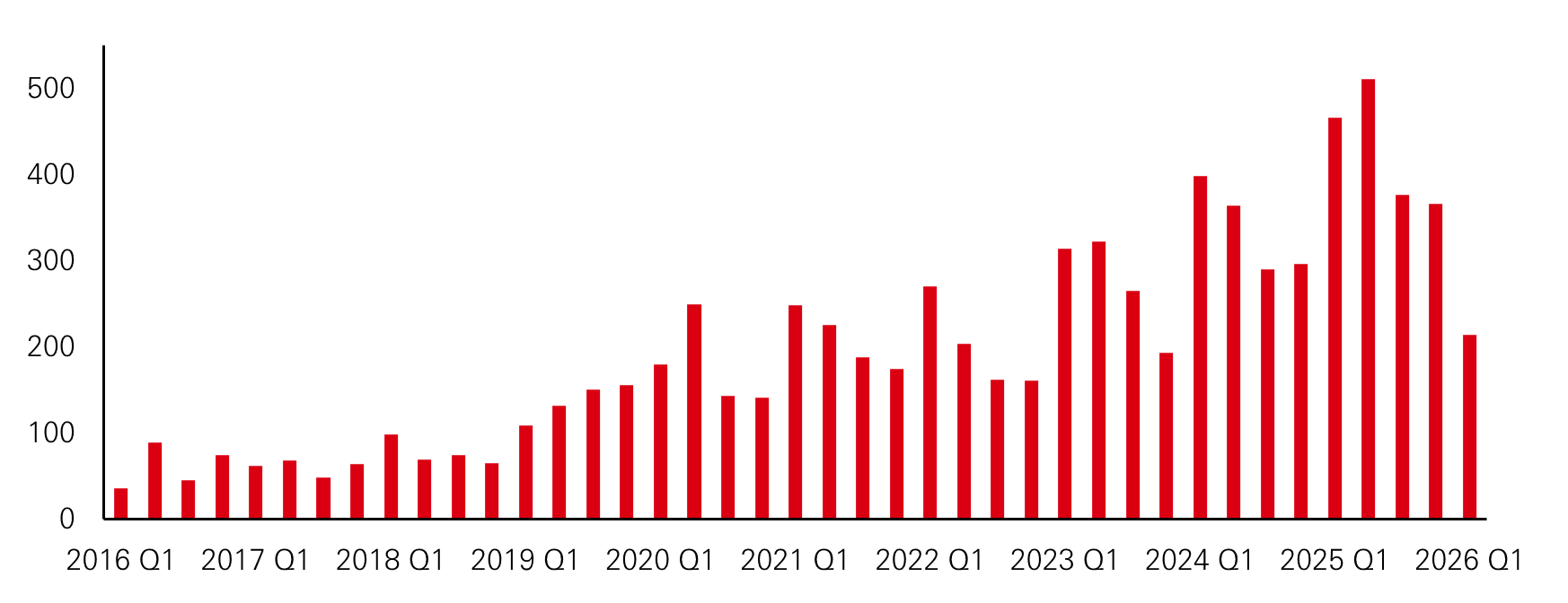

Figure 1: Euro Credit net supply (billions)

Click the image to enlarge

Source: HSBC Asset Management. Data as of March 2026.

This dynamic creates an asymmetric outcome. In a falling-rate scenario, corporate bonds benefit from both duration and carry. In a rising rate environment driven by renewed inflation or fiscal concerns, the additional spread income provides a cushion relative to sovereign bonds. In both cases, high quality corporate credit offers a more balanced risk-return profile than pure government duration.

Historical precedent reinforces this logic. During the 2011–12 sovereign crisis, Italian government spreads widened sharply, yet corporate spreads tightened following ECB intervention, illustrating how central bank liquidity often transmits more directly into credit markets than into sovereign premia. More recently, heavily oversubscribed ultra-long corporate issuance – including century maturities – highlights investor willingness to treat certain high-grade corporates as duration anchors comparable to sovereigns. For fixed income investors, therefore, high-quality investment grade corporate bonds increasingly function as a core defensive allocation, not merely a satellite exposure. In an environment where traditional safe assets are being repriced, institutional investors might continue to support best-rated corporate credit markets.

For Professional Clients and intermediaries within countries and territories set out below; and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager’s skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets: investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

All data from HSBC Asset Management unless otherwise specified. Any third-party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group).

- In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws;

- In Bermuda, this document is issued by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority;

- In France, Belgium, Netherlands, Luxembourg, Portugal, Greece, Finland, Norway, Denmark and Sweden this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026);

- In Germany, this document is issued by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients);

- In Hong Kong, this document is issued by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This content has not been reviewed by the Securities and Futures Commission;

- In India, this document is issued by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India;

- In Italy and Spain, this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026) and through the Italian and Spanish branches of HSBC Global Asset Management (France), regulated respectively by Banca d’Italia and Commissione Nazionale per le Società e la Borsa (Consob) in Italy, and the Comisión Nacional del Mercado de Valores (CNMV) in Spain;

- In Malta, this document is issued by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act;

- In Mexico, this document is issued by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversión, Grupo Financiero HSBC which is regulated by Comisión Nacional Bancaria y de Valores;

- In the United Arab Emirates, this document is issued by HSBC Investment Funds (Luxembourg) S.A. – Dubai Branch (Level 20, HSBC Tower, PO Box 66, Downtown Dubai, United Arab Emirates) regulated by the Capital Market Authority (CMA) in the UAE to conduct investment fund management, portfolios management, fund administration activities (CMA Category 2 license No.20200000336) and promotion activities (CMA Category 5 license No.20200000327).

- In the United Arab Emirates, this document is issued by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Capital Market Authority in the UAE under CMA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient’s country of residence and therefore may not be subject to supervision of the local regulator in the recipient’s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient’s country of residence.

- In Singapore, this document is issued by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore;

- In Switzerland, this document is issued by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website; if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (“SBA”) Brochure “Risks Involved in Trading in Financial Instruments”;

- In Taiwan, this document is issued by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan);

- In Turkiye, this document is issued by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations.

- In the UK, this document is issued by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority;

- In the US, this document is issued by HSBC Securities (USA) Inc., an HSBC broker dealer registered in the US with the Securities and Exchange Commission under the Securities Exchange Act of 1934. HSBC Securities (USA) Inc. is also a member of NYSE/FINRA/SIPC. HSBC Securities (USA) Inc. is not authorized by or registered with any other non-US regulatory authority. The contents of this document are confidential and may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose without prior written permission.

- In Chile, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Obtain information about the state guarantee to deposits at your bank or on www.cmfchile.cl;

- In Colombia, HSBC Bank USA NA has an authorized representative by the Superintendencia Financiera de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution;

- In Costa Rica, the Fund and any other products or services referenced in this document are not registered with the Superintendencia General de Valores (“SUGEVAL”) and no regulator or government authority has reviewed this document, or the merits of the products and services referenced herein. This document is directed at and intended for institutional investors only.

- In Peru, HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Perú whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Perú and is not for public distribution;

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy.

Copyright © HSBC Global Asset Management Limited 2026. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Asset Management.

Content ID: D066766; Expiry Date: 28.02.2027